Implementation of A Guide to Computation and Use of System-Level Valuation of Transportation Assets (2026)

Chapter: 1 Research Summary

1. Research Summary

1.1 Background

Transportation agencies need to determine the current value of their physical assets to prepare financial reports and to support various applications related to transportation asset management (TAM). For U.S. agencies, the topic of asset value first arose in the 1990s with the development of Governmental Accounting Standards Board (GASB) Statement 34. This document details accounting standards for state and local agencies to use to prepare their financial statements, requiring that these statements include a calculation of the value of an agency’s physical assets.

More recently, in its requirements for National Highway System (NHS) Transportation Asset Management Plans (TAMPs), the Federal Highway Administration (FHWA) required that State Departments of Transportation (DOTs) include a calculation of the value of NHS pavement and bridge assets in their TAMPs, and that they calculate the cost of maintaining asset value. These requirements appear in 23 Code of Federal Regulations (CFR) § 515.7(d)(4).

Calculating asset value is important not simply because doing so is required – it is also consistent with best practice in TAM. Once an agency has calculated the value of its assets, the agency can use the resulting value as a measure to help describe its asset management program, demonstrate the impact of its investments, and answer key questions related to TAM. Asset values serve to help summarize the quantity of assets an agency owns or maintains. Changes in value show the direction of asset conditions and whether an agency’s inventory is improving or deteriorating. Further, depending on how it is calculated, asset value can support decisions about how best to invest in assets, or even whether an investment is justified.

NCHRP Project 23-06 developed guidance for agencies to use to calculate asset value to support TAM. This guidance is detailed in NCHRP Web-Only Document 335 and is included in the digital version of the guidance depicted in Figure 1-1, now maintained by the American Association of State Highway and Transportation Officials (AASHTO).

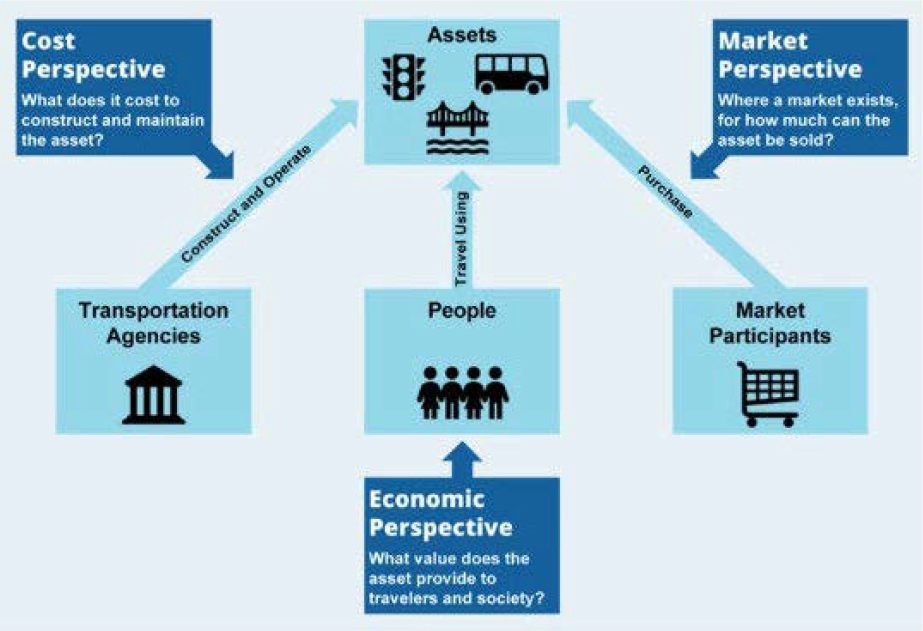

A key feature of the NCHRP guidance is that it recognizes different perspectives regarding what asset value represents. As depicted in Figure 1-2, the value of an asset can be viewed based on

Source: NCHRP Web-Only Document 335

the cost of the asset, on its market value (in cases where a market exists, such as for used vehicles), or on the economic benefits the asset yields.

The best approach to use for calculating asset value depends upon one’s perspective on what asset value represents, as well as on what data is available to support the calculation, and the specific questions one is trying to use asset value to help answer. The guidance details the different approaches and provides flowcharts recommending an approach for performing the different steps of the asset value calculation depending on the various relevant factors.

NCHRP Project 23-06 included a set of proof-of-concept tests of the asset valuation guidance. These tests were used to help validate the guidance and develop worked examples. However, opportunity remained to support the implementation of the NCHRP 23-06 research. Given there are many paths through the asset valuation guidance, a key activity for supporting implementation of the research was to perform additional agency pilots that demonstrate different implementation approaches and serve as case studies that provide useful information to other agencies seeking to improve their asset value approach. The pilots were tailored to explore specific issues such as:

How does an asset valuation calculation performed using current replacement costs made to support TAM compare to an alternative approach using historic costs made to support financial reporting using GASB Statement 34?

- What issues might an agency encounter if they extend their asset value calculation made for their TAMP for NHS pavement and bridges to other ancillary assets?

- How does the value calculated based on an economic perspective compare to the value calculated based on a cost or market perspective?

- Under what cases is it feasible to use market value to establish value? What are the challenges and benefits of this approach?

- Are there additional issues specific to local agencies or transit agencies that need to be incorporated in the asset valuation guidance given it is intended to support a multi-modal calculation?

The research effort explored these and other related issues through the agency pilots. Also, based on the experience gained from the pilots, the research team will develop additional materials to support implementation of the research, as detailed further in Section 1.3.

Note that while the pilots performed during this research project focused on highway transportation assets (i.e., pavements, bridges, and ancillary assets), the asset valuation guidance may be applied to all types of transportation assets and modes, including transit, ports, airports, and others. The valuation framework and calculation steps can support asset valuation needs for any U.S. agency responsible for transportation assets.

1.2 Research Objectives

The objective of this implementation project was to promote and support further use of the asset valuation guide through the development and dissemination of outreach materials that provide an overview of the guide, through case studies, and through supplemental tools and worksheets. The results of this project were added to the web-based version of the asset valuation guidance.

1.3 Research Approach Summary

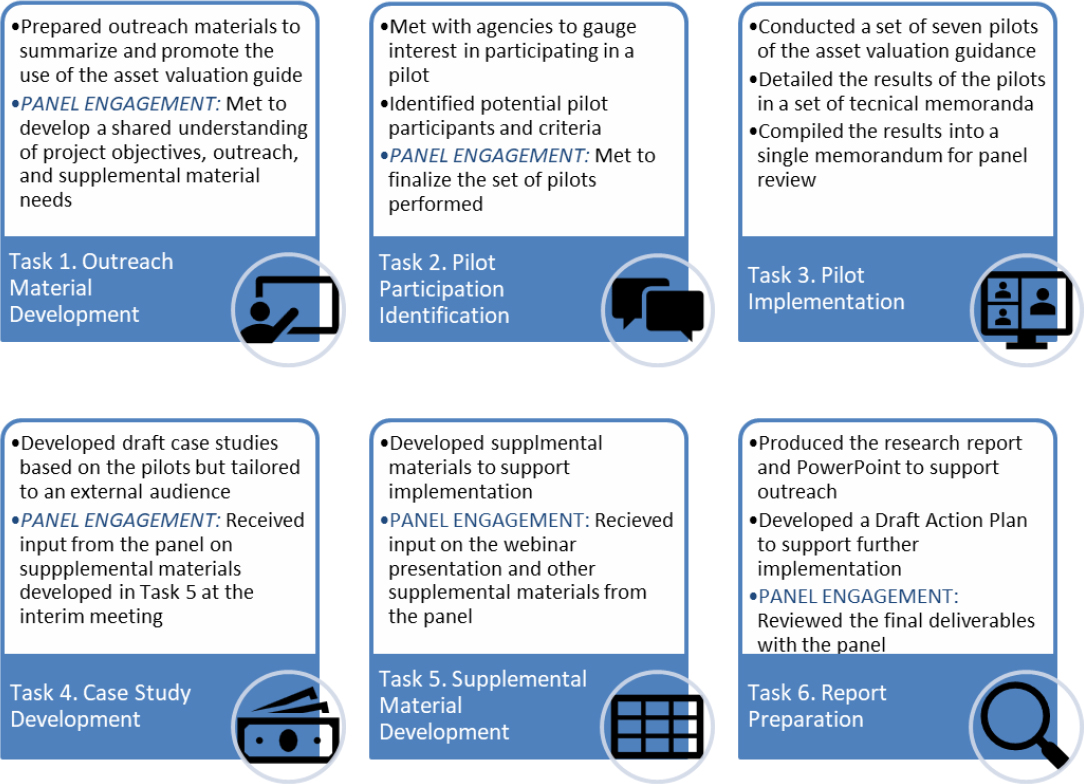

The work was conducted through six tasks. In Task 1, the project team worked closely with the project panel to develop a shared understanding of the project goals, approach to the pilots, and the supplementary tools and other resources that were needed to support the outreach and ongoing use of the asset valuation guide. The team then developed outreach materials.

In Task 2 the team distributed materials developed in Task 1 to help promote the research and then establish a set of candidate pilot participants. The team met with the panel to finalize the set of pilots to perform as part of the project. In Task 3 the team performed the set of six pilots of the asset valuation guidance. In Task 4 the team used the results of the pilots to develop a set of case studies. The team then used information gathered in Tasks 1-4 to assist in developing supplemental materials as part of Task 5 to support the use and advancement of asset valuation. In Task 6 the team prepared this report summarizing the research. Figure 1-3 provides a graphical representation of this approach, including panel and stakeholder engagement.

1.4 Document Organization

The remainder of this document is organized as follows:

- Chapter 2 details the work performed for each task of the project.

- Chapter 3 presents an action plan for potential, future activities to further research implementation.

- Appendix A presents the outreach materials developed in Task 1.

- Appendix B presents the case studies developed in Task 4 and 5.

- Appendix C is a presentation summarizing the research.