Paying the Price: The Status and Role of Insurance Against Natural Disasters in the United States (1998)

Chapter: 5 Hurricane Insurance Protection in Florida

CHAPTER FIVE

Hurricane Insurance Protection in Florida

EUGENE LECOMTE AND KAREN GAHAGAN1

AS POINTED OUT IN CHAPTER 2, windstorm, which includes tornadoes, is covered as a peril in the residential and commercial property insurance policies in use today. This standard feature provides for the direct physical loss of or damage to covered property caused by or resulting from windstorm.

The passage of time and the regularity of windstorm events, hurricanes, and winter storms have confirmed the importance of this insurance. The recent spate of hurricanes to strike the state of Florida, Hurricane Andrew in particular, have revealed the extent to which this coverage is a necessity, as well as the precarious financial position in which many Florida insurers now find themselves. Today there is a question as to whether the voluntary insurance market can provide affordable coverage to customers who seek it and still ensure the long-term solvency of firms in the industry.

FLORIDA'S VULNERABILITY TO HURRICANES

Florida is the state geographically and historically most vulnerable to hurricanes. North Atlantic hurricanes normally form out of tropical depressions off the coast of West Africa and move in a west-to-northwest direction through the Atlantic and Caribbean, frequently toward Florida's coast. They are also known to form in the Gulf of Mexico, the Caribbean, and off the coast of the United States. The North Atlantic hurricane season occurs during the months of June through November, with September generally having the largest number of hurricanes.

From 1871 to 1993, nearly 1,000 tropical storms of varying intensity occurred in the North Atlantic, the Caribbean Sea, and the Gulf of Mexico. Of these, about 180 reached Florida, with 75 known to have had hurricane-force winds (wind speed of 74 mph or greater) and 105, tropical-storm-force winds (39–73mph) (Doehring et al., 1994). During this century, the occurrence of tropical storms has not been random but has exhibited a cyclical tendency, with periods of activity and inactivity lasting two or three decades or longer. For example, the period from the late 1940s through the late 1960s had a much larger number of hurricanes (i.e., a strong cycle) than did the 1970s and 1980s (i.e., a weak cycle). Also, between the years 1900 and 1992 Florida had been hit directly by a little more than one-third of the hurricanes that struck the United States. This is far more than that experienced by any other states on the Atlantic or Gulf coastal states, as indicated in Table 5-1.

TABLE 5-1 Number of Hurricanes Striking Florida and the United States Mainland, 1900–1997

|

|

|

|

|||||

|

Area |

1 |

2 |

3 |

4 |

5 |

Total |

All Major Hurricanesb |

|

Florida |

17 |

16 |

17 |

6 |

1 |

57 |

24 |

|

Total U.S. (Texas to Maine) |

59 |

36 |

47 |

15 |

2 |

159 |

64 |

|

a From the Saffir/Simpson Hurricane Damage Potential Scale. Category 1: 74-95 mph (minimal); Category 2: 96–110 mph (moderate); Category 3: 111–130 mph (extensive); Category 4: 131–155 mph (extreme); Category 5: more than 155 mph (catastrophic). b Greater than or equal to Saffir/Simpson Category 3. Source: NOAA, Tropical Prediction Center. |

|||||||

Recent Hurricane Activity

After Hurricane Andrew in 1992, which caused insured losses of $15.5 billion, Florida was spared hurricane activity in 1993. In the 1994 season, Tropical Storm Alberto caused an estimated $95 million in insured losses, and Hurricane Gordon caused approximately $60 million in insured losses.

The year 1995 was recorded as one of the most active years of this century for storms. The official count for named storms in 1995 was 19, and there were 115 named-storm days (Gray, 1995). Two 1995 hurricanes, Erin and Opal, caused significant damage to coastal property in Florida. Current estimates of insured losses for Erin are $375 million, and for Opal, $2.1 billion, making Opal the third most costly insured hurricane in U.S. history, after Andrew and Hugo.2 Fortunately, losses from Opal did not exacerbate adverse conditions existing in the insurance marketplace in Florida; most of Opal's damage was caused by storm surge, coverage for which is provided by the National Flood Insurance Program.

It has been suggested that the exceptionally active 1995 hurricane season is an indicator of a move toward a new, strong cycle. William M. Gray, of the Department of Atmospheric Sciences at Colorado State University, publishes annual forecasts and periodic updates of Atlantic tropical cyclone activity. He believes the United States may be on the verge of an active hurricane cycle that could last anywhere from 20 to 50 years. This would mean that intense, damaging storms would threaten once every two years instead of the current rate of about once every seven years (Vowinkel, 1995).

Complicating the task of predicting hurricane activity is the growing realization that weather in the southeastern United States may be influenced by the El Niño Southern Oscillation (ENSO) phenomenon. According to O'Brien et al., Atlantic-based hurricanes are more likely to make landfall in a regular year rather than an El Niño year; specifically, "it is 2.2 times more likely to have two or more land-falling hurricanes on the United States" if El Niño has not occurred the previous winter (O'Brien et al., 1996).

Increasing Insurance Exposure

Each year approximately 130,000 new households are established in Florida, drawn by the attractive climate and vigorous economy. These demographic changes play a significant role in increasing Florida's vulnerability to hurricanes. The potential for loss of life and destruction of property continues to expand as the state's population grows and its structures multiply. It is not surprising that five of the ten most costly hurricanes in terms of insured losses have occurred in Florida, as shown in Table 5-2.

Florida's coastal county population rose from 7.7 million to 10.5 million between 1980 and 1993, an increase of 37 percent. As shown in Table 5-3, over three-fourths (78 percent) of Florida's population resides in counties that are adjacent to the Gulf or Atlantic Coasts (IIPLR, 1995).

TABLE 5-2 The 10 Most Costly Insured Hurricanes

|

Dates |

Place |

Hurricane |

Estimated Insured Loss |

|

1992, Aug. 23–24, 25–26 |

FL, LA, MS |

Andrew |

$15,500,000,000 |

|

1989, Sept. 17–18, 21–22 |

U.S. Virgin Islands, PR, GA, SC, NC, VA |

Hugo |

4,200,000,000 |

|

1995, Oct. 4–5 |

FL, AL, GA, SC NC, TN |

Opal |

2,100,000,000 |

|

1992, Sept. 11 |

Kauai and Oahu, HI |

Iniki |

1,600,000,000 |

|

1979, Sept. 12–14 |

MS, AL, FL, LA, TN, KY, WV, OH, PA, NY |

Frederic |

752,510,000 |

|

1983, Aug. 17–20 |

TX |

Alicia |

675,520,000 |

|

1991, Aug. 18–20 |

NC, NY, CT, RI, MA, ME |

Bob |

620,000,000 |

|

1985, Aug. 30–Sept. 3 |

FL, AL, MS, LA |

Elena |

543,300,000 |

|

1965, Sept. 7–10 |

FL, AL, MS |

Betsy |

515,000,000 |

|

1985, Sept. 26–27 |

NC, VA, MD, DE, PA, NJ, NY, CT, RI, MA, NH, VT, ME, TX |

Gloria |

418,750,000 |

|

Source: Insurance Information Institute from estimates provided prior to 1984 by the American Insurance Association; thereafter, by the Property Claim Services division of the American Insurance Services Group, Inc. |

|||

TABLE 5-3 Population Distribution in Florida, 1980–1993

|

|

1980 Population |

1993 Population |

Percent Change 1980–1993 |

1993 Coastal Population as % of Total |

|||

|

Location |

Coastal |

Total |

Coastal |

Total |

Coastal |

Total |

|

|

Florida |

7,659,364 |

9,746,320 |

10,501,222 |

13,527,968 |

37 |

39 |

78 |

|

U.S. Total |

31,340,808 |

226,546,368 |

36,061,500 |

254,293,104 |

15 |

12 |

14 |

|

Source: National Planning Data Corporation, U.S. Census Bureau (IIPLR, 1995). |

|||||||

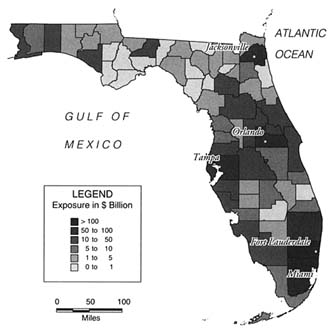

Florida accounts for the largest share of insured coastal exposures in the country. Table 5-4 shows that during the 13-year period from 1980 to 1993 Florida exposures increased from $332.9 billion to $871.7 billion. At that rate of growth and development, the value of property at risk in the state will shortly pass $1 trillion (IIPLR, 1995). See Figure 5-1 for a map of residential and commercial exposures in the state.

When looking at exposure values, it is of interest to note that some of the individual counties in Florida have significantly more property at risk than the total exposures for 16 of the 18 Atlantic and Gulf coastal states. For example, in 1993 Dade County (where Miami is located) exposures totaled $160.8 billion. Just to the north, Broward and Palm Beach counties had exposures of $116.4 billion and $103.0 billion, respectively. Thus, within a fairly small geographic area in southeast Florida, highly vulnerable to hurricanes, there is a concentration of insured property exposures approaching $400 billion (IIPLR, 1995).

Estimating Future Losses

Increased coastal exposures and the magnitude of damage caused by Hurricane Andrew have led to major upward revisions in projections of damage from future severe hurricanes. In addition, post–Hurricane Andrew investigations revealed that property losses were exacerbated by noncompliance with building codes, faulty structural designs, and the scarcity of building material and tradesmen to make repairs (Dade County Grand Jury, 1992). Consequently, most insurers, meteorologists, and academics, who had believed it unlikely that any one U.S. hurricane could cause insured damages on the scale of Hurricane Andrew, altered their views. According to A. M. Best, ''Before 1992, many weather experts believed that the worst-case hurricane in the U.S. would produce less than $10 billion in insured property damage" (BestWeek Property/Casualty Supplement, 1996). That view has changed dramatically.

Recent estimates by Applied Insurance Research (AIR) suggest that if a Category 5 hurricane were to hit Miami or Ft. Lauderdale, it would cause more than $51 billion in insured losses. Factoring in additional costs such as uninsured direct and indirect losses, flood insurance losses, or other economic losses not insured by the private insurance industry would make the total cost much higher (IIPLR, 1995).

The insurance industry has reassessed damageability functions for structures subject to hurricane damage and has made adjustments to reflect

TABLE 5-4 Value of Insured Coastal Property Exposures for Florida, 1980–1993 (in Millions of Dollars)

|

|

Residential |

Commercial |

Total |

Percent Change 1980–1993 |

|||

|

Location |

1980 |

1993 |

1980 |

1993 |

1980 |

1993 |

|

|

Florida |

177,709 |

418,392 |

155,213 |

453,288 |

332,922 |

871,680 |

162 |

|

U.S. Coastal Total |

615,598 |

1,639,741 |

514,066 |

1,507,304 |

1,129,664 |

3,147,045 |

179 |

|

U.S. Total |

4,240,948 |

10,278,875 |

3,807,860 |

11,043,124 |

8,048,808 |

21,421,999 |

166 |

|

Source: Applied Insurance Research, Inc. (IIPLR, 1995). |

|||||||

FIGURE 5-1 Total and residential commercial exposures in Florida.

building code noncompliance, fraud in construction, and the post-loss increase in the costs of labor and materials. The industry has also expanded use of, and reliance upon, unproven loss estimation models, because of their ability to handle complex damageability curves and other data. The credibility of these models will be tested when the next major hurricanes strike.

HURRICANE ANDREW AND THE FLORIDA INSURANCE MARKET

On August 24, 1992, Andrew, a Category 4 hurricane, hit the southern coast of Florida just south of Miami, causing economic damages estimated in excess of $25 billion, which makes it the most expensive hurricane ever to strike the United States. The disaster caused an estimated $15.5 billion in insured losses according to Property Claim Services (PCS). (This figure does not include loss adjustment expenses.) Table 5-5 displays the insured damage by lines of coverage. According to the Florida Department of Insurance, "personal insurance policies covering residential and personal property loss were affected by the total

TABLE 5-5 Insured Hurricane Andrew Damage in Florida, by Line

|

Line of Insurance |

Insured Lossesa |

Number of Direct Claims |

|

Homeowners' |

9,762,571 |

280,000 |

|

Commercial Multiperil |

3,309,863 |

50,517 |

|

Fire and Allied Lines |

932,952 |

24,467 |

|

Auto, Physical Damage |

320,786 |

161,400 |

|

Mobile Home Owners' |

179,472 |

11,779 |

|

Farm Owners' |

13,905 |

1,245 |

|

Other Lines |

491,530 |

17,177 |

|

Total |

15,018,265 |

680,239 |

|

a In thousands of dollars. Note: Individual dollar losses and claims by line do not add to totals because not all companies reported loss information by line of insurance. Source: Florida Insurance Department. Based on information from insurers writing 97 percent of property-casualty insurance in the state, as of December 31, 1992. |

||

destruction of over 28,000 homes; damage to 107,380 homes; and 180,000 persons made homeless" (Gallagher, 1993, p. 1). The large number of homeowners' claims was due to damage to contents and other covered items for owner and non-owner occupied structures. At least 11,779 mobile home claims were made, many involving total loss of the home and its contents (IILPR, 1995). Commercial insurance claims covering property damage, inventory loss, and loss of use were triggered by the total destruction of, or damage to, 82,000 businesses. The loss of power to 1.4 million residents and the loss of telephone service to some 80,000 locations resulted in the interruption of businesses, the loss of electronic records, and the spoilage of food (Gallagher, 1993).

The short-term impact of this storm on the socioeconomic structure of southern Dade County has proven significant. In the year following Andrew, at least 50,000 people decided to move out of the area permanently (IIPLR, 1995). The Metro-Dade Planning Department estimates the total restoration of the population and economic base of the affected area will not occur until the year 2000 (IIPLR, 1995).

Immediate Market Impacts

At the time of Hurricane Andrew, the Florida insurance market ranked fifth in size among the states, with 4.9 percent of total property-casualty

premiums (King, 1993). Due to the magnitude of insured losses inflicted by Hurricane Andrew, an immediate post-storm reaction of a number of insurance companies was to attempt to reduce their underwriting exposure. In early 1993, the Florida Department of Insurance released a list showing 39 insurers who intended either to cancel or not renew 844,433 policies in Florida's post-Andrew marketplace. Factors that influenced the private insurers to take such actions included:

-

the inability to obtain adequate reinsurance for new and existing risks in Florida: when available, the cost of reinsurance was considered too high by primary insurers relative to their alternative costs of capital, and the price they could obtain for coverage from the insureds;

-

new information from catastrophe risk models indicating that existing levels of exposure might be more significant than previously realized, and that these exposure levels were disproportionate to individual company and industry financial resources when considered in the aggregate;

-

significant reductions in insurers' policyholders surplus as a result of Hurricane Andrew losses;

-

concerns about rate adequacy, especially for coastal counties, and for certain classifications of risk such as condominiums;

-

"hidden" exposures resulting from potential assessments by various other mandated insurance mechanisms (e.g., residual markets, catastrophe funds, guarantee funds, etc.);

-

fear that an unfavorable catastrophe exposure would negatively impact the rating by agencies such as A. M. Best and Standard and Poor's.

Some insurers have determined their potential risk of a catastrophic loss in Florida to be so great that they have withdrawn from the state entirely. Withdrawal was prompted in some cases by concerns on the part of the regulator in the insurer's home state about solvency, about the ability to meet other obligations outside Florida, and about the effect of steeply increased reinsurance costs.

Institutional Arrangements

In order to address the needs of stranded policyholders, the insurance commissioner issued an emergency rule on October 15, 1992, that activated the Florida Property and Casualty Joint Underwriting Association

(FPCJUA) on a temporary basis to provide property coverage to all policyholders of insolvent insurers who were already making repairs or were planning to make repairs to their homes. A special session of the legislature held in December 1992 ratified the actions of the Department of Insurance (DOI) and extended the coverage until repairs were completed and the homes became eligible for insurance in the voluntary market.

The FPCJUA had been created in 1986 as a vehicle to provide commercial coverage if and when such coverage became unavailable in the voluntary market. Even though activation of the FPCJUA for the purpose of issuing residential coverage clearly had a questionable legal basis, the DOI initiated this action to resolve a short-term problem and secure the support of private insurers, who agreed not to challenge the emergency rule after it was issued.

The Florida Insurance Guaranty Fund (FIGA) had been created in 1970 to cover the claims payments of insolvent insurers. When insolvencies occurred, FIGA was funded by assessing the property premiums written by all other insurers in the state based on their percentage of market share. The maximum assessment allowed by law at the time of Andrew's occurrence was 2 percent of gross annual premiums, generating about $70 million in available funds (State of Florida, 1993).

Since FIGA's creation, assessments had been minimal and infrequent. However, the liabilities of the Hurricane Andrew insolvencies—more than $400 million in unpaid claims—required a doubling of the assessment rate on insurers (Conning and Company, 1994). Even at this assessment level, FIGA was still short of the funds needed to respond to the insolvencies. In order to fill this gap, the Florida legislature in the December 1992 special session authorized FIGA to issue up to $500 million in tax-exempt revenue bonds. These were issued in February 1993 through the city of Homestead as tax-free municipal bonds, and about $430 million in claims were paid through June 1993.

To repay these bonds, the state legislature authorized the insurers to collect a special additional assessment on policies of 2 percent of premium per year for the next ten years (IIPLR, 1995). The bonds were also insured by MBIA, Inc., the municipal bond insurer. By 1997, with sufficient funds at hand, FIGA retired the city of Homestead's bonds ahead of schedule.

Despite Florida's actions, which successfully dealt with the post-Andrew insolvency crisis, it was obvious to most that problems associated with insolvencies, including delays in claims payments from FIGA

and the burden of continuing indebtedness, created an unstable situation which could grow worse if another major catastrophe struck Florida in the near term. Both the state legislature and the DOI realized that Florida needed a more permanent insurance mechanism to both prevent massive insolvencies and to more efficiently handle those that occur.

Insolvencies

Nine property-casualty insurance companies became insolvent as a direct result of Hurricane Andrew (King, 1993). Eight of these companies were domiciled in the state of Florida, with individual surplus amounts ranging between $1.4 million and $4.4 million. The ninth company, with a surplus of $24 million, was domiciled in Oklahoma but wrote most of its policies in Florida.3 While there was no single characteristic common to these companies, in general they had all experienced poor underwriting results in the year or two prior to Andrew, and most had realized a depletion in their surplus ranging between 9 percent to 68 percent. Six of the insurers were relatively new to the industry, having been incorporated in the mid-1980s (A. M. Best, 1992).

These insolvencies added to the financial burden of other insurers when they were assessed by the FIGA to pay the losses of the defunct companies up to the maximum provided in the law. In fact, a tenth company became insolvent as a result of FIGA's post-Andrew assessments. [This was American Property and Casualty Company, with $2.1 million in surplus (Conning and Company, 1994).]

Insolvencies also contributed to problems with the availability of property insurance after Andrew. Florida law, as it existed at that time, required that every policy issued by an insolvent insurer be canceled within 30 days to allow the policyholders time to find replacement coverage. Following the Andrew-related insolvencies, however, policyholders with damaged property were unable to purchase a policy because most insurers do not accept damaged property under a new policy (Gallagher, 1993).

SEEKING SOLUTIONS

Amid the public clamor for claims payments from FIGA and the unavailability of insurance from the private sector, the Florida Department of Insurance, the state legislature, and the insurance companies (which had previously competed fiercely for business) joined forces to address the mounting public demands for affordable insurance available to all qualified homeowners and commercial establishments. In the ensuing months and years, the regulatory and legislative process generated a latticework of interlocking measures to support the market and make affordable coverage available once more.

Regulatory Response

The State of Florida operates under a "plural executive" concept in which the executive power is divided between the governor and six other elected magistrates. One of the elected magistrates is the treasurer and insurance commissioner, who under Florida statutes has both the power to regulate insurance in the state and also the exclusive executive authority to oversee the insurance industry.

Chapter 627 of the Florida Statutes specifically gives the Department of Insurance (DOI) the authority and responsibility to regulate insurance rates. Insurance companies must file rate requests with the DOI, which are then subject to review and approval or modification. This review uses three basic criteria: rates must not be excessive, inadequate, or unfairly discriminatory.

In order to evaluate whether rates meet these criteria, the DOI uses various factors including projected future losses, the degree of market competition, reinsurance costs, and the catastrophe loss provision (State of Florida, 1993). After Hurricane Andrew, the question of rate adequacy, whether in voluntary or residual markets, has been paramount in the interaction between the insurance commissioner and the state's property insurers.

Moratorium on Insurer Withdrawals

As companies indicated their intent to either reduce their writings or leave the Florida market entirely, the Florida insurance commissioner issued an emergency rule (4ER92-11) on November 17, 1992, which delayed insurance companies from withdrawing from Florida for 90 days.

Mobile home park flattened by Hurricane Andrew, 1992 (FEMA).

They were required to file a written statement of intent containing details of the reasons for their actions 90 days before taking action and had to be prepared to demonstrate that their withdrawal would not adversely affect the market (Florida Department of Insurance, 1994). When the emergency rule was set to expire on February 15, 1993, the DOI issued another emergency rule (4ER93-5) extending the regulations pertaining to withdrawal for an additional 90 days until May 12.

After the second emergency rule expired, the DOI took a more drastic step; on May 19, 1993, the DOI imposed a moratorium on the cancellation and nonrenewal of residential property policies for 90 days to prevent insurers from carrying out their proposed cancellations at the start of the new hurricane season. Shortly thereafter, during the special session of the Florida legislature in the last week of May, the legislature enacted a law extending the moratorium until November 14, 1993, so that a legislatively created Study Commission on Property Insurance and Reinsurance could look into the viability of the property insurance industry and the adequacy of reinsurance.

During a third special session of the legislature, held in November 1993, the state legislature enacted a bill requiring a phaseout of the moratorium, which would last three years, from November 14, 1993 to November 14, 1996. The law provided that in this phaseout period individual insurers could not cancel more than 10 percent of their homeowners' policies in any county in one year, and that they could not cancel

more than 5 percent of their property owners' policies statewide for each year the moratorium was in effect (Insurance Services Office, 1994). The moratorium was, at best, a stopgap measure, designed to buy time while long-term solutions to Florida's property insurance problems were developed (State of Florida, 1993).

During the 1996 state legislative session, the moratorium phaseout law was extended for an additional three years until June 1, 1999. The moratorium's application was broadened to include condominium associations' master policies in addition to homeowner policies (Briggs, 1996). However, the legislature also allowed accelerated nonrenewals. An insurer, with approval of the commissioner, could use its entire "quota" of nonrenewals allowed through June 1, 1999, in the first year. Several major insurers filed for permission to do that, and those filings were approved.

Recently, the U.S. District Court for the Northern District of Florida ruled that the implementation of the moratorium by the state legislature in 1993 was within the state's constitutional rights, considering the economic crisis that could have been caused if a large number of insurers had left the state after Hurricane Andrew in 1992. The ruling is being appealed by the plaintiff insurer. The 11th Circuit of Appeals heard an oral argument in February 1998, but as of this writing has not ruled on it (Jack E. Nicholson, Chief Operating Officer, Florida Hurricane Catastrophe Fund, personal communication, 1998).

While the moratorium serves as a barrier to market exit, it is also a barrier to market entry. Insurers not doing business in Florida are reluctant to enter because they are concerned that they may not be able to exit if business circumstances change. More significantly, the moratorium contributes to the reluctance of insurers already writing in the state to increase their market share. Also contributing to this reluctance are the formulae of the residual market mechanisms, which base assessments on a carrier's market share.

A State Hurricane Trust Fund

In the special legislative session held in November 1993, the Florida Hurricane Catastrophe Fund (FHCF) was created to relieve pressure on insurers to reduce their exposures to catastrophic hurricane losses. This fund enables insurers to remain solvent while renewing most of their policies scheduled for nonrenewal (Florida House of Representatives, 1993); it reimburses a portion of insurers' losses following major hurricanes.

The FHCF, a tax-exempt trust fund administered by the State of Florida, is funded by premiums paid by insurers that write insurance policies on both personal residential property and commercial residential property (defined as apartments and condominiums). Participating insurers are charged premiums based on their property exposure in the state. Rates are based on type of coverage (personal residential, commercial residential, or mobile home), zip code location grouping, construction type, and deductible level.

The FHCF is never obligated to pay more than its assets and borrowing capacity. At year-end 1997, the fund had an estimated capacity of $8 billion—approximately $2 billion in cash derived from premiums and interest earnings, and a borrowing capacity estimated at $6 billion (Jack E. Nicholson, FHCF, 1998). It was planned that these funds would be raised through the issuance of revenue bonds funded by emergency assessments of up to 4 percent of premiums on all property and casualty insurers, excluding workers' compensation writers. As of the spring of 1998, the State of Florida was seeking a private letter ruling from the Internal Revenue Service regarding the ability of the FHCF Finance Corporation to issue tax-exempt debt. Should the ruling be obtained, the estimated bonding capacity of the FHCF will increase around $2 billion due to the lower cost of financing on a tax-exempt basis.

If the fund does not have sufficient resources available to pay all claims in full, each insurer will first be eligible for reimbursement up to an amount equal to the insurer's share of the actual premium paid for that contract year multiplied by the actual claims paying capacity. Each insurer is therefore entitled to its share of the fund's capacity based on the premiums it has paid to the fund. Stated another way, a coverage multiple is calculated by dividing the total claims-paying capacity by FHCF aggregate premiums for the particular year. The product of the coverage multiple and each insurer's FHCF reimbursement premium will determine each insurer's expected minimum payout from the fund. Once insurers are reimbursed for their losses up to their coverage level, reimbursements are next based on losses subject to available funds. Losses are then reimbursed on a prorated basis at the highest level possible, given the remaining available funds.

The coverage multiple for 1997 was calculated by dividing $7.97 billion, which is the sum of the projected fund balance at year-end plus the estimated bonding capacity ($1.97 billion + $6 billion), by the 1977 FHCF reimbursement premiums of $471 million, yielding a multiple of 16.9. This coverage multiple times an insurer's 1997 FHCF reimbursement

premium produces an expected minimum payout from the fund. For example, an insurer that paid a $1 million premium could expect to recover $16.9 million from the FHCF. The insurer may recover more depending on whether other insurers utilized their share of the FHCF's capacity (Jack E. Nicholson, FHCF, personal communication, 1998).

The tax-exempt status of the FHCF is a significant advantage to the insurers participating in it, as it removes a level of potential income taxation resulting from the annual buildup of contingent reserves in years when there are few, or no hurricanes, and provides for a dedicated accumulation of funds in Florida for the benefit of the state's policyholders. Some insurers have now taken steps to issue bonds in the capital markets prior to future hurricane events. In June 1997, USAA successfully floated a catastrophe bond. This bond has two layers of debt: one is subject to interest forgiveness should USAA suffer a loss in excess of $1 billion from a Category 3, 4, or 5 hurricane; the second layer has both principal and interest at risk. The targeted capacity of $400 million was oversubscribed partly because investors are now more familiar with these types of instruments, but also because of the very high return on the investment (Doherty, 1997).

RESIDUAL MARKET MECHANISMS

Residual market mechanisms (RMMs) provide ''insurance of last resort" to individuals who are unable to obtain coverage in the voluntary market. As the example of the Florida Hurricane Catastrophe Fund illustrates, these mechanisms do not actually "remove" losses from the private insurers' financial burden. All insurers writing in the state of Florida must participate in these mechanisms and are subject to assessments by them. Thus, less desirable risks are borne in proportion to a company's market share in the relevant lines of insurance.

Two property insurance residual market mechanisms now exist in Florida, the Residential Property and Casualty Joint Underwriting Association (RPCJUA) and the Florida Windstorm Underwriting Association (FWUA).

Residential Property and Casualty Joint Underwriting Association (RPCJUA)

The RPCJUA was created in the December 1992 special legislative session to address the unavailability of property insurance in the voluntary

market for homeowners' and dwelling fire coverage. [It included the Florida Property and Casualty Joint Underwriting Association (FPCJUA) referred to earlier in this chapter.] It was organized in January 1993, and began issuing policies in March, 1993. The policies issued by the RPCJUA cover single-family homes, townhomes, mobile homes, individual condominium units, and the contents of rented apartments and homes. These policies may be written as complete multiperil policies, which include wind coverage, or are written to exclude wind coverage in the areas eligible for coverage through the Florida Windstorm Underwriting Association.

The section of state law addressing rates has been amended over time. In 1995, lawmakers required the RPCJUA to base its homeowners' rates on the rates and statewide market shares of the 10 largest private insurance companies in the state. In each county, the average rate was required to be as high or higher than the highest average county rate charged by one of those 10 companies. For mobile homes, the rate is set as high or higher in each county than the highest average county rate

|

SIDEBAR 5-1 Current Status of the Residential Property and Casualty Joint Underwriting Association (RPCJUA) As of February 28, 1998, the RPCJUA stood at 372,289 personal lines residential policies, with $50.6 billion in coverage. Much of the exposure in the personal lines residential book is in south Florida. Approximately 271,000 policies, representing 73 percent of the total, and $42 billion in exposure, representing 83 percent of the total, were in three south Florida counties: Dade, Broward, and Palm Beach. On the commercial lines residential side, there has also been a significant drop in policy count and exposure. The commercial book peaked at 2,291 policies in March 1997, with $11.5 billion in coverage. As of March 21, 1998, the commercial book stood at 1,041 policies and $4.7 billion in coverage. There has been continuing concern among insurers and legislators about the RPCJUA's fiscal condition and the aggregate windstorm exposure. For this reason the state legislature created special purpose homeowners' insurance companies |

charged by one of the five largest private companies writing mobile home policies, based on the companies' statewide market shares. The higher price of RPCJUA policies, therefore, encourages consumers to seek private market coverage (Gallagher, 1993).

In the early history of the RPCJUA, lawmakers and state regulators viewed its rates as too low and undercutting the rates charged by private insurance companies. This fact, at least in part, helped spur the association's early growth. However, between 1993 and 1998, the total cumulative increase in premium on a statewide average basis was 90 percent for homeowners' policies, 83 percent for dwelling fire policies, and 67 percent for mobile home policies. Today, the association's rates are generally the highest in the market in each of Florida's 67 counties.

The RPCJUA accepts almost all applications for coverage, although it is not allowed to write windstorm coverage in areas eligible for coverage by the Florida Windstorm Underwriting Association. The RPCJUA peaked at 937,000 personal residential lines policies in September 1996, with $98.2 billion in coverage. However, the association has been significantly

|

for RPCJUA takeouts. In late 1997, the first special purpose homeowners insurance company was formed under Florida law. Companies such as this one may only write policies removed from the RPCJUA or assumed from an unaffiliated authorized insurer and cannot write policies in the voluntary market. They are not members of the RPCJUA or the FWUA and therefore not subject to regular assessments. However, their policyholders are still subject to emergency assessments. These insurers would be subject to assessment only by the guarantee fund, the FIGA, and the catastrophe fund. In May, 1997, the RPCJUA board put into place a catastrophe-financing program that essentially doubled the association's capacity to pay claims from a major hurricane. The program includes $279 million in regular assessments upon member companies, $1.15 billion in proceeds from the Florida Hurricane Catastrophe Fund in 1997, $500 million in pre-event notes (which are invested in a trust fund until needed), and a $1.5 million line of credit with a worldwide group of banks. (This financing program replaced the $1.5 billion line of credit the RPCJUA put in place in 1995.) This new financing program, coupled with the |

reduced in size since then through various depopulation initiatives.

Under the law, most property insurance companies (except for special purpose homeowners' companies) are required to be members of the RPCJUA. Each year, the association determines the companies' market shares by calculating the amount of premium they wrote in the preceding calendar year. If the association incurs a deficit, the RPCJUA can impose "regular assessments" upon each of the member companies, based on their market shares. The companies must pay this assessment to the RPCJUA to cover the association's expenses. These regular assessments are capped at either 10 percent of the deficit or 10 percent of the total amount of statewide written premiums that private insurance companies wrote for the previous year, whichever is higher.

The insurance companies can recoup these regular assessments from their policyholders by filing for a rate increase with the Florida Department of Insurance. If a deficit exceeds the amount that can be covered through a regular assessment, the RPCJUA can impose "emergency assessments" on all property insurance policyholders in Florida. The policyholders

|

significant reduction in the number of policies in the RPCJUA, has enabled the association to have sufficient financing in place to cover a one-in-100-year hurricane. In the fall of 1996, when the RPCJUA stood at nearly 937,000 policies, the association's probable maximum loss from a one-in-100-year hurricane stood at $4.8 billion. As of February 1998, when the RPCJUA had been reduced to 372,000 policies, the one-in-100-year probable maximum loss was down to $2.75 billion. The law establishing the RCPJUA sets out some specific incentives for companies to remove policies from the association. The statute also gives the RPCJUA board of governors more general authority to establish additional incentives to hasten depopulation. The board has used this authority in crafting various depopulation programs, which have had a considerable impact on reducing the size of the RPCJUA. Had these depopulation efforts not been undertaken, the association estimates that it would have grown to 1.5 million or more policies, which would have made the RPCJUA the largest property insurer in the state. As of the end of February 1998, 22 companies had in force 676,797 policies that they had |

would be required to pay the assessments to their insurance companies, who would then turn the money over to the RPCJUA.

The emergency assessments are capped annually at 10 percent of the deficit, or 10 percent of the total amount of property insurance premium that private insurers wrote in Florida in the previous year, whichever is larger, plus interest, fees, commissions, required reserves, and other costs associated with financing the original deficit. The RPCJUA has imposed regular assessments for deficits totaling $17.7 million in 1994 and $22.8 million in 1995 (Adams, 1996). The RPCJUA recorded a modest surplus in 1996. In 1997, the surplus was $170.2 million on a GAAP reporting basis (GAAP = generally accepted accounting principles). The 1997 surplus was primarily the result of a one-time takedown of loss reserves in 1997 and the fact that no hurricanes hit Florida in 1996 and 1997. To date, the association has not imposed an emergency assessment.

Rate adequacy and the size of the residual market mechanisms have been an ongoing concern to the legislature. When the legislature could not agree on revisions to these mechanisms, it created the Legislative

|

removed from the association. The number of policies removed by these companies is actually higher, but in some instances the policies did not ultimately wind up with the companies—that is, policyholders shopped for coverage on their own, left the state, or chose to go without coverage, and so on. While the depopulation efforts have been successful, the RPCJUA continues to receive a heavy flow of new business each month that threatens to erode the success the association has achieved in reducing its policy count. As of early 1998, the RPCJUA was writing approximately 15,000 to 16,000 new policies monthly. As a result, the association has embarked on "keep out" programs designed to prevent policies from ever entering the RPCJUA. As a first step, the RPCJUA has solicited expressions of interest from insurers willing to write a meaningful amount of new business each month. The companies have been asked to provide information on the types of policies they are willing to write. Association producers have been requested to voluntarily submit applications for coverage to the companies for their underwriting review. To date, 11 companies have expressed interest in participating in these programs. |

Working Group on Residual Property Insurance Markets to fully examine the residual markets and make recommendations for legislative changes in the 1997 session. The primary purpose of the Legislative Working Group on Residual Property Insurance Markets was to develop recommendations for the legislature for a permanent residual market mechanism to replace the existing RPCJUA and the FWUA. The Working Group issued a final report in December 1996, recommending that the RPCJUA and the FWUA should remain separate, but work toward better coordination and eventual consolidation. The report said the boards of the two associations should develop a transitional plan for merging the two entities into a single residual market when the RPCJUA reaches 100,000 policies. The Legislative Working Group did not address the rate issues.

In an effort to allay concerns about its liquidity and its ability to pay claims after another hurricane, the association's board of governors in 1995 secured a $1.5 billion line of credit from a consortium of banks. In 1995, the board also authorized the purchase of catastrophe reinsurance at a time when several hurricanes simultaneously formed in the Atlantic and appeared to pose a threat to Florida. At that time, the board approved the purchase of $300 million in second-event coverage attaching after an aggregate of $1.175 billion in losses. In September 1997, the association purchased facultative reinsurance, excluding wind, for its commercial book of business covering locations valued in excess of $10 million. (See Chapter 2 for a discussion of different reinsurance treaties, including facultative.)

Because of an unintended problem created by wording in the 1996 special purpose homeowners' insurance company legislation, the RPCJUA would have been in default under its 1995 $1.5 billion line of credit if the Florida Department of Insurance (DOI) had allowed a special purpose homeowners' insurance company to form. Therefore the DOI issued an order stating that no such companies would be allowed as long as the possibility of a default existed. During the 1997 session, the Florida legislature amended the special purpose homeowners' insurance company statute and corrected the wording problem. As a result, the DOI order was rescinded.

Florida Windstorm Underwriting Association (FWUA)

This residual market mechanism, in existence since 1970, is the oldest in the state. It was created to assure the availability of windstorm

and hail insurance coverage for dwellings and other structures in designated eligible areas. The eligible areas are determined by the DOI and have traditionally been areas at high risk for wind damage (Gallagher, 1993).

If an insurer operates at a loss, the FWUA, like other residual market mechanisms, assesses those insurers operating in Florida. Assessments are based on a company's market share for the previous year, but can be reduced by credits derived from voluntarily writing wind coverage in FWUA-eligible areas. The total assessment for member companies may not exceed 10 percent of its statewide property premium writings in a given year.

The FWUA's loss exposure and the number of its policies in force have grown dramatically since Hurricane Andrew. From December 1992 to December 1994, policies in force increased by 198 percent. As of the end of 1996, loss exposure was estimated at $49 billion on 320,000 policies in force (PIPSO Reports, 1997). The growth in exposure is directly linked to the additional areas in Florida in which FWUA has begun to operate. In the aftermath of Hurricane Andrew, the DOI designated Dade and Broward Counties eligible for FWUA coverage. In the subsequent

Store destroyed by Hurricane Andrew, 1992 (FEMA).

months, the department also made other coastal areas eligible, which greatly increased the FWUA's exposure.

During the 1995 hurricane season the FWUA received about 9,300 claims caused by Hurricane Opal. These amounted to $145 million in losses, with approximately $70 million of that total reimbursed by reinsurance. The state's insurers were assessed $84 million for Hurricane Opal, which followed an October 1995 assessment of $33 million to cover Hurricane Erin losses (information provided via facsimile, FWUA, 1998).

In the wake of these economic impacts, the FWUA has reevaluated and determined that its fully indicated rate level should be 124.3 percent of the existing base rate. However, recognizing that policyholders need time for rate increases, the FWUA requested that the indicated rate be phased in gradually. As a result, the FWUA requested an overall rate increase of 67 percent. In March 1996, the Department of Insurance approved only a 31 percent rate increase effective with new and renewal policies on or after June 1, 1996. In August 1997 the FWUA filed a rate increase averaging 62 percent statewide, to be phased in over a period of three years (Adams, 1997). The insurance commissioner rejected the hike, however an independent arbitration panel recently overruled him and indicated that the FWUA can raise rates an average of 12 percent after August 1, 1998. Dade and Broward County rates could go up as much as 40 percent, which is the maximum increase allowed under the ruling (DeLollis, 1998).

THE REINSURANCE MARKET4

In the four years prior to Hurricane Andrew the world reinsurance market sustained a number of catastrophic losses in Europe, in the North Sea, and in Asia. Thus, the profound effect of Hurricane Andrew was felt in a market segment already suffering losses. The major impacts for primary company buyers of reinsurance in the year following Andrew included a severe shortage of catastrophe property reinsurance capacity and stricter policy terms and conditions, as well as sharp increases in property catastrophe cover rates due to a significantly increased demand against scarce supply.

These profound changes in the reinsurance market further reduced

A Florida hurricane (FEMA).

the primary carriers' willingness to write additional business, or even renew portfolios in force. The primary carriers were faced with an inability to pass along the increased reinsurance costs, and a concurrent inability to reduce or effectively manage catastrophe exposures. Under these conditions, the reinsurance market was viewed by the public and the Florida Department of Insurance as part of the problem rather than as a hoped-for solution. Reinsurers for their part were paying losses far beyond their expectations. It is doubtful that, as the magnitude of the Andrew loss became clear, the reinsurance market could have contributed significantly to a marketplace solution because of its own inability to diversify away the concentrations of Florida exposures in portfolios, even on a worldwide basis.

In response to the acute distress in the catastrophe reinsurance market, reinsurance intermediaries, aided by investment bankers, raised capital to create new reinsurers in Bermuda, virtually overnight. As pointed out in Chapter 2, more than $4.8 billion in private capital was raised, and in the course of 1994 eight monoline catastrophe reinsurers were formed (wind and earthquake coverage only). U.S. insurers and reinsurers were major backers of these new companies. The market opportunity available to new entrants was huge, and Bermuda offered an

excellent regulatory and tax-free climate in which to conduct the highly volatile catastrophe business.

While concerns were voiced initially about the durability of these new monoline catastrophe companies, the companies have proven to be successful, accounting for approximately 32 percent of worldwide catastrophe capacity in 1995; the U.S. markets provided 25 percent (Piper, 1995). It is worth noting that several of the Bermuda reinsurers have begun offering additional lines of coverage (liability excess, for example), either directly or through mergers or acquisitions.

In conjunction with limited post-Andrew capacity, reassessment of exposures and risk management programs by primary insurers and reinsurers have also stimulated exploration of other means of financing catastrophic coverage. In 1994 and 1995, reinsurers, investment bankers, and financial market traders moved to develop contingent capital, reinsurance, and derivative risk management products to add risk-bearing capacity from the capital markets. Depending upon the buyers' needs and willingness to accept basic risk, these new risk management products will provide an alternative, or a supplement, to traditional reinsurance (Reinsurance Association of America, no date). A key mechanism for the introduction of the capital markets is expected to be the creation of an index of catastrophe loss which will provide transparency to the capital markets investor. Much work and education remains to be done with investors, who must accept insurance risk as an asset class for inclusion in portfolios.

THE FUTURE

Each hurricane season highlights Florida's extreme vulnerability to the windstorm peril. Issues of insurance availability and affordability, as well as the solvency of primary insurers, remain the major concern of insurers, the state's insurance regulator, its legislature, and its insurance consumers. All the players are not necessarily in agreement as to how these elements are best balanced, however. It is clear that the basic problems brought to light by Hurricane Andrew remain the primary challenge six years later.

While this chapter concentrates on insurance mechanisms in the post-Andrew environment, it is important to note that they are not the only factors in improving Florida's lot. New ways to finance catastrophe losses (whether private or government), new risk management tools, and new insurance products must be met on equal terms by thorough disaster

planning, mitigation programs, public education, and a stronger built environment. Initiatives are currently under way that recognize the need for an approach where each stakeholder plays its role.

One such initiative is a proposal by the Florida Insurance Council (FIC) for an agreement establishing post-hurricane cooperation between the FIC, the state insurance department, and state and local emergency management officials. In addition, the governor created a Building Codes Study Commission to evaluate the current effectiveness of the Florida building code system and recommend any necessary reforms (Executive Order 96-234). In early 1998 this commission recommended that Florida should have one building code for statewide use which would be administered and enforced by local government building and fire officials (Five Foundations for a Better Built Environment, 1997).

Another initiative is the Florida Commission on Hurricane Loss Projection Methodology which was established by the state legislature in 1995 to examine the role of computer models in determining insurance rates. The commission developed a set of standards which a model must meet and hired a professional team to audit the modeling companies on site. By December 1997 the three principal models (those of Applied Insurance Research, EQECAT, and Risk Management Solutions) had all met the commission's standards and are approved for use in establishing insurance rates. The extent to which the Department of Insurance approves rate filings based on computer models is still unsettled (Mark Johnson, Director of the Institute of Statistics, University of Central Florida, personal communication, 1997).

The extent to which all of Florida's stakeholders come together and create successful collaborations will, in large measure, determine the state's ability to deal with the next Hurricane Andrew when it arrives, as it inevitably will. In the interim there will be ongoing tensions between the insuring public, the regulator, the legislature, and the insurance industry on the benefits and economic value of the changes already implemented, or under consideration. The economic future of the state of Florida, and its competitiveness, is at stake.