Paying the Price: The Status and Role of Insurance Against Natural Disasters in the United States (1998)

Chapter: 8 Regulation and Catastrophe Insurance

CHAPTER EIGHT

Regulation and Catastrophe Insurance

ROBERT KLEIN

THE PUBLIC HAS A VESTED interest in insurance. Hence, public choice plays a significant role in the financing and control of risk. Insurance companies, products, and markets are closely regulated, primarily by the states. Laws and public institutions significantly influence how society responds to a variety of perils that cause human and economic losses. This is especially true for natural hazards, where current private and public institutions (e.g., the legislature; the courts; federal, state, and local agencies; etc.) are struggling to accommodate the greatly increased risk of catastrophes caused by earthquakes, hurricanes, and other acts of nature. We need to understand how current regulatory policies are dealing with this crisis and consider more efficient and equitable approaches for mitigating and financing catastrophic losses.

Current insurance regulatory policies are driven by economic, political, ideological, and bureaucratic forces (see Klein, 1995; and Meier, 1988). The economic rationale for insurance regulation is based primarily on the market failures that are caused by imperfect information and by principal-agent problems associated with the fiduciary aspect of insurance contracts.

In theory, the regulators' job is to limit the insurers' risk of insolvency and ensure ''fair" market practices. Public policy is not forged in a political vacuum, however, and various factors have affected the scope and design of insurance regulation. Some of these factors include voters' perceptions and preferences regarding how the cost of risk should be shared among different groups.

Insurance regulation affects society's response to the risk of natural hazards in a number of ways. Regulation influences the supply and purchase of disaster insurance by controlling insurers' entry into and exit from the market, their capitalization, investments, diversification of risk, prices, products, underwriting selection, and trade practices. Government coverage requirements and information programs also affect individuals' and firms' demands for disaster insurance and hazard mitigation. Regulators are faced with the difficult challenge of assuring an adequate supply of "affordable" insurance coverage at a time when many insurers are seeking to significantly decrease their disaster risk exposure and increase their prices. The resolution of this dilemma could have substantial implications for the economies of many disaster-prone areas and the individuals who live in those areas.

This chapter assesses the role that insurance regulation has played in society's response to disaster risk, and identifies the issues that must be addressed in evaluating how regulatory policy might be modified to help lower disaster costs and support a more efficient and equitable way to finance them. The first section provides a brief overview of the structure of insurance regulation, focusing on its primary institutions and functions. This is followed by a detailed evaluation of the areas of regulation that are most relevant to insuring disaster risk and the options available to regulators to improve market conditions.

The chapter concludes with a discussion of how insurance regulation could be better coordinated with other government policies to achieve public goals. As noted in Chapter 1, insurance regulation interacts with many other areas of public policy that affect catastrophe risk. Hence, the implications of insurance regulatory policies for insurance market conditions could vary depending on the nature of other public and private sector actions that affect catastrophe risk.

STRUCTURE OF INSURANCE REGULATION

The current state regulatory framework for insurance is rooted in the early 1800s when insurance markets were generally confined to a

particular community. (For reviews of the history of insurance regulation, see Hanson et. al., 1974; Lilly, 1976; and Meier, 1988.) Local stock companies and mutual protection associations formed to provide fire insurance to property owners in a city. The high concentration of risk and large conflagrations led to highly cyclical pricing and periodic shakeouts when a number of insurers failed after a major fire (Hanson et al., 1974). The local orientation of insurance markets at the time led municipal and state governments to establish the initial regulatory mechanisms for insurance companies and agents.

Government control of insurers was initially accomplished through special legislative charters and discriminatory taxation, but these proved to be inefficient mechanisms as the number of companies grew and the need for ongoing oversight became apparent (Meier, 1988). New Hampshire appointed the first insurance commissioner in 1851. Insurance commissions were subsequently formed by various states to license companies and agents, regulate policy forms, set reserve requirements, police insurers' investments, and administer financial reporting. Price regulation in the early 1900s was essentially confined to limited oversight of property-casualty industry rate cartels. Through the years, insurance department responsibilities grew in scope and complexity as the industry evolved. Price regulation also changed as industry rating bureaus were transformed into advisory organizations and insurance pricing became very competitive.

Several major forces appear to have heavily influenced the evolution of insurance regulatory functions and institutions. One factor has been the dramatic growth and increasing diversity of insurance products and the types of risks that insurers have assumed. Increased competition among insurers and alternative risk-financing mechanisms have imposed additional pressures on the industry and its regulators. Competitive pressures and consumer demands prompted insurers to incur increased financial risk during the 1980s, which resulted in a significant increase in insurer failures and guaranty fund costs (Klein, 1995). This increased risk has been coupled with the geographic extension of insurance markets nationally and internationally, which has increased the interdependence among regulatory jurisdictions.

The relationship between the federal and state governments has been a critical factor in the evolution of insurance regulation and also is very pertinent to disaster insurance issues. Throughout the industry's development, the states and the federal government have wrestled over its regulation. This tension is fed by the interstate operation of many insurers

and their significant presence in the economy. On numerous occasions, the federal government has sought to exert greater control over the insurance industry. The states have fought back aggressively to retain their authority, backed by the industry. (See Meier, 1988, and Advisory Commission on Intergovernmental Relations, 1992, for reviews of various attempted federal interventions into insurance regulation.)

The primacy of the states' authority over insurance was essentially affirmed in various court decisions until the Southeastern Underwriters case in 1944 [United States v. South-Eastern Underwriters Ass'n, 322 U.S. 533 (1944)]. In that case, the U.S. Supreme Court ruled that the commerce clause of the U.S. Constitution applied to insurance and that the industry was subject to federal antitrust law. This decision prompted the states and the industry to join forces behind the passage of the McCarran-Ferguson Act in 1945, which delegated regulation of insurance to the states, except in instances where federal law specifically supersedes state law.

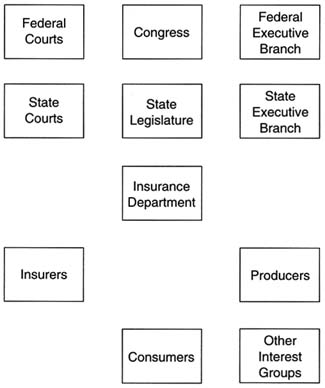

The federal government has affected state insurance regulatory policy and institutions in several ways. In a number of instances, Congress has instituted federal control over certain insurance markets or aspects of insurers' operations that were previously delegated to the states (e.g., the provision of liability insurance by risk retention groups, employer-sponsored health plans, etc.). In other cases, the federal government has established insurance programs, such as flood and crop insurance, that are exempt from state regulatory oversight. In addition, the federal government has set regulatory standards that the states are expected to enforce (e.g., Medicare supplement insurance). Finally, federal policies in a number of other areas such as antitrust, international trade, law enforcement, taxation and expenditures, and the regulation of banks and securities have significant implications for the insurance industry and state regulation. See Figure 8-1 for a schematic representation of the parties involved in the regulatory process. Arrows are not drawn between the boxes because all of the parties are connected with each other in some ways.

Authority of State Insurance Commissioners

State insurance commissioners have the principal authority to regulate the business of insurance within their jurisdictions. This authority encompasses: licensing insurers and producers; oversight of insurers' financial structure, investments, transactions, and operations; approval of

insurance products and prices; and policing insurer and producer trade practices. The insurance commissioner is authorized to take direct control of an insurer if its financial condition becomes hazardous to policyholders' interests. Insurance commissioners' authority is broad and can have significant effects on insurance markets.

At the same time, insurance regulatory agencies are part of a larger governmental structure that helps to set and implement policy as well as constrain regulatory actions. Regulatory policy is formulated collectively by the insurance commissioner, the legislature, and the courts. The state legislature establishes the insurance department, enacts insurance laws, approves the regulatory budget, and may review and approve insurance regulations. Insurance departments are part of the state executive branch, either as a stand-alone agency or as a division within a larger department. Commissioners must often utilize the courts to help enforce regulatory actions, and the courts in turn may restrict regulatory action.

FIGURE 8-1 The insurance regulatory system.

Each insurance department also must coordinate with other state insurance departments in regulating multistate insurers, and must rely on the National Association of Insurance Commissioners (NAIC) for advice as well as some support services. As discussed above, the federal government overlays this entire structure, delegating most regulatory responsibilities to the states, while retaining an oversight role and intervening in specific areas. (In practice, the federal government has left the principal insurance regulatory functions to the states.)

Most commissioners are appointed by the governor (or by a regulatory commission) for a set term or "at will," subject to legislative confirmation. Typically, the governor and other higher administration officials do not interfere with daily regulatory decisions, but may influence general regulatory policies and become involved in particularly salient issues. Twelve states elect their insurance commissioners, who are autonomous in the sense that they do not take orders from the governor, but they must still cooperate with the administration and legislature in order to achieve their objectives. Elected commissioners directly cultivate voters' political support, while appointed commissioners do this indirectly as part of their administrations.

Principal Regulatory Functions

Insurance regulatory functions can be divided into two primary categories: solvency regulation and market regulation. Solvency regulation seeks to protect policyholders and the public against the risk that insurers will not be able to meet their financial obligations. Market regulation attempts to ensure fair and reasonable insurance prices, products, and trade practices. Solvency and market regulation are closely related and must be coordinated to achieve their specific objectives. Regulation of rates and market practices will affect insurers' financial performance, and solvency regulation constrains the prices and products that insurers can reasonably offer.

All U.S. insurers are licensed in at least one state and are subject to solvency and market regulation in their state of domicile and in other states in which they are licensed to sell insurance. If an insurance company is licensed in a state, it is classified as an admitted insurer; an insurer who operates in a state but is not licensed is classified as a nonadmitted insurer. Reinsurers domiciled in the United States also are subject to the solvency regulation of their domiciliary state. Some U.S. and non-U.S. insurers write certain specialty and high-risk coverages on a nonadmitted

or surplus lines basis that are not subject to price and product regulation. Insurance commissioners still control entry of nonadmitted insurers into their states by imposing minimum solvency and trust requirements, and regulate surplus lines brokers.

Solvency Regulation

The public interest argument for the regulation of insurer solvency derives from inefficiencies created by costly information and principal-agent problems (Munch and Smallwood, 1981).1 If an insurance company becomes insolvent, any unfunded obligations to its policyholders do not become the personal liability of the insurance company's owners. (This is the case with virtually all organizational structures used by insurers; the only exception is Lloyd's organizations.) Hence, owners of insurance companies are not necessarily motivated to maintain a high level of financial safety because their personal assets are not at risk to cover these obligations.

It is costly for consumers to properly assess an insurer's financial strength in relation to its prices and quality of service. Consequently, consumers may unwittingly purchase a policy from a financially weak or high-risk insurer. This diminishes an insurer's incentive to limit its financial risk if its behavior is not rewarded by increased demand and consumers' willingness to pay a higher price for its services. Many insurers may have other reasons to limit their financial risk. For instance, many insurers have a significant amount of franchise value (i.e., investments that will yield long-run profits if the insurer stays in business) that will be lost if the insurer becomes insolvent. However, some insurers may be motivated to take advantage of consumers' ignorance and incur a high probability of ruin in return for higher profits.

Principal-agent conflicts also arise after insureds have purchased policies from insurers. It is difficult for policyholders to monitor and control the behavior of their insurers once the policyholders have paid premiums in return for the insurers' promise to pay claims covered under their contracts. Hence, some insurers may be encouraged to increase their financial risk beyond a level acceptable to their policyholders and jeopardize

their ability to meet future claims obligations. Insurers can increase their financial risk in many ways, including investing in high-risk assets, underpricing to attract new business, establishing inadequate loss reserves, failing to adhere to appropriate underwriting guidelines, failing to purchase adequate reinsurance, paying excessive dividends to owners, and incurring an excessive exposure to catastrophic losses. These actions can increase short-run profits and returns to owners of an insurer at the expense of the insurer's long-run solidity and its capacity to meet its obligations to policyholders.

Without regulation, such actions taken by insurers could result in an excessive number of insolvencies. This is not to say that all or even most insurers would choose to incur excessive risk if left on their own. However, experience has indicated that some will. For example, nine insurers failed due to losses from Hurricane Andrew because of their relatively low levels of capital and their failure to take adequate precautions to protect themselves against catastrophic losses. It is this kind of insurer that regulators must identify and control. Solvency regulation is intended to impose an upward bound on the degree of insolvency risk in accordance with society's preference for safety.

Regulators protect policyholders and society in general against excessive insurer insolvency risk by requiring insurers to meet certain financial standards and to act prudently in managing their affairs. State statutes require insurers to meet minimum capital and surplus standards and financial reporting requirements, and authorize regulators to examine insurers and take other actions to protect policyholders' interests. Solvency regulation polices various aspects of insurers' operations, including capitalization, pricing and products, investments, reinsurance, reserves, asset-liability matching, transactions with affiliates, and management.

If an insurer fails to comply with regulatory requirements and/or its financial condition becomes hazardous to policyholders' interests, regulators are authorized to intervene in various ways to control the insurer's activities. If an insurer becomes severely impaired or insolvent, regulators will place it in receivership and either rehabilitate, sell, or dissolve the company. State guaranty funds, financed by uniform pro rata assessments on the premiums of solvent insurers, cover most of the unfunded obligations of failed insurers to policyholders and claimants. While guaranty funds provide a level of financial security for policyholders and claimants, they also create a moral hazard problem that must be controlled by effective solvency oversight by regulators.

Market Regulation

Market regulation encompasses a diverse set of areas and is approached somewhat differently by the various states. Rates and policy forms are subject to some form of regulatory approval in virtually all states. The traditional explanation for regulation of insurance prices also involves costly information and solvency concerns (Hanson et. al., 1974; Joskow, 1973). Some insurers may charge inadequate prices to grab a larger volume of business and increase their short-run profits at the expense of their long-run financial solidity. Some consumers will buy insurance from low-price carriers without properly considering the greater financial risk involved. According to this theory, poor incentives for safety could induce a wave of "destructive competition" in which all insurers are compelled to cut their prices below costs to retain their market position. Thus, regulators must impose a floor under prices to prevent the market from disintegrating because of a downward spiral of price cutting and insolvencies.

The desire to make sure premiums were high enough against particular risks governed insurance rate regulation until the 1960s, when states began to disapprove of requested price increases in lines such as personal auto and workers' compensation. The rationale offered for restricting insurance price increases is that the costs consumers incur in shopping for insurance products impede competition and lead to excessive prices and profits by insurers (Harrington, 1992). Further, imperfect consumer information and unequal bargaining power between insurers and consumers can expose potential policyholders to abusive marketing and claims practices of insurers and their agents.

It also can be argued that it is costly for insurers to ascertain consumers' risk characteristics accurately, giving an informational advantage to insurers already entrenched in a market and creating barriers to entry that diminish competition and result in much higher prices than would be expected based on the insured risk (Cummins and Danzon, 1991). In this view, the objective of regulation is to enforce a ceiling that will prevent prices from rising above a competitive level and to protect consumers against unfair market practices.

In addition, the public may express a preference for regulatory policies to guarantee certain market outcomes consistent with social norms or objectives. For example, most states require drivers to purchase auto liability insurance, and this increases political pressure to suppress auto insurance prices to keep them affordable for all drivers. Similarly, the

necessity for homeowners' insurance may increase public pressure on regulators to keep homeowners' rates low, even in areas subject to high catastrophe risk.

State laws typically require that rates not be inadequate, excessive, or unfairly discriminatory. For the personal property-casualty lines, approximately half of the states require rates to be approved before they go into effect. Other states allow insurers to implement rates on personal lines without prior approval, placing greater reliance on competition to regulate prices. Except for workers' compensation and medical malpractice, commercial property-casualty lines in most states are also subject to a competitive rating approach. Under such a system, regulators typically retain authority to disapprove proposed rate increases if they find that competition is not working, although in practice such a finding rarely occurs. [This residual authority is provided in the NAIC's Property and Casualty Model Rating Law (File and Use Version), which many states have adopted. NAIC publishes its model laws in a compilation Model Laws: Regulation and Guidelines , which can be obtained from the NAIC.]

Historically, after the passage of the McCarran-Ferguson Act, many property-casualty insurers adopted rates filed by an advisory organization (e.g., Insurance Services Office) or filed deviations from advisory rates. Recently, the states have gone to a system in which advisory organizations file prospective loss costs. These loss costs represent expected claims payments and associated claims adjustment expenses. Historical loss costs are developed and trended forward to develop prospective loss costs applicable to the policy period for which the advisory loss costs are filed.2 The advisory loss costs include a provision for catastrophe losses, which are modeled because historical experience along provides an insufficient basis upon which to estimate future catastrophe losses.

Insurers are allowed to file multipliers to advisory loss costs, which include provisions for adjustments to the advisory loss costs, expenses, profit and investment income, or full rates as before. For example, an insurer can accept the advisory loss costs and file a multiplier of 1.4 to

"load" the advisory loss costs for its expenses and profits. In this instance, the insurers' rates would be equal to the advisory loss costs multiplied by the factor of 1.4. Additionally, the insurer could also adjust its multiplier upward (or downward) on the basis that its losses will be higher (or lower) than the advisory loss costs. Alternatively, an insurer might choose to file full rates rather than a multiplier to be applied to the advisory loss costs.

The loss costs approach to advisory filings is intended to promote independence and competition among insurers by removing full advisory rates as a potential focal point for insurer pricing. It is presumed that loss costs will tend to be similar among insurers and less subject to discretion. (Insurer differences and discretion with respect to expected loss costs should only arise from differences in underwriting stringency, risk portfolios, and loss control efforts.) The analysis of industry loss costs by advisory organizations is perceived as having informational value for insurers and the public that outweighs any negative effect it may have on competition. On the other hand, insurers' loadings for expenses and profits are perceived as subject to greater discretion based on insurers' service levels, efficiency, and competitive considerations. Hence, the advisory filing of a common loading factor or full rates would be perceived as having a greater detrimental effect on competition than any efficiencies that would be gained.

In addition, insurers must obtain approval for the products that they sell and, specifically, the policy forms that they use. Regulators seek to ensure that policy provisions are reasonable and fair and do not contain major gaps in coverage that might be misunderstood by consumers, or that might be inconsistent with state coverage requirements. For example, regulators would be unlikely to approve homeowners' insurance policies that would exclude coverage for windstorm losses unless these losses are covered by another mechanism.

Regulators also police insurers' and agents' sales and underwriting activities to make sure that they adhere to certain standards and that claims are handled according to the provisions of insurance contracts. The objective is to prevent abusive practices—for example, misleading presentations on insurance coverage or the failure to pay legitimate claims on a timely basis—that take unfair advantage of consumers. Responding to consumer complaints and performing market conduct examinations are the primary ways in which insurance departments regulate market practices.

State insurance departments perform various other functions. The

insurance commissioner is generally held accountable for the overall performance of insurance markets under his or her jurisdiction, and this leads to a number of activities to support market operations. Enhancing consumer information about insurers' prices, products, and financial strength is a critical function, given the heavy reliance on competition to ensure good market performance. Other functions performed by insurance departments include agent licensing and education, adjuster licensing (in some states), anti-fraud enforcement, coordinating market assistance plans, collecting premium taxes, and providing public information. In addition, insurance commissioners frequently advise legislators on laws affecting public policy on insurance. For example, an insurance commissioner may take an active role in promoting programs to mitigate catastrophe losses.

Regulatory Constraints

Insurance is a large and complex business; state regulators face significant challenges in achieving their objectives in the face of limited information. Regulators must establish and implement rules governing insurance transactions based on incomplete knowledge about the nature of the risk transferred and its cost. At best, regulators can attempt to enforce general parameters on market activity and prevent the most flagrant abuses without creating significant market distortions inconsistent with public objectives. This necessitates considerable reliance on market forces, even in jurisdictions with extensive regulatory restrictions.

The more regulators seek to control insurance market transactions, the greater the demands on their human and technological resources. The cost of regulation is further increased by its administration at the state level, which limits the economies of scale that individual insurance departments can achieve (Grace and Phillips, 1996). Maintaining a regulatory infrastructure—which consists, for example, of investments in databases and information systems—involves certain fixed costs, as well as variable costs that increase less than proportionately with the number of insurance transactions regulated. These costs could be spread over a larger volume of business if insurance regulation were consolidated into one or several agencies nationwide. Another example of the inefficiency of state insurance regulation is the fact that an insurer must make separate rates and forms filings in every state in which it does business, and regulators in each state must review these rates and filings, thus duplicating the review process that regulators in other states are performing.

Regulation imposes further indirect costs on insurers in complying with regulatory requirements.

The states also face the challenge of coordinating their actions and reconciling their economic interests in the oversight of multistate and multinational insurers. On average, 80 percent of the premiums in a state are written by insurers that are domiciled elsewhere. Hence the commissioner must rely on these other states to regulate nonadmitted companies' actions with respect to potential insolvency (Klein, 1995). A state focuses its regulatory oversight on the solvency of its domestic companies and the market activities of all insurers operating within its boundaries.

Some analysts contend that many insurance departments lack the expert staff and technology necessary to perform their regulatory responsibilities (see U.S. GAO, 1979). These resources are particularly relevant to the regulation of disaster insurance markets, which requires utilization of considerable scientific and actuarial expertise. Many insurance departments do not possess an abundance of staff with these skills, although they can contract with outside consultants to analyze rate filings. Still, departments face budget constraints that limit the level of analysis they can perform.

Department staff levels vary significantly depending on the size of the markets they regulate and other factors (NAIC, 1997). In 1996, the number of state insurance department personnel, excluding the four U.S. territories, ranged from 23 in South Dakota to 1,056 in California. Total full-time equivalent staff for all departments combined amounted to 9,649, in addition to 1,661 contract staff. For fiscal year 1998, state department budgets ranged from $1.2 million in South Dakota to $122.4 million in California, with a total combined budget for all departments of approximately $753.7 million. Insurance departments employed a total of 90 property and liability actuaries and 354 property and liability rates/forms analysts (not counting contract staff). Many of these analytical resources are concentrated in the larger states, which coincidentally possess a large portion of the risk of natural disasters.

In an effort to overcome some of their jurisdictional boundaries and diseconomies, the states have utilized the NAIC extensively to coordinate their efforts and pool their resources to improve the efficiency of insurance regulation. The NAIC is a private, non-profit association of the chief insurance regulatory officials of the 50 states, the District of Columbia, and the four territories. It was established in 1871 to coordinate the supervision of multistate companies within a state regulatory framework, with special emphasis on insurers' financial condition.

The NAIC functions in an advisory capacity and as a service provider for state insurance departments. Its objective is to allow states to focus their resources on regulation of their markets and the solvency of their domiciliary companies, utilizing support services from the NAIC. The NAIC has several committees and working groups that evaluate disaster insurance issues. These efforts help to overcome some of the structural challenges that the states face in regulating a global insurance industry.

REGULATION AND DISASTER RISK: ISSUES AND OPTIONS

The market problems and market failures with respect to catastrophe risk and insurance pose a number of issues for regulation. To what extent can regulators correct or offset market failures to improve economic efficiency and equity in the provision of catastrophe insurance? What limitations do regulators face? Are there some market problems that would be more effectively addressed by private or public mechanisms outside of regulation? Can regulation potentially worsen rather than improve market conditions? In reviewing the potential benefits and pitfalls of insurance regulation, we need to thoroughly understand the nature of the problems that it intends to correct and whether regulators can reasonably be expected to correct these problems, given economic and political realities.

Regulation and Its Effect on Availability and Price

Regulators are subject to various limitations in seeking to influence the availability and price of insurance in response to economic and political pressures. If regulators suppress rates below costs, insurers will be disinclined to write insurance policies voluntarily. This will diminish the availability of coverage. Regulatory restrictions on policy terminations may delay insurers' withdrawal from a market, but they also may discourage entry and decrease the supply of insurance in the long run. Regulators pressured to constrain price increases and cutbacks in coverage in the short run face the prospect of causing more severe market dislocations in the long run.

Policymakers may seek to justify market restrictions on the basis of equity considerations (e.g., equalizing rates between low- and high-risk areas), but such efforts are likely to impair market efficiency by distorting

sellers' and buyers' decisions. Moreover, there are different opinions on whether uniform rates are more equitable than actuarially fair rates that vary with the level of risk.

An individual state's ability to ensure adequate insurance coverage of catastrophe perils and allocate the cost of this coverage among different risks also is limited by its jurisdictional boundaries. States are limited to pooling catastrophe risks within their boundaries. A state cannot create an insurance pool that includes exposures outside its boundaries and force insureds in other jurisdictions to subsidize its insureds.

However, the division of the principal solvency and market regulation responsibilities between states can lead to some inconsistencies between these policies and create externalities between states. This externality problem arises from the fact that the gains that result from regulatory actions that increase the risk of an insurer's insolvency can be distributed in a different manner among states than the costs arising from the insolvency would be distributed. The costs of an insurer's insolvency are distributed among states proportionate to the insurer's volume of business, but the gains from high-risk regulatory actions accrue only to those states that engage in these actions. For example, some states with a high exposure to natural disasters may seek to externalize some of their costs or risk to other states by suppressing insurers' rates or attempts to reduce their exposures. If an insurer becomes insolvent because of these actions, the insolvency costs will be distributed among all states in which the insurer does business, but only the states that suppressed the insurer's rates and underwriting will achieve any gains.

Competition and regulation in other jurisdictions and federal budgetary restrictions check this behavior, but these checks are imperfect, particularly in the short run. For instance, if an insurer would attempt to raise its rates above its expected costs in Iowa to offset its regulation-suppressed rates in Florida, other companies could take business away from the insurer in Iowa by charging lower rates that would not contain a subsidy for Florida insureds. The federal government also may limit the disaster assistance it will provide to a state. However, as explained above, a state can increase the insolvency risk of an insurer and externalize a portion of this increased risk to other states. States on the losing end of this practice can only discourage it by exerting moral suasion on the ''offending" regulators and forcing insurers to structurally insulate their operations and surplus from claims from high-risk states. It is unlikely that such drastic action would be taken until an insurer's vulnerability became very apparent and forced regulators to respond.

Control of Market Entry and Exit

Regulatory policy and issues in this area vary, depending on whether the insurer is admitted (licensed in the state), nonadmitted (unlicensed), or alien (domiciled in a foreign country).

Admitted Insurers

The states control the market entry of insurers primarily to limit insolvency risk and enforce the regulation of insurers' market practices. Capital requirements for licensing are relatively low, but other aspects of the processing of licensing applications can significantly slow entry. Entry barriers that do not protect consumers impede competition unnecessarily and restrict the supply of insurance. Easing entry barriers could help new insurers to enter catastrophe insurance markets and write business shed by insurers which have an excessive geographic concentration of catastrophe exposures.

Easier entry could be facilitated through greater standardization of procedures and interstate cooperation in admitting nondomestic insurers. Indeed, some states, such as Hawaii, have explored the use of the NAIC's accreditation program as a means to expedite the admission of insurers domiciled in certified states. Reciprocal agreements among states in the admission and regulation of nondomestic companies also could reduce entry barriers. Several states are currently developing standardized and expedited licensing procedures that consider where an insurer is already domiciled and licensed. At the same time, states with severe availability problems should guard against a tendency to set their entry and solvency requirements too low, which could have adverse consequences for consumers in the long run.

In recent years, regulators also have attempted to restrict exit to some degree, particularly with respect to the personal lines and catastrophe risks. Exit refers to insurers' efforts to shed some exposures within a state, as well as efforts to completely withdraw from one or more lines within a state. Regulators may attempt to delay or prevent insurers' withdrawal from a market to maintain the availability of insurance coverage, but these efforts could prove to be counterproductive in the long run if they discourage entry. Exit can be costly for an insurer to the extent that it will lose its investments in establishing a distribution system, as well as its reputation and its relationships with its policyholders. Indeed, the costs of full exit from a state by a multiline, multistate company tend to make it a permanent decision and discourage insurers from such exits.

This gives regulators some leverage in seeking to keep insurers in a market, but there is a limit to regulators' power in this regard.

At most, regulators can slow and increase the cost of exit but not ultimately prevent it. Many states today impose some restrictions on exits in the form of prior notice requirements on policy cancellations and nonrenewals. Insurers serving multistate commercial risks will have a higher cost of exit than insurers that can exit a state without adversely affecting their ability to cover risks in other states; this increases the economic rent that a state can extract before it forces an insurer out of the state.

If insurers attempt to shed exposures after a catastrophe, regulators can impose moratoriums on policy terminations, such as in Florida after Hurricane Andrew, or force an insurer to exit from all lines, not just lines chosen by the insurer. (Florida extended the moratorium in 1996 to business that insurers placed on their books in anticipation of the moratorium being lifted.) Such moratoriums can discourage insurers from writing new business because the moratoriums limit the insurers' flexibility in shedding business if it proves to be necessary to reduce their concentration of risk exposure.

It is possible that exit restrictions could force an insurer into insolvency, but in practice this has rarely occurred. In most cases, insurers, with the help of the courts, can exit the market before they become insolvent. Of course, this is less likely in the event of a catastrophe, which can cause a rapid change in an insurer's financial condition before it is able to withdraw. In extreme cases, insurers may respond to severe exit barriers by establishing a single-state company to insulate the rest of its business from losses within a state.

Some regulators believe there is a need for regulatory restrictions on the speed of insurers' withdrawal or adjustment of their concentration of exposures. This presumes that some insurers "overreact" to perceived increased catastrophe risk and withdraw from a market "too quickly," resulting in an excessive degree of market instability. This could be true, but it has not been demonstrated by empirical analysis. What principles should govern regulatory exit restrictions and how far should they go? At what point would the social cost of exit restrictions exceed the social gains from promoting greater market stability? As an example of exit restriction, a one-year limitation on policy terminations in high-risk areas following a catastrophe could give insurers and regulators the opportunity to take stock of the situation and determine what long-run adjustments are necessary in terms of insurers' concentration of exposures.

Such adjustments, based on sound risk analysis, would allow the market to reach a sustainable equilibrium without attempting to permanently anchor insurers to an excessive concentration of exposures in high-risk areas. In the interim, regulators and consumers could make provisions for alternative sources of coverage.

Without further analysis, it is not possible to determine whether this policy would be more efficient than placing less severe restrictions on insurers' ability to terminate policies after a disaster. Short-term restrictions are more likely to increase efficiency if: (1) insurers' decision-making processes are flawed to the extent that they overreact to external and internal pressures to avoid risk after a disaster; and (2) abrupt decreases in the supply of insurance impose significant transaction costs on insureds, who must seek other sources of coverage or retain more risk than they would prefer. However, long-term or extended moratoriums on policy termination are likely to be counterproductive in terms of their negative effect on entry and on insurers' willingness to write new policies.

Even if regulatory exit restrictions provide some stability to the market in the short run, they can lead to increased market concentration and a decreased supply of coverage in the long run. Exit restrictions also can adversely affect the policy objective of limiting insurers' insolvency risk. Indeed, regulatory constraints on entry and exit could interfere with the market's movement toward an optimal level of risk diversification among insurers. Ideally, as some insurers reduce their excessive concentration of exposures in high-risk areas, other insurers would see opportunities and come in to fill the gap. This process will not guarantee "affordable" rates but it should decrease the "risk premium" that insurers require to cover catastrophe perils.

Consequently, in the long run, regulatory restrictions on the movement of insurers and their capital could have the perverse effect of decreasing availability and increasing prices. If regulators place severe, long-term restrictions on exits, new insurers will be discouraged from entering the market because of fear of the high cost of exit if they need to withdraw. At the same time, insurers already present in the state will find ways to gradually decrease their exposures (even if it is costly to do so) and require higher rates to compensate for the excessive level of risk they are forced to retain. Alternatively, regulators may wish to explore ways in which insurable risks might be more smoothly transferred from insurers with high concentrations of catastrophe exposures to insurers with low concentrations. As shown in Chapter 5, after Hurricane Andrew, Florida forced insurers to renew most of their homeowners' policies. The

state has also been forging agreements with insurers to encourage risk transfer.

Nonadmitted and Alien Insurers

Nonadmitted and alien insurers present a special issue. Today these insurers tend to fill gaps in regular markets and cover risks eschewed by admitted insurers. While regulators impose only minimal restrictions on nonadmitted carriers, some barriers still exist, and they could be evaluated in terms of their impact on the availability of disaster-related coverages. Although the role of nonadmitted insurers is understood and accepted in certain commercial lines, what potential role do they have, if any, to provide additional capacity in the personal lines in catastropheprone areas? Would it be necessary and feasible to increase regulatory protections for personal risks purchasing coverage from nonadmitted insurers? Is it possible to allow personal risks to form groups or cooperatives to purchase personal lines coverage from nonadmitted carriers? The use of groups would presumably enhance consumers' bargaining power and ability to protect themselves from transactions adverse to their interests. However, some regulators are concerned that group policies and group marketing can be used to discriminate against risks considered to be undesirable by insurers. Also, policymakers would need to consider the problems created by the insolvency of nonadmitted carriers insuring personal lines risks that would not be protected by guaranty funds.

Regulatory restrictions hamper the ability of alien insurers to enter state insurance markets on an admitted basis. To do so, these non-U.S. companies must acquire a U.S. company, establish a U.S. branch, or utilize a particular state as a port of entry with quasi-domiciliary regulatory responsibilities. Within the structure of state insurance regulation, certain requirements are necessary to enable regulators to enforce alien insurers' compliance with state laws and regulations. It might be possible to establish cooperative arrangements among states and foreign jurisdictions to ease the entry of non-U.S. insurers on an admitted basis to serve primary commercial and personal lines markets while preserving necessary regulatory protections. But are alien insurers interested in serving U.S. markets on an admitted basis? And is it possible to allow them to do so, yet maintain a level playing field with respect to their competition with U.S. insurers? Some alien insurers could have advantages in terms of broader geographic diversification, access to capital and reinsurance, and expertise in insuring catastrophe risk. Alien insurers could be a significant

source of additional catastrophe insurance if regulatory barriers were eased, but they also could leverage their entry into other lines of insurance which might create economic problems for U.S. insurers. Increased competition from alien insurers could increase financial risk for some U.S. insurers or force them out of business.

Alternative Insurance Mechanisms

The states and the federal government also control the formation and use of "alternative risk-financing" mechanisms such as self-insurance, captives, and risk retention groups. What potential role do these mechanisms have in addressing disaster risk and how should they be regulated? Presumably, such mechanisms would only be functional for catastrophe risk if they allow for risk-spreading across different types of risk, different geographic areas, and over time. The nature of catastrophe risk—infrequent, severe, and concentrated losses—may pose problems for alternative mechanisms that could not efficiently diversify this risk. For example, a reciprocal insurance arrangement for a group of homeowners living in close proximity to each other might work well for auto liability risk, but not for earthquake or hurricane risk. On the other hand, a firm that owns a number of establishments dispersed throughout the country might be in a better position to self-insure, or use a captive to finance its catastrophe risk exposure. Alternative mechanisms may be the most viable for groups and firms that can diversify catastrophe risk within the group or firm, take advantage of favorable tax treatment of accumulated reserves, and/or buy excess reinsurance.

It has been suggested that banks' entry into insurance could ease market availability problems. If banks' insurance activities are confined to distribution, entry costs could be lowered for insurers seeking to write more business in underserved markets subject to catastrophe risk. If banks' activities are expanded to insurance underwriting, this could add capacity to catastrophe insurance markets. However, changes in state and federal law would be required to allow banks to underwrite insurance risk, and this would raise a host of logistical, policy, and regulatory issues. Underwriting disaster insurance is risky and requires considerable expertise. Hence, it may be the least suitable line for bank entry. Also, the correlation of a bank's exposure to insurance losses and loan defaults stemming from a natural disaster would further concentrate its risk. In reality, banks may have little interest in assuming the catastrophe risk exposures that insurers are seeking to shed.

Financial Regulation

Financial regulation and the other areas of regulation are closely tied. In general, more stringent financial regulation means that insurers are forced to offer less favorable terms on insurance contracts (i.e., insurers have to charge higher prices or reduce coverage). On the other hand, regulatory attempts to force insurers to offer more favorable terms to consumers (e.g., lower prices, more generous coverage, etc.) can have a negative effect on solvency. For example, higher capital requirements may force an insurer to raise its rates; regulatory suppression of rates below costs can threaten an insurer's solvency. Thus, financial regulatory policy can affect disaster insurance market conditions, and regulation of disaster insurance markets can affect insurers' solvency.

Capital Requirements

There is an inherent tension between the regulatory objectives of limiting insolvency risk and ensuring available and affordable coverage. Regulators would generally agree that solvency is their first priority, but the availability and affordability of insurance coverage also are important objectives, and these objectives must be balanced consistent with market realities and societal preferences. For instance, regulators could virtually ensure that no insurer would ever fail, by imposing very stringent capital requirements and other risk limitations. However, such a policy may decrease the supply of insurance and raise prices to socially unacceptable levels. In practice, regulators and the marketplace tolerate some degree of insolvency risk in return for a greater supply of insurance. Guaranty funds have been established to diversify this residual insolvency risk across all policyholders, but the "flat pricing" of insolvency guarantees can impose cross-subsidies and encourage excessive risk-taking by some insurers. Regulators could force a suboptimal solvency-supply solution inconsistent with social preferences.

This tension between the goals of solvency of insurers and available, affordable coverage for consumers is exacerbated by the division of primary regulatory responsibilities for regulating a multistate insurer's solvency and market practices between domiciliary and non-domiciliary states. Under "normal" market circumstances, when coverage is readily available and premiums are relatively affordable, a non-domiciliary state may regulate the solvency of a nondomestic insurer more stringently than would a domiciliary state. This is because the domiciliary state has the most to gain from the growth of the company in terms of employment and tax

revenues, while the risk of insolvency is distributed among all the states in which the company writes business (Klein, 1995). However, when a state is suffering from severe availability problems and cost pressures, it may favor less stringent solvency regulation of its nondomestic insurers to increase the supply of insurance and relieve pressure on its market.

For instance, a high-risk state may prefer that other states ease catastrophe risk limitations on its nondomestic companies to avoid a significant number of policy terminations. While such a measure might increase the long-term insolvency risk of these insurers, the regulators in a high-risk state may give more weight to the short-term political gains to be had from maintaining the availability of insurance coverage. If an insurer does become insolvent because of its excessive concentration of catastrophe exposures in high-risk states, the current guaranty fund system distributes the insolvency costs among all of the states in which the insurer does business. Hence, all of the other states bear a portion of insolvency risk from catastrophes in the high-risk state, but do not reap the corresponding short-term political benefits from maintaining the availability of coverage. The potential difference in interests between states with respect to an insurer's catastrophe risk could lead to conflicts between the states in how they regulate the insurer.

Areas related to solvency regulation that are likely to have the greatest significance for disaster insurance market conditions include capital requirements, investments, reserves, risk limitation, and reinsurance. As mentioned above, state capital requirements are relatively low and, hence, would not be expected to have a significant effect on the supply of disaster insurance. The states have recently implemented risk-based capital (RBC) requirements that vary according to an insurer's volume of business and other risk factors. While RBC requirements are typically higher than state-fixed minimum capital requirements, RBC requirements are still relatively low (very few insurers fail to meet them) and do not consider catastrophe risk (Cummins et al., 1995; and Barth, 1996). Hence, the introduction of RBC has likely had a minimal effect on entry or insurers' risk of insolvency due to catastrophic losses. For example, all nine insurers that failed because of Hurricane Andrew would have satisfied NAIC RBC requirements prior to their insolvency had they been in effect.

Other Financial Regulation

Regulatory requirements governing investments generally address proper valuation of investments, credit quality, and diversification.

Stricter restrictions on insurers' investments generally lower their investment return and hence require higher insurance prices or some other offsetting action. However, some regulatory restrictions might also hamper insurers' ability to diversify risk, particularly regulation of insurers' use of derivative instruments to hedge financial and underwriting risk, including disaster risk. Because of the complexity and relative newness of these instruments, regulatory policy in this area is still evolving. The NAIC's Investments of Insurers Model Act allows insurers to use derivatives to engage in hedging transactions and certain income-generation transactions. The total value of these transactions is limited to certain percentages of an insurer's total admitted assets. Thus, in theory, the model law should allow insurers to purchase securities that would compensate them for a portion of their losses caused by a natural disaster. The model law does not appear to allow insurers to purchase catastrophe derivatives for income-generation purchases, however.

This prohibition could impede the diversification of disaster risk within the industry. Some insurers might be well positioned to assume more disaster risk because they do not already have high catastrophe exposures. They may find that assuming catastrophe risk through investing in catastrophe-related securities would be less costly than entering a new disaster insurance market as a primary writer or as a reinsurer. Insurers may be more inclined to buy catastrophe-related securities than other investors because of the insurers' greater understanding of the underlying risk.

However, regulators may find it difficult to ascertain whether an insurer's purchase of disaster-related derivatives exposes it to excessive risk. Regulators can choose to: (1) allow insurers considerable discretion in making such investments; (2) expend considerable resources in analyzing and approving specific investments; or (3) establish arbitrary rules that severely limit or prohibit such investments. Some regulators might elect the third option as the easiest and safest route, but this would be contrary to the interests of disaster-prone states. Arbitrary restrictions on insurers' purchase of disaster-related securities could have a negative effect on the ability of financial markets to help diversify disaster risk and expand the supply of insurance.

The issue of risk limitation received increased attention at the NAIC after recent natural disasters. Regulatory action to force an insurer to reduce its catastrophe exposure could have a negative effect on the availability of insurance in disaster-prone states. Such regulatory actions would compel insurers to terminate policies and decline applications in

high-risk areas, which would reduce the supply and availability of insurance in these areas. Rating agencies, such as A. M. Best and Standard & Poor's, also have begun to consider an insurer's catastrophe risk in their rating evaluation, which increases insurers' incentives to diminish this exposure.

The valuation of reserves is another area that could affect disaster insurance markets. Currently, generally accepted accounting principles do not allow insurers to establish catastrophe reserves. There is no provision or requirement for catastrophe reserves under statutory accounting rules, nor do insurers receive favorable tax treatment of catastrophe reserves under current law. Reserves for future catastrophes represent a new concept in that they would not be tied to an event that has occurred, but rather would be based on an event that might occur in the future (Davidson, 1996; Russell and Jaffee, 1995). Insurers would be encouraged to accumulate funds to pay future catastrophe losses if these reserves were either not taxed or benefited from tax deferral. Insurers and regulators are currently working on proposed regulations governing catastrophe reserves which would be implemented if the federal government gives catastrophe reserves favorable tax treatment.

The complexity of catastrophe risk assessment, and the uncertainty surrounding estimates of the risk, also would affect estimating proper reserves for future catastrophe losses; insurers and regulators could easily make different subjective judgments about what is appropriate. If regulators require an insurer to increase its reserves for reported or anticipated claims due to natural disasters, this could force the insurer to reduce its exposure or increase rates. Since reserves are reported as a liability, insurers must set aside additional assets equal to the increase in reserves to maintain a given level of surplus. Further, because of the uncertainty surrounding reserve estimates, insurers must set aside additional capital to provide for losses that might exceed reserves.3 Insurers could raise additional capital to support these reserves, but this would come at a cost that would need to be reflected in insurance premiums. Otherwise, insurers will be forced to reduce their exposure to losses to bring it into line with regulatory requirements. This would necessitate

policy terminations and declinations, which in turn would reduce the supply and availability of insurance.

Finally, regulatory requirements governing insurers' ability to claim credit for reinsurance could limit the supply of disaster insurance. Regulators require reinsurers to meet certain criteria to be considered ''authorized" and allow a ceding insurer to account for anticipated recoveries from these reinsurers as assets. Primary insurers may still have some incentive to transfer disaster risk to unauthorized reinsurers (i.e., reinsurers who do not meet regulatory requirements to be authorized), but the inability to claim surplus credit for this reinsurance is a substantial disincentive for such transactions. Hence, regulation of reinsurance credit could have a substantial effect on primary insurers' capacity and ability to insure disaster-prone areas. This could hinder the emergence of new reinsurance capacity to help alleviate disaster insurance availability problems if regulators are reluctant to authorize new reinsurers.

The process by which regulators authorize reinsurers and allow reinsurance credit could be evaluated to see if there would be ways to boost capacity and still satisfy regulatory objectives. The access of U.S. regulators to alien reinsurers' financial data and regulatory actions has been one of the issues of contention. Agreements between U.S. regulators and foreign jurisdictions on information disclosure and the disposition of assets in the event of financial difficulty could help more alien reinsurers to become authorized.

Guaranty Funds

The use of guaranty funds and regulatory actions against failing insurers are important components of solvency regulation. Guaranty funds can accommodate short-term capacity problems by boosting assessment limits and borrowing funds, but high insolvency costs from a large natural disaster could severely tax the capacity of a guaranty fund and the market supporting it. As pointed out in Chapter 5, the nine insolvencies caused by Hurricane Andrew exceeded the Florida guaranty fund's assessment limits and forced it to borrow funds against future assessments to pay claims. The current system of uniform, pro rata guaranty fund assessments is not sensitive to risk and, hence, encourages greater risk-taking by insurers and policyholders.

Risk-sensitive assessments would encourage safer behavior, but they also could further tighten the supply of disaster insurance. Still, this could be preferable to arbitrary limits on risk. There also may be some value in

exploring arrangements that would allow state guaranty funds to pool capacity in certain instances (e.g., natural disasters) to provide additional liquidity and further diversify insolvency risk. Such arrangements would need to be structured to avoid perverse incentives and externalities among states in their regulatory policies towards high-risk insurers and markets (Klein, 1996). Without such provisions, a state could be encouraged to expose insurers operating within its jurisdiction to an excessive level of insolvency risk, since the costs of insolvencies would be spread among all states.

Policy Forms and Coverage Requirements

In regulating insurers' policy provisions covering disaster risk, insurance commissioners must balance the objectives of available coverage and affordable rates. Historically, regulators have tended to frown on policy provisions that would significantly restrict coverage, because of their concern that insureds will retain an excessive exposure to risk, knowingly or unknowingly. There may be some value in reconsidering this view for catastrophe insurance and allowing insurers to modify coverage provisions (e.g., increasing deductibles, altering limits, establishing coinsurance provisions, etc.) to encourage loss prevention and make it more economically feasible to offer catastrophe coverage. For example, the Insurance Services Office (ISO) has developed new homeowners' insurance policy forms that raise deductibles for damages caused by windstorms. Allowing such policies could serve the public interest if it enabled policyholders to bear more of the cost of small losses themselves, but to retain protection against catastrophic losses that would exhaust their assets. This would help to lower insurers' total losses from a disaster but would still provide insurance protection for severe damage to individual properties. Examining distributions of claim severity related to disasters could help insurers and regulators assess the potential gains from such an approach.

The question of whether homeowners should be mandated to carry certain coverages is difficult to answer. Mandatory coverage requirements can facilitate geographic risk diversification within a state and possibly counter adverse selection. Such requirements can force homeowners in low-risk areas to contribute actuarially fair premiums to a pool of funds available to pay losses in any part of the state. Adverse selection is countered by forcing low-risk homeowners to purchase coverage when they might otherwise choose not to buy insurance. However,

the fairness and effectiveness of such requirements are questionable, particularly if regulators also attempt to enforce cross-subsidies through price regulation or other measures. A preferable alternative may be to emphasize consumer education about disaster risk and to avoid policies that encourage risk-taking and discourage the purchase of insurance.

Rates

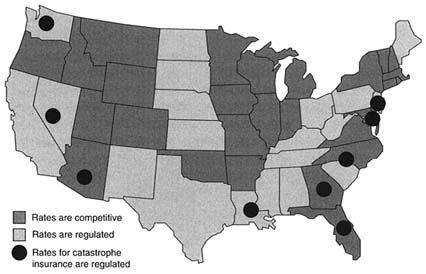

Regulation of disaster insurance rates is one of the most controversial issues facing policymakers. If an insurance market is structurally competitive, rate regulation should be unnecessary, unless the objective is to enforce cross-subsidies. Enforcing cross-subsidies through price regulation is difficult to accomplish if the offer and purchase of insurance are voluntary. Insurers will be reluctant to offer coverage at prices below cost, and consumers will be less inclined to buy coverage for which the price exceeds the actuarial cost. Some insurers would be encouraged to only market insurance in low-risk areas where they could undercut the prices charged by insurers forced to subsidize their insureds in high-risk areas. (This occurred in Michigan when the legislature attempted to restrict rate differentials between urban and nonurban areas for auto and homeowners' insurance.) Regulatory efforts to suppress rates below costs will cause economic distortions and potentially threaten insurers' solvency if exit is restricted. Figure 8-2 depicts states that have prior-approval regulations for homeowners' insurance rates as well as those states that have instituted regulations restricting rates for coverage against catastrophic losses.

However, allowing insurers to significantly raise prices following a natural disaster raises some economic questions as well as political problems. Recent disasters appear to have awakened insurers to their greater catastrophe risk and the inadequate catastrophe loads in their rates. New databases and more sophisticated modeling techniques have been developed to meet insurers' information needs and support more accurate pricing. However, this science is still evolving, and regulators as well as insurers are having some difficulty assessing the validity of the new catastrophe rate analyses and the assumptions that drive their results. For proprietary reasons, modelers are reluctant to disclose their assumptions in public rate proceedings. The complexity of this analysis, the secrecy surrounding it, and the significance of the results compound the political problems. Hence, insurers have been frustrated in their attempts to obtain

FIGURE 8-2 Insurance price regulation, by state.

regulatory approval for large rate increases for increased catastrophe risk based on catastrophe models.

The challenge of prospective pricing of catastrophe risk may require new regulatory approaches. As discussed in Chapter 5, the Florida Commission on Hurricane Loss Projection Methodology is an example of a public-private effort to improve the science underlying catastrophe risk assessment and insurance pricing, and reach consensus regarding them. This approach does not guarantee regulatory acceptance of a catastrophe model; for example, Florida Insurance Commissioner Bill Nelson has challenged a model approved by the commission. The NAIC is developing a manual to help regulators understand and assess catastrophe models. Given the high degree of uncertainty associated with catastrophe loss projections, it is critical to find ways to increase public confidence in the use of the best scientific methods to support adequate insurance prices. There is also the question of whether prior regulatory approval of complex catastrophe rate filings is feasible and necessary. Would it be more practical for regulators to implement some form of competitive rating approach (e.g., file and use), where they would monitor market pricing and performance and intervene only if competition failed or other serious market problems developed?

Discounting premiums for policyholders who take effective mitigation measures is another important issue. Insurers allege that inadequate regulatory ceilings on prices discourage them from implementing pricing discounts for loss prevention efforts by insureds. Their logic may be that any economic gains that would accrue to an insurer from offering such discounts would be offset by greater losses from writing more business at inadequate rates. Research aimed at better catastrophe risk assessment as well as the effects of mitigation on reducing losses could help to solve both problems. If insurance companies and regulators can agree on adequate overall rate levels, insurers should offer price discounts that, at the margin, are equal to their expected cost savings from mitigation. This would increase homeowners' incentives to invest in mitigation and lower overall losses to the extent that it is cost-effective to do so through mitigation. Ideally, a homeowner should receive sufficient information to capitalize investments in mitigation over the expected life of their home. Capitalized mitigation investments could be recaptured in the price of a home if the owner sold it. The present value of even a small annual premium reduction could be significant if accumulated over the life of a home.

Even with discounts for mitigation and greater public confidence in catastrophe risk modeling, implementing actuarially fair disaster insurance prices could have significant economic implications for some high-risk areas and could encounter significant political opposition. Large rate increases could strain some homeowners' budgets and reduce property values in high-risk areas. While these kinds of economic adjustments are inevitable unless subsidies are provided, policymakers may wish to consider phase-in or transition strategies that will help to ease the adjustment process and diminish political opposition.

Regulators and legislators face strong political pressures to subsidize insurance rates in high-risk areas. Political support for subsidies, which may be concentrated among residents in high-risk areas, conflict with countervailing political pressure against subsidies in low-risk areas. Equity issues and political considerations aside, however, it is very difficult for regulators to enforce cross-subsidies within a state as well as across states when insurance is sold by private firms (as opposed to a government-imposed monopoly insurer). Even with coverage mandates, individual private insurers can find a number of ways to avoid writing risks at rates below cost (e.g., not marketing to high-risk areas). Efforts to enforce cross-subsidies also encourage greater risk-taking and economic losses. If rates are suppressed below expected costs from catastrophes,

insureds will have diminished incentives to mitigate their risk in order to lower their premiums.

Underwriting Selection

States generally impose only limited underwriting restrictions on insurers, such as requirement of advance notice for policy terminations. However, as indicated in Figure 8-3, a number of states have imposed special underwriting restrictions related to catastrophe risk, according to an NAIC survey. These restrictions have taken the form of limitations or moratoriums on insurers' ability to terminate or otherwise not renew policies because of geographic location or exposure to catastrophe risk.

In addition, in areas subject to severe availability problems, legislators may be tempted to enact laws that restrict insurers' ability to refuse to accept new risks. The Florida legislature, for example, in 1996 considered but did not enact legislation that would force an insurer to maintain a market share in coastal areas at least as high as its market share in other parts of the state. Such restrictions are difficult to enforce and

FIGURE 8-3 Catastrophe underwriting restrictions, by state.

counterproductive in the long run. Many of the variables that affect an insurer's volume of business, such as competition, are not under the direct control of the insurer or of regulators. Also, this type of regulation would discourage the entry of new insurers.

As an alternative, insurers could be required to inform rejected insurance applicants as to the reason for their failure to obtain a policy and give the applicant the opportunity to cure the problem that caused the rejection. This might introduce a greater degree of discipline and accountability in the underwriting process without tying insurers' hands, although it would increase paperwork burdens for insurers. This policy could also encourage homeowners to undertake certain mitigation efforts to make their properties more insurable. On the other hand, such a policy would not solve the problem for homes rejected because of their locations or other conditions for which there is no effective remedy.

Claims Adjustment

Regulation of insurers' claims adjustment practices following a disaster can have a significant effect on the cost and supply of insurance. Clearly, regulators must ensure that insurers meet the terms of their contracts. This becomes difficult, however, when these terms are unclear or claimants seek to retroactively expand coverage beyond that stated in their contract or paid for through premiums. For example, there is the issue of whether insurers should pay the cost of rebuilding a structure to meet more stringent building code standards than those in effect when the structure was originally built. Some regulators believe that code enhancement should be covered under standard insurance contracts, but many insurers disagree. Although a retroactive effort to expand coverage may be intended to help claimants, it can subject insurers to unanticipated losses and encourage fraud and excessive risk-taking. In addressing claim disputes, regulators need to be careful to maintain the integrity of policy provisions; failing to do so could further discourage entry, lessen availability, and increase rates.

Regulators have a substantial role to play in facilitating the claims adjustment process following a natural disaster. Regulators in California, Florida, South Carolina, and Texas, among other states, have developed comprehensive disaster response programs that are key to recovery efforts. The NAIC has revised and expanded its disaster response manual based on the experiences of these states. This manual outlines a number of steps that regulators can take to expedite payment of claims from a

natural disaster, including providing an information clearinghouse for consumers and insurers, and helping to support adjusters rushed in to deal with the flood of claims. Some states have even taken steps such as controlling the prices of building materials following a disaster.

Other Market Practices

Other market practices that may affect the availability and cost of disaster insurance include sales and marketing activities, appointment and termination of agents, and so on. It is not clear that the regulation of these practices can significantly improve market conditions for disaster insurance. For example, it is very difficult to force insurers to sell coverage to populations in high-risk areas. It also is hard to measure the intensity of insurers' efforts to market to particular areas, and their success will be affected by a number of factors outside their control.

Residual market mechanisms and other state-sponsored disaster risk financing mechanisms (discussed in Chapters 2, 4 and 5) raise some interesting policy questions. Regulators generally believe that these mechanisms can be effective in providing an intermediate layer of excess reinsurance coverage. Residual market mechanisms could promote greater economic efficiency if they facilitate more effective risk pooling within a state, or if they can utilize state government guarantees and recoupment mechanisms to facilitate long-term risk financing, which in turn facilitates the diversification of risk over time.

State residual market mechanisms have been affected by the decreased supply of residential property coverage because of catastrophe risk. Most states have seen small or moderate increases in their residential property RMMs because of catastrophe risk and insurance availability problems, as reflected in Figure 8-4. However, Florida and Hawaii have very large residual markets (representing approximately 30 percent of the market) because of their high catastrophe risk exposure. RMMs of this size are difficult to sustain for a long period, and there are vigorous efforts to depopulate them.

Public insurers may be able to secure favorable tax treatment for catastrophe reserves that may be denied to private insurers because of concerns that private insurers would manipulate reserves to lower their taxes. If state risk pools supplement (rather than supplant) private reinsurance market capacity, they could increase the supply of voluntary market coverage. Such mechanisms cannot be used to enforce cross-subsidies within a state unless they are established as a monopoly, and all

property owners are forced to buy insurance. If coverage were voluntary, private insurers would avoid selling, and property owners would be disinclined to buy insurance that was overpriced in order to support subsidies for high-risk areas.

State catastrophe pools have limited capacity to solve disaster insurance availability problems in high-risk states. A state mechanism can only pool exposures within a state; this insufficiently diversifies the risk of very large catastrophes that could occur within a state. States can accumulate tax-favored reserves over time, as well as borrow money if necessary, but the size of their markets still limits the amount of funds they can accumulate or borrow. As noted above, rough estimates of the total catastrophe capacity (including state pools) for Florida or California are $10–$12 billion, which falls considerably short of the potential $50–$75 billion in insured losses that could occur from a catastrophe in a major population center of either state.

FIGURE 8-4 Residual market share, by state. Shows percentage of insurance market in each state that is covered by residual market mechanisms.

COORDINATING GOVERNMENT POLICIES TOWARD DISASTER RISK