Accommodating Peer-to-Peer Carsharing at Airports: A Guide (2024)

Chapter: 5 Financial Implications of P2P Carsharing for Airport Operators

CHAPTER 5

Financial Implications of P2P Carsharing for Airport Operators

This chapter describes the importance of rental car revenues to airport operators and the potential effect P2P carsharing services could have on these revenues.

5.1 Revenues Airports Receive from Traditional Rental Car Businesses

To better serve their customers and the local community, airport managers seek to maintain or enhance their non-aeronautical revenues in order to attract new airline service and maintain existing service by offering airlines competitive rates and charges.

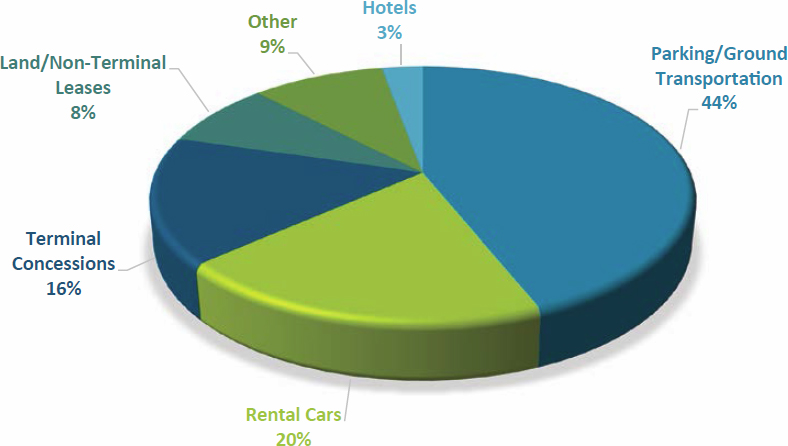

As shown in Figure 5-1, the largest source of non-airline revenues is public parking/ground transportation, followed by rental cars [excluding customer facility charges (CFCs)]. Rental car revenues represent about 20 percent of total non-aeronautical revenues at U.S. airports, with the percentages varying based on the airport’s size or hub classification. The FAA defines airport hub sizes on the basis of the percentage of U.S. annual airline passenger boardings an airport serves, with a large hub serving over 1.0 percent, a medium hub serving between 1.0 percent and 0.25 percent, a small hub serving between 0.25 percent and 0.05 percent, and a non-hub serving less than 0.05 percent. (The data source for Figure 5-1 and Figure 5-2, as well as for Table 5-1, is CATS, which includes data from 520 commercial service airports in the United States.)

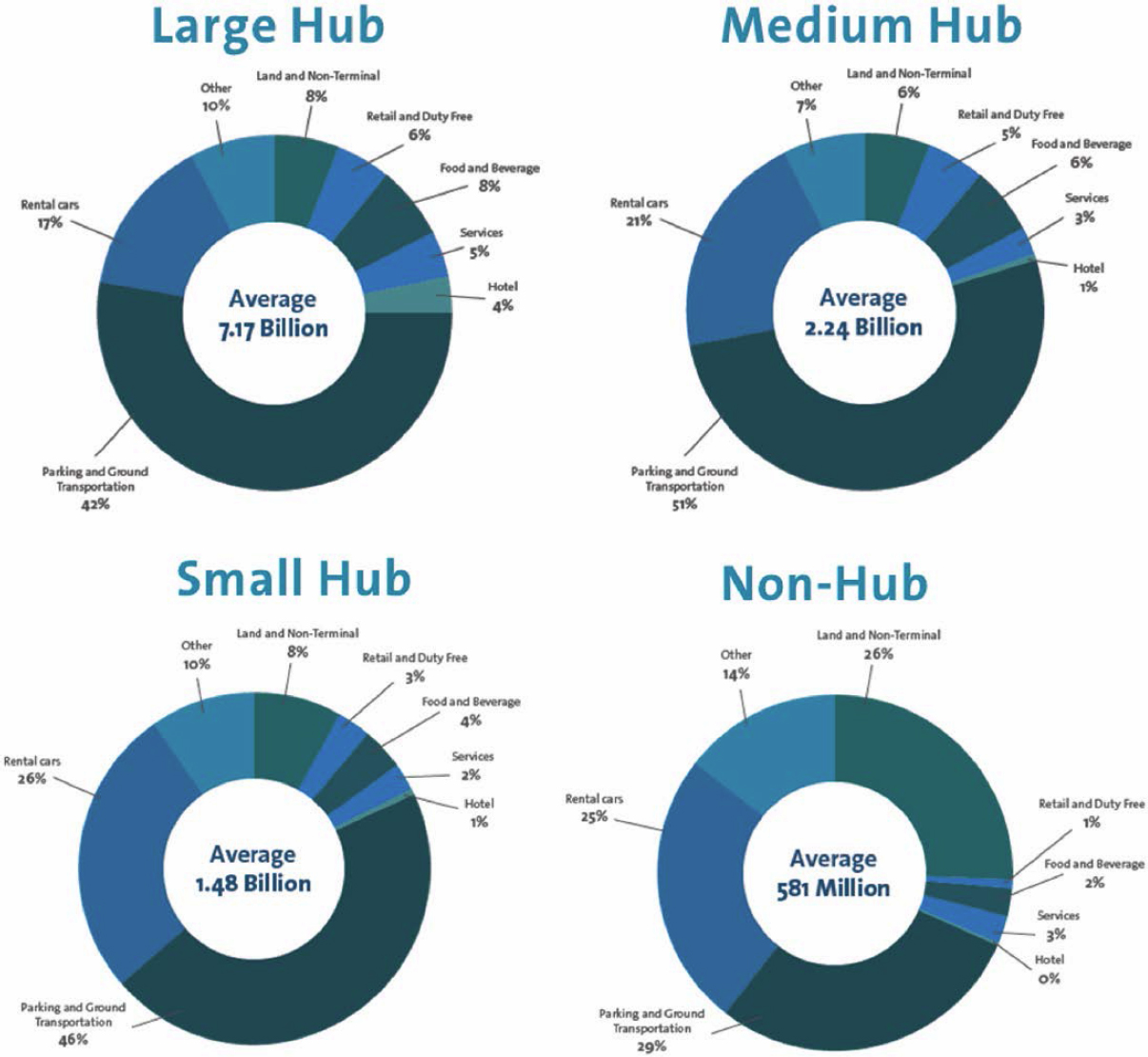

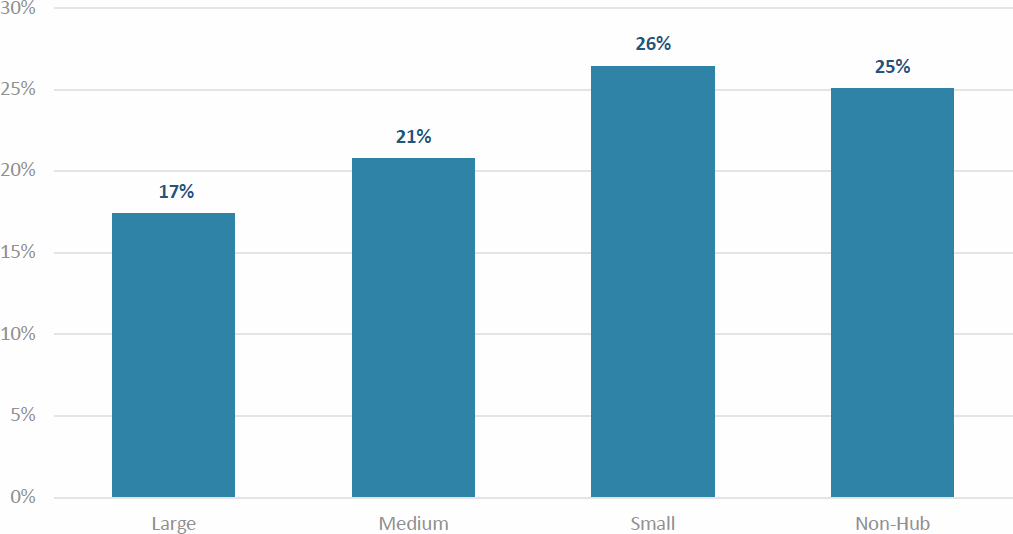

As shown in Figure 5-2, parking and ground transportation revenues are between 29 percent (small-hub airport average) and 51 percent (medium-hub airport average) of an airport’s non-airline revenues. As shown in Figure 5-2 and Figure 5-3, rental car revenues are between 17 percent and 26 percent of total non-aeronautical revenues, again depending on hub size.

As shown in Table 5-1, the average cost per enplanement (CPE) at U.S. airports varies from $14.45 at large-hub airports to $7.55 at non-hubs, with an average of $9.84 per enplaned passenger for all commercial service airports in the United States. Table 5-1 also presents the rental car revenue per enplaned passenger, which, as shown, varies from $6.05 at non-hub airports to $2.23 at large hubs, with the overall average of $3.88 per enplaned passenger.

5.2 Potential Effects of P2P Carsharing Businesses on Airport Revenues

An airport operator’s ability to maintain or enhance non-aeronautical revenues can be challenged if P2P carsharing companies divert market share from traditional rental car companies but do not pay airport operators similar fees. Consequently, airport operators typically require

Figure 5-1. Allocation of non-aeronautical airport revenues.

P2P carsharing companies to have a business agreement to operate at an airport and to pay a fee pursuant to such an agreement. However, if the fee that airports require P2P companies to pay is less than traditional rental car companies are charged (e.g., a fee per each rental car transaction), the revenue collected from P2P carsharing businesses would not completely replace the fees paid to an airport by the traditional rental car companies, assuming the P2P customer would have otherwise rented from a traditional company.

A reduction in rental car revenue per enplanement would directly affect an airport’s overall CPE. For example, if a large-hub airport were to lose a portion of its rental car revenues to P2P carsharing, then its CPE would increase from the current average of $14.45. Such a loss of revenues, whether from P2P carsharing or other reasons, would present a challenge to an airport’s revenues and business model.

Consequently, to maintain existing revenues and potentially increase these revenues, airport operators typically require P2P carsharing companies to pay fees to conduct business on the airport. These fees are often similar to those paid by traditional on-airport and off-airport rental car companies.

Figure 5-2. Non-aeronautical airport revenues by hub size.

Table 5-1. Average CPE and rental car revenue per enplanement.

| Hub Size | CPE | Rental Car Revenue per Enplanement |

|---|---|---|

| Large | $14.45 | $2.23 |

| Medium | $9.65 | $2.44 |

| Small | $7.73 | $4.79 |

| Non-Hub | $7.55 | $6.05 |

| Average | $9.84 | $3.88 |

Source: DKMG Consulting, LLC, CATS database maintained by the FAA, as of September 2023.

Figure 5-3. Rental car revenues as a percentage of total non-aeronautical airport revenues.