Paying the Price: The Status and Role of Insurance Against Natural Disasters in the United States (1998)

Chapter: 9 A Program for Reducing Disaster Losses Through Insurance

CHAPTER NINE

A Program for Reducing Disaster Losses Through Insurance

HOWARD KUNREUTHER

THIS CHAPTER FIRST LOOKS at the current market for insurance against natural disasters by addressing the following questions: What are the factors influencing property owners' demand for insurance? Why are insurers reluctant to provide coverage against hurricanes, floods, and earthquakes today? An understanding of both the demand and supply sides of the market suggests a disaster management program where private insurance plays a central role in bringing together other policy tools and key interested parties.

THE CURRENT SCENE

It is apparent from the preceding chapters that residents of hazard-prone areas as well as the insurance community are reluctant to deal with natural disasters today for very different reasons. Many homeowners at risk are not anxious to purchase insurance voluntarily because they feel the disaster will not happen to them; others who have compared premiums with potential benefits may feel that insurance is not a good investment, as indicated by the number of policies

that have been canceled since the California Earthquake Authority was instituted in California in 1996.

Private insurers have been reluctant to promote coverage against hurricanes, floods, and earthquakes because of uncertainty regarding the risk and because of concern with what the financial consequences of a natural disaster would be for their companies. Hurricane Andrew and the Northridge earthquake were wake-up calls for many firms, alerting them to the possibility of insolvency following another major event. Hence, insurers want to limit their exposure in hazard-prone areas. In some cases they are restricted from doing so by state regulatory agencies and insurance commissioners.

Demand for Insurance

As shown in Chapter 3, many property owners at risk do not purchase insurance voluntarily. As of July 1997 only 20 percent of residential properties in flood-prone areas in the United States were covered by insurance. In California, which is the area in the continental United States most susceptible to earthquakes, less than 20 percent of residences have earthquake insurance, down from 30 percent to 40 percent at the time of the Northridge earthquake. Most homes have protection against wind damage from hurricanes, since it is part of the standard homeowners' policy, which is normally required by financial institutions as a condition for a mortgage.

Unless individuals have personally experienced an event or know others who have suffered losses, they are unlikely to voluntarily purchase insurance coverage against natural disasters (Kunreuther et al., 1978). Relatively little insurance was purchased by residents of Kobe prior to the January 1995 earthquake, presumably because the city had never experienced a severe earthquake. Following the severe earthquakes in California in the 1980s and early 1990s, voluntary demand for insurance increased because residents in affected areas became concerned about future damage from these disasters (Palm, 1995).

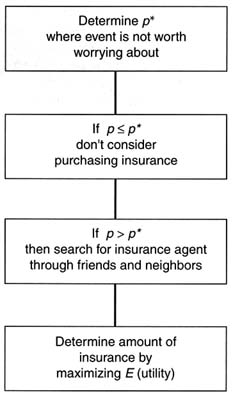

Figure 9-1 presents a model of the decision-making process involved when individuals choose whether to purchase hazard insurance. Residents in hazard-prone areas have a perceived probability of a disaster p which influences their decision on whether to purchase coverage. There is likely to be a threshold probability p* below which a person will not want to buy coverage because the costs—the attention costs of thinking about the event as well as the transaction costs of collecting information

FIGURE 9-1 Sequential model of choice for homeowners' decisions. Source: Kunreuther et al., 1978.

and deciding on the amount of coverage—are too high. The higher these costs, the larger p* will be. Those who feel that the probability of a disaster exceeds their cost threshold (p > p*) are likely to seek out friends and neighbors for information on where to buy coverage (Kunreuther et al., 1978; Weinstein, 1987). Once they obtain this information, people base their actual purchase decision on tradeoffs between the costs of insurance in relation to the risks of being unprotected, using a set of simplified rules rather than undertaking detailed calculations.

In her recent studies of insurance purchase in California, Palm (1995) found that the decision to purchase coverage is influenced primarily by assessing risks and costs. This suggests that most people in California are already aware of the presence of earthquake insurance and do not have

to turn to friends and neighbors for information on coverage. It thus appears that the demand for insurance depends on whether the product is at an early or late stage of the diffusion process. In the case of earthquake coverage, the market is much more mature than it was in the 1970s when earlier demand studies were undertaken.

What determines the demand for insurance when individuals have the freedom to specify coverage limits is still not well understood, although recent controlled experimental studies provide insight into consumer decision processes. For example, there is evidence that framing manipulations influence how much consumers are willing to pay for coverage. Some of these factors are the vividness of the media's reporting of a projected event, the use of rebates so that policyholders feel they have experienced a gain if they do not collect on their policies, and the use of the status quo as a reference point for deciding between options. Data from insurance markets indicate that these same effects occur when actual insurance decisions are made (Johnson et al., 1993).

Supply of Insurance

Turning to the supply side of the market, Chapter 2 points out that insurers and reinsurers are concerned about the impact of future severe earthquakes and hurricanes on their solvency. Large insured losses from such disasters could significantly reduce their surplus, which is likely to lead to a restriction in future coverage. Firms in the industry are therefore considering either rationing policies written in high-risk areas and/or supplementing traditional reinsurance with funding from the capital markets.

The literature in recent years suggests that insurers and other firms are risk averse, and hence they are concerned with non-diversifiable risks such as catastrophic losses from disasters (Mayers and Smith, 1982). (See Froot et al., 1994, for a discussion of the increasing role that risk management tools are playing in how corporations are doing business today.) As discussed in Chapter 2, insurers are also likely to be averse to ambiguity, as shown by their taking uncertainty regarding loss into account when determining the premium they would like to charge. Actuaries and underwriters both utilize heuristics that reflect these concerns.

Actuaries normally determine a premium based on expected value by assuming that the probability and loss are known. They then increase this value to reflect the amount of perceived ambiguity in the probability and/or uncertainty in the loss. One commonly used formula for determining

a premium is z = (1 + λ)µ, where µ = expected loss (i.e., p × L) and λ > 0 is a factor reflecting ambiguity and uncertainty independent of any adjustment to cover administrative costs (Lemaire, 1986).

Underwriters decide whether a risk is insurable by utilizing the actuary's recommended premium z as a reference point, and then focus on the impact of a major disaster on their company's solvency. In other words, underwriters are first concerned with the firm's safety and then with profit maximization. A safety-first model, first proposed by Roy in 1952, can be contrasted with a value maximization approach to firm behavior. A safety-first model explicitly concerns itself with insolvency when making a decision regarding maximum amount of coverage and premiums to charge. A value maximization model recognizes that firms are risk averse so that premiums have to be higher to reflect the chances of a catastrophic loss. It does not explicitly focus on keeping the probability of insolvency below some prespecified level. Stone (1973) formalized these concepts by suggesting that an underwriter who wants to determine the conditions under which a specific risk is insurable will first focus on keeping the probability of insolvency below some threshold level q*.

As an example, suppose that an insurer expects to sell S policies, each of which can create a loss L. The underwriter recommends a premium z* so that the probability of insolvency is no greater than q*. Risks with more uncertain losses or greater ambiguity will cause underwriters to want to charge higher premiums for a given portfolio of risks. The situation will be most pronounced for highly correlated losses, such as earthquake policies sold in one region of California.

A safety-first model of underwriter behavior is consistent with the Mayers and Smith (1990) rationale as to why insurance firms want to purchase reinsurance. In fact, a rule that focuses on keeping the chances of insolvency below q* explicitly recognizes the role that risk plays in the decision process. By characterizing the underwriter's behavior in this way, one can then examine how reinsurance and other capital market instruments can alleviate these concerns.

Interview data with several U.S. insurance companies provides additional evidence that firms follow a safety-first model. Prior to Hurricane Andrew (1992) and the Northridge earthquake (1994), these insurers were not worried about the potential impact of losses to their portfolio from severe hurricanes and earthquakes. Hence they did not attempt to restrict coverage and/or make the case for higher premiums because of the likelihood that they would become insolvent.

In the aftermath of Hurricane Andrew and Northridge, company executives modified their views and are now concerned about their ability to survive a future catastrophe given their current portfolios and the amount of reinsurance coverage they can obtain at a reasonable price. In other words, they feel that their chance of insolvency based on their current portfolios exceeds their threshold level of concern q*. Therefore, they want to exercise one or more of the following options: reduce the number of policies they write in catastrophe-prone areas, raise their perunit premium z, or obtain more reinsurance coverage.1 Earlier chapters in this book have shown that insurers in the United States have had problems undertaking these actions due to regulatory constraints in some states (e.g., Florida), which have set ceilings on the premiums they can charge and limited the number of policies that they cancel in any given year.

Winter (1988, 1991) and Doherty and Posey (1992) have shown that a particularly severe earthquake or hurricane could have a very negative impact on the availability of insurance throughout the country. Doherty, Posey, and Kleffner (1992) have examined how insurers have responded to a variety of surplus shocks in the past. Their analysis suggests that only 50 percent of the lost surplus is likely to be replaced following a catastrophic loss, so that the availability of coverage in many different lines of insurance would have to be reduced in the immediate aftermath of the disaster.

Key Role of Insurance

The challenge society faces today is how to promote investments in cost-effective risk reduction measures, while at the same time placing the burden of recovery on those who suffer losses from natural disasters. In theory, insurance is one of the most effective policy tools for achieving both objectives because it rewards investments in cost-effective mitigation with lower premiums and provides indemnification should a disaster occur. (This presumes that both homeowners and insurers are aware of state-of-the-art technologies and can determine what impact they will have on reducing expected losses from future disasters.)

In practice, insurance has not played this role in recent years. Insurers generally do not charge premiums that encourage loss prevention measures for several reasons. First, they feel that few people would voluntarily adopt these measures based on the small annual premium reductions in relation to the large up-front cost of investing in these measures. If individuals have short time horizons, they would have little interest in investing $1,200 in return for a reduction in premiums of $200.

As shown in Chapter 8, insurance is a highly regulated industry; rate changes and new policies generally require the approval of state insurance commissioners. Premium schedules with rate reductions for adopting certain mitigation measures require administrative time and energy both to develop and to promote to the state insurance commissioners. If potential policyholders do not view mitigation measures as attractive investments, insurers who developed these premium reduction programs would be at a competitive disadvantage relative to those firms who did not.

A HAZARD MANAGEMENT PROGRAM FOR DEALING WITH CATASTROPHE RISKS

Private insurance can be an important part of a hazards management program, but this requires a reorientation of its role in preventing losses as well as covering damage from disasters. Fortunately, we can think more broadly about how insurance can help manage these risks in the future because of advances in the technology for analyzing data, and because of the recent availability of capital market funding for supplementing traditional reinsurance. These developments suggest a strategy in which private insurance plays a key role in encouraging cost-effective risk reduction measures while providing protection against the financial consequences of disaster.

For such a strategy to be successfully implemented, the insurance and reinsurance industries need to be closely linked with other interested parties in the private sector, notably the financial institutions, investment bankers, and the building and real estate communities. Also, government agencies at the local, state, and federal levels need a much clearer understanding of the importance of having insurance rates reflect the risks of living in hazard-prone areas, and of the possible need for multistate and/or federal arrangements to cover some of the losses from future disasters. The proposed hazard management program consists of the following elements, which will be discussed in more detail below:

-

improving estimates of risk

-

auditing and inspecting property

-

emphasizing building codes

-

providing economic incentives for mitigation

-

broadening protection against catastrophic losses.

Improving Estimates of Risk

Insurers will benefit from improved estimates of the risk associated with catastrophes in two ways. First, by obtaining better data on the probabilities and consequences of disasters, insurers will be able to more accurately set their premiums and tailor their portfolios to reduce the chances of insolvency. The improved information should enable them to more accurately determine their needs for protection through reinsurance or capital market instruments. Second, more accurate data on risk also reduces the asymmetry of information between insurers and other providers of capital. Investors are more likely to supply additional capital as they become increasingly confident in the estimates of the risks of insured losses from natural disasters.

In setting rates for catastrophe risks, insurers have traditionally looked backwards, relying on historical data to estimate future risks. 2 This process is likely to work well if there is a large database of past experience from which to extrapolate into the future. Low-probability, high-consequence events such as disasters, by their very nature, make for small historical databases. Thus, there is a need to integrate scientific estimates of the probabilities and consequences of events of different magnitudes with the evidence from past experience. (New advances in seismology and earthquake engineering are discussed in FEMA, 1994, and Office of Technology Assessment, 1995.)

In many cases some controversy exists among the experts as to the risks from hazards and technologies. For example, scientific knowledge about the probability of earthquakes of different magnitudes has been growing rapidly since the 1960s, but there is still no consensus on what information to use as the basis for seismic probability maps (Mittler et al., 1995).

Advances in information technology have encouraged catastrophe modeling, which can simulate a wide variety of different scenarios reflecting the uncertainties in different estimates of risk. For example, it is now feasible for insurers to evaluate the impact of different exposure

levels on both expected losses and maximum possible losses by simulating a wide range of different estimates of seismic events using the data generated by scientific experts. Similar studies can be undertaken to evaluate the benefits and costs of different building codes and loss prevention techniques (Insurance Services Office, 1996).

The growing number of catastrophe models has presented challenges to users who are interested in estimating the potential damage to their portfolios of risks. Each model uses different assumptions, different methodologies, different data, and different parameters in generating projections. The models' conflicting results make it difficult for the insurer to know what premiums to set to cover their risks; the results also make it difficult for reinsurance and capital market communities to feel comfortable investing their money in providing protection against catastrophe risk.

Hence the need for a better understanding of why these models differ and of the importance of reconciling these differences in a more scientific manner than has been done up until now. Bringing the leading modelers together with the insurers, reinsurers, and capital markets to discuss how their data are generated may reduce the mystery that currently surrounds these efforts.

Auditing and Inspecting Property

One way to determine the ability of a structure to withstand the impact of natural disasters would be to inspect the property carefully. A

|

BOX 9.1 Open Question about Estimating Risk

|

careful appraisal of the structure is expensive. To date, such audits have been undertaken primarily on commercial risks where the insurer has absorbed the cost of the audit through its large premium base with the policyholder. With respect to residential properties at risk, one way to encourage the adoption of cost-effective risk reduction measures would be to incorporate them in building codes and provide a seal of approval to each structure that meets or exceeds these standards. (Kunreuther and Kleffner, 1992, provide a rationale for strengthening building codes by analyzing the factors that lead individuals to avoid investing in mitigation measures even if they have accurate information on the risk.)

Banks and financial institutions could require that structures be inspected and certified against natural hazards as a condition for obtaining a mortgage. This inspection, which would be a form of buyer protection, is similar in concept to termite and radon inspections normally required when property is financed. Natural hazard inspections are not routinely undertaken by banks today, even though it is in their interest to know as much about the risk as possible to protect their mortgages. The success of a program of natural hazard inspection requires the support of the building industry, of realtors, and of a cadre of inspectors, well qualified to provide accurate information on the condition of the structure.

Emphasizing Building Codes

Building codes serve two principal purposes: they help correct misimpressions that property owners have with respect to the safety of their structures, and they reduce disaster losses that are directly attributable to the collapse of buildings.

How Building Codes Promote Accurate Information about Risk

One reason why property owners misperceive risks is that the real estate community has limited interest in providing information on the nature of hazards, even when required to do so by legislation such as the Alquist-Priolo Special Studies Zone Act (Palm, 1981). Furthermore, engineers and builders have limited economic incentives for designing safer structures since doing so normally means incurring costs that they feel will hurt them competitively (May and Stark, 1992).

Well-enforced building codes help correct misinformation that property owners may have regarding structural safety, while leveling the playing field for constructing buildings. For example, suppose a property

|

BOX 9-2 Open Questions about Property Inspection

|

owner believes that hurricane damage to a structure would total $20,000, but the developer knows that the total would be $25,000 because the house is not well constructed. The developer has no incentive to relay the correct information to the prospective property owner because the developer is not held liable for hurricane damage to a poorly constructed building. If the insurer is unaware of how well the building is constructed, the insurer cannot convey this information to the potential owner through risk-based premiums. Inspecting the building to see that it meets code and then giving it a seal of approval provides accurate information to the property owner. It also forces the developer and real estate agent to let the potential buyer know why the structure has not been officially approved for safety.

Officially designating structures in this way has an additional side benefit. Insurers may want to limit coverage only to those pieces of property that receive a seal of approval. Evidence from a July 1994 telephone survey of 1,241 residents in six hurricane-prone areas on the Atlantic and Gulf Coasts provides evidence supporting this type of program. Over 90 percent of the respondents felt that local home builders should be required to follow building codes, and 85 percent considered it very important that local building departments conduct inspection of new residential construction (Insurance Institute for Property Loss Reduction, 1995).

The Insurance Institute for Property Loss Reduction (IIPLR), now the Institute for Business and Home Safety, has been a driving force in providing economic incentives for communities to adopt building codes and in advocating code enforcement. Formed by the property-casualty insurance companies in the United States, this independent, nonprofit

organization helped create the Building Code Effectiveness Grading Schedule (BCEGS). This rating system, administered by the Insurance Services Office, measures how well building codes are enforced in communities around the United States. Property located in communities that have well-enforced codes will presumably benefit through lower insurance premiums. For fire insurance, lower premiums are based on the level of fire protection.

How Building Codes Reduce Externalities

Cohen and Noll (1981) provide an additional rationale for building codes. A building collapse may create externalities in the form of economic dislocations and other social costs in addition to the economic loss suffered by the owners. The owners may not have taken these consequences into account when evaluating specific mitigation measures.

Consider the following example. A building toppling off its foundation after an earthquake could break a pipeline and cause a major fire, which could damage other homes that had not been affected by the earthquake in the first place. This type of damage has a direct impact on the pricing of insurance in a hazard-prone area. Suppose that an unbraced structure that toppled in a severe earthquake had a 20 percent chance of bursting a pipeline and creating a fire which would severely damage 10 other homes, each of which would suffer $40,000 in damage. Had the house been bolted to its foundation, this series of events would not have occurred.

The insurer who provided coverage against these fire-damaged homes under a standard homeowner's policy would then have had an additional expected loss of $80,000 (i.e., .2 × 10 × $40,000). A building code requiring concrete block structures to be braced in earthquake-prone areas would have prevented this loss. One option for dealing with this situation would be for homes adjacent to those that are not braced to be charged a higher fire premium to reflect the additional hazard of living next to the unprotected house. Charging this additional premium to the unprotected structure that caused the damage would be more equitable, but this cannot legally be done. Thus, each of the 10 homes that are vulnerable to fire damage from the quake would be charged this extra premium.

The point of this analysis is that mitigation yields an additional annual expected benefit over and above the reduction in losses to the specific structure adopting a mitigation measure. All financial institutions

|

BOX 9-3 Open Questions about Building Codes

|

and insurers who are responsible for these other properties at risk would favor building codes to protect their investments and/or reduce the insurance premiums they charge for fire following earthquake.

Providing Economic Incentives for Mitigation

As pointed out in Chapter 7, insurers could provide financial incentives in the form of lower premiums, lower deductibles, or increased coinsurance to encourage the adoption of cost-effective risk reduction measures. If budget constraints prevent a property owner from investing in these mitigation measures, then insurers should consider having a bank or other financial institution provide funds through a home improvement loan with a payback period coterminous with the life of the mortgage.

Consider the following example, where the cost of risk reduction measures on a piece of property in earthquake-prone country is $1,500. If the seismologists' best estimate of the annual probability of an earthquake is 1/100, and the reduction in loss from investing in the risk reduction measure is $27,500, then the expected annual benefit is $275. A 20-year loan for $1,500 at an annual interest rate of 10 percent would result in payments of $145 per year. If the annual insurance premium reduction reflected the expected benefits of the risk reduction measure (i.e., $275), then the insured homeowner will have lower total payments by investing in mitigation than by not undertaking the measure.

The above example also illustrates the robustness of the risk estimates that would still make it desirable for a homeowner with insurance to take out a long-term loan for mitigation payments. Even if the annual probability of an earthquake is as low as 1/189, the property owner would want to take out the loan. (If the probability of an earthquake were 1/189, the annual premium reduction would be $145, the same as the annual loan payment.) Similarly, if the probability p were known to be 1/100, then the reduction in loss from mitigating could be as low as $14,500, and the loan would still be attractive because of the benefits from the reduced insurance premium.

Many poorly constructed homes are owned by low-income families who cannot afford the costs of mitigation measures or the costs of reconstruction should their house suffer damage from a natural disaster. Equity considerations argue for providing this group with low-interest loans and grants so that they can either adopt cost-effective risk reduction measures, or relocate to a safer area. Since low-income victims are likely to receive federal assistance to cover uninsured losses after a disaster, subsidizing these mitigation measures can also be justified on efficiency grounds.

|

BOX 9-4 Open Questions on Economic Incentives for Mitigation

|

Broadening Protection Against Catastrophic Losses

New sources of capital from the private and public sectors could provide insurers with funds against losses from catastrophic events, which would alleviate insurers' concerns that the next major disaster might leave them insolvent. This section examines some of these new developments and proposals.

Role of the Capital Markets

In the past couple of years investment banks and brokerage firms have shown considerable interest in developing new financial instruments for protecting against catastrophe risks (Jaffee and Russell, 1996). Their objective is to find ways to make investors comfortable trading new securitized instruments covering catastrophe exposures, just like the securities of any other asset class. In other words, catastrophe exposures would be treated as a new asset class.

Some of the recently proposed instruments provide funds to the insurer should it suffer a catastrophic loss. J. P. Morgan and Nationwide Insurance successfully negotiated such a transaction, whereby Nationwide borrowed $400 million from J. P. Morgan and placed the money in a trust fund composed of U.S. Treasury securities. Nationwide pays a higher-than-normal interest rate on these funds in return for having the ability to issue up to $400 million in surplus notes to help pay for the losses should a catastrophe occur (Mooney, 1995).

In June 1997 the insurance company USAA floated Act of God bonds that provided it with protection should a major hurricane hit Florida. In July 1997, a two-year catastrophe bond based on California industry losses was put together by Swiss Re Capital Markets, and Credit Suisse First Boston to deal with catastrophic earthquake losses. This multiyear catastrophe bond compares favorably with the rate of return on high-yield corporate bonds. Other financial arrangements, such as catastrophe insurance futures contracts and call spreads introduced by the Chicago Board of Trade (CBOT) in 1992, enable an insurer to hedge against its underwriting risk by attracting capital from insurance and non-insurance segments of the economy (Cummins and Geman, 1995; Harrington et al., 1995). The Catastrophic Risk Exchange (CATEX) creates a marketplace where insurers, brokers, and the self-insured can swap units of their catastrophe risks by region and peril. For example, an insurer could swap units of California earthquake for Florida windstorm (Insurance Services Office, 1996).

Use of Insurance Pools

The National Conference of Insurance Legislators (NCOIL) has considered a multistate Natural Disaster Compact, modeled after the Florida Hurricane Catastrophe Fund, to expand the pool, increase available resources, and further spread geographic risks. This concept has obvious appeal to the most disaster-prone states, and an equal lack of appeal to states where disasters are more rare. As pointed out in Chapter 8, these pools face a number of legal and political challenges which may make it difficult for them to be initiated.

A successful example of the use of an insurance pool is the one that provides coverage against catastrophic losses from nuclear power plant accidents in the United States. Under the Price-Anderson Act, a group of private insurers agreed to provide coverage to utility companies for losses that can total up to $8.5 billion (P.L. 100-408) (U.S. Congress, 1995). The German Pharmaceutical Pool, consisting of private insurers and reinsurers from all over Europe, operates in a similar fashion, providing protection against large risks by private drug manufacturers associated with new drugs (Kunreuther, 1989).

Proposed Federal Solutions

Lewis and Murdock (1996) developed a proposal that the federal government offer catastrophe reinsurance contracts, which would be auctioned annually. The Treasury would auction a limited number of excess-of-loss (XOL) contracts covering industry losses between $25 billion and $50 billion from a single natural disaster. Insurers, reinsurers, and state and national reinsurance pools would be eligible purchasers. XOL contracts would be sold to the highest bidder above a base reserve price which is risk-based. Half of the proceeds above the reserve price would go into a mitigation fund, with the remainder retained to cover payouts. This federal reinsurance effort would be part of a broader program involving mitigation and other loss reduction efforts.

Another proposed option is for the federal government to provide reinsurance protection against catastrophic losses. Private insurers would build up the fund by being assessed premium charges in the same manner that a private reinsurance company would levy a fee for excess-loss coverage or other protection. The advantage of this approach is that resources at the federal government's disposal enable it to cover catastrophic losses without charging insurers the higher-risk premium that

|

Box 9-5 Open Questions about Catastrophic Loss Protection

|

either reinsurers or capital market instruments would require. If one views the private sector as the first line of attack on the problem, as we do, then one would only want to use federal reinsurance as last resort.

SUMMARY AND SUGGESTIONS FOR FUTURE RESEARCH

This concluding chapter has proposed a new approach for managing natural hazards which stresses the importance of private insurance as a catalyst for reducing losses in the future and covering much of the damage after a disaster occurs. This new approach takes advantage of recent developments in information technology and the emergence of new capital market instruments to deal with non-diversifiable catastrophe risks. These two major changes open up opportunities for residents and firms to undertake cost-effective loss protection measures, while at the same time providing a financial cushion to insurers concerned with the possibility of insolvency. Insurance should thus be able to play a more important role in the future in helping to manage catastrophe risks.

The success of the proposed hazard management program requires the active involvement of a number of interested parties from the private sector such as insurers, banks and financial institutions, realtors, builders, and contractors. It also requires that government officials enforce building codes. Public sector agencies have a role in providing assistance

Fire in the Marina district, San Francisco, triggered by ground shaking from the Loma Prieta earthquake, 1989, which ruptured underground water and gas pipelines (USGS, W. Hays).

to low-income families so that they can adopt cost-effective mitigation measures, and so that they can recover after a disaster. The federal government may want to issue XOL contracts or provide catastrophe reinsurance to insurers if the private sector does not offer sufficient coverage. Interested parties in the private sector need to work closely with public sector agencies at the federal, state, and local levels to determine a set of programs that satisfy both the efficiency and equity concerns outlined in Chapter 1.

With respect to future directions for research, the types of cost-effective mitigation measures that could be applied to new and existing structures should be specified. Only then can insurers, builders, and financial institutions work together to incorporate these measures as part of building codes and provide property owners with appropriate rewards for adopting them. Questions remain about the use and enforcement of building codes, and about the types of incentives insurers can provide to individuals who invest in loss mitigation measures (see Boxes 9-3 and 9-4).

One strategy for developing a disaster management program involves analyzing the impact of disasters or accidents of different magnitudes on

different structures. Long-term simulations could help in estimating expected losses from these events and in projecting the maximum probable losses arising from worst-case scenarios. By constructing simulations of large, medium, and small representative insurers with specific balance sheets, types of insurance portfolios, and premium structures, one could examine the impact of different disasters on the insurers' profitability, solvency, and performance under different scenarios. This simulation exercise would enable one to evaluate how risk reduction measures and the provision of funds against catastrophic losses by reinsurers and the capital markets affect insurers' profitability and likelihood of insolvency. An example of the application of such an approach to a model city in California facing an earthquake risk can be found in Kleindorfer and Kunreuther (in press).

Such an analysis may also enable one to compare how attractive capital market instruments are relative to reinsurance for different types of insurers who have specific risks in place. For example, the recent Act of God bonds issued by USAA are similar in form to a proportional reinsurance contract above a retention level. From USAA's point of view, the bonds may be priced more attractively than a comparable reinsurance contract. (Doherty, 1997 provides more details on these and other recent financial instruments.) One would expect the price of reinsurance to fall in the future, given these and other financing and hedging instruments against catastrophe risk, unless certain features of reinsurance would prevent the price from declining. The data from the simulations could also be used to determine the return an investor would require to provide capital for supporting each instrument. The selling prices of different types of capital market instruments would reflect both the expected loss and variance in these loss estimates to capture risk aversion by investors. (See Froot, 1997, for a detailed discussion of reasons why insurers may view reinsurance as more desirable than capital market instruments.)

The type of simulation modeling we describe must rely on solid theoretical foundations in order to delimit the boundaries of what is interesting and implementable in a market economy. Such foundations will also apply to research on the traditional issues of capital markets and the insurance sector, and to research on the processes by which (re-)insurance companies, public officials, and property owners determine levels of mitigation, insurance coverage, and other protective activities. In the area of catastrophe risks, the interaction of these decision processes, which are central to the outcome, seem to be considerably more complicated

than in other economic sectors, perhaps because of the uncertainty and ambiguity of the causal mechanisms underlying natural hazards and their mitigation.

Finally, public sector damage from natural disasters results in a large cost to taxpayers. Government officials should be encouraged to purchase insurance for public structures and invest in cost-effective risk reduction measures. One way to do this is to change legislation so that a lower percentage of damage to these structures is covered by federal disaster recovery funds. Recovery funds would not be available unless municipalities implemented cost-effective mitigation measures. Another alternative is to levy property taxes on all community residents to cover losses to public structures from disasters. This is a form of community-based insurance, with all residents paying a share in proportion to the value of their property. To our knowledge, this alternative has not been seriously proposed as part of future legislation. However, if there is a feeling in Congress that the responsibility for disaster recovery lies primarily with the private sector or at the local level, then insurance, incentives, taxes, and well-enforced local building codes will have a higher profile in the future than they do today. These issues related to the public sector deserve serious study in the future.

This is a very exciting time for the insurance and reinsurance industries to explore new opportunities for dealing with catastrophe risks. If insurance can be used as a catalyst to bring other interested parties to the table, it will have served an important purpose in helping both the industry and society deal with the critical issue of reducing losses and providing protection against damage from earthquakes, floods, hurricanes, and other natural disasters.