Paying the Price: The Status and Role of Insurance Against Natural Disasters in the United States (1998)

Chapter: 6 The National Flood Insurance Program

CHAPTER SIX

The National Flood Insurance Program

EDWARD T. PASTERICK

FLOODS, LIKE OTHER NATURAL disasters, present us with two challenges: how to contain the cost of the damage they cause, and how to provide economically feasible relief to victims that will help them recover from the disaster. Containing the cost of damage caused by flooding has generally been accomplished either through constructing flood control works designed to keep floodwaters away from properties located in the floodplain, or through land use regulation employed to guide construction away from the path of floods or ensure safer building in the floodplain.

The federal government's first response in this arena was the Flood Control Act of 1936 (49 Stat., 1570), which launched a national program of structural flood control works. Structural flood control measures have had their critics almost from the start. They argue that, while structural projects have afforded a degree of protection from floods, they also give the residents of floodplains a false sense of security, which has resulted in even further encroachment on the floodplain, thus increasing rather than reducing the cost of potential losses (White, 1953).

For assisting flood victims in the post-disaster recovery process, the only available recourse until 1968 was federal disaster assistance, which took the form of disaster loans and grants. However, the continuing increase in the costs to the federal treasury of providing this relief has caused policymakers to look closely at the feasibility of providing insurance coverage against flood losses as a preferable alternative to federal assistance.

When insurance against flood losses was first discussed in the 1950s, it became clear that private insurance companies could not profitably provide such coverage at an affordable price. This was primarily because of the catastrophic nature of flooding and the insurers' inability to develop an actuarial rate structure that could adequately reflect the risk to which flood-prone properties were exposed. The conclusion was that such an insurance program would require a substantial involvement by the federal government.

With passage of the Federal Flood Insurance Act of 1956, Congress proposed an experimental program designed to demonstrate that private sector provision of flood insurance was commercially feasible (42 U.S. Code, sec. 2401 et seq.). This experimental program was never implemented, largely due to a lack of support from the insurance industry and the above-mentioned difficulty in establishing a sound actuarial foundation for the program. (It should be noted that private insurers do write limited amounts of flood coverage, usually for commercial insureds, under Inland Marine and ''Difference of Conditions" policies. The existence of the National Flood Insurance Program has now created an environment favorable to the provision of some private residential flood coverage.)

The next serious look into the feasibility of creating a program of insurance against flood loss took place in the aftermath of Hurricane Betsy, which struck the Gulf Coast in the summer of 1965, and the heavy flooding on the upper Mississippi River in that same year. The Southeast Hurricane Disaster Relief Act of 1965 (P.L. 89-339), which provided federal financial relief to the victims of Hurricane Betsy, authorized a study to explore alternative ways of providing aid to flood victims.

This study resulted in a 1966 report from the Secretary of Housing and Urban Development (HUD) entitled "Insurance and Other Programs for Financial Assistance to Flood Victims" (U.S. Department of Housing and Urban Development). This report proposed that a flood insurance program to replace reliance on public assistance to repair flood-damaged property would be feasible if it contained the following essential elements:

accurate estimates of risk

compensation to the risk bearer

the possibility of some level of premium subsidy, if publicly desirable

incentives to policyholders to reduce risks

incentives to states and local governments for wise management of flood-prone areas

continuous reappraisal.

It was on the basis of this report that Congress passed the National Flood Insurance Act of 1968 (see Figure 6-1), which created the National Flood Insurance Program (NFIP). Later legislative revisions have generally been based on one or more of the key elements just listed. These revisions—the Flood Disaster Protection Act of 1973 and the National Flood Insurance Reform Act of 1994—both addressed perceived program inadequacies arising from experience with the program up to that point in time. The measures adopted had generally been anticipated and discussed in the 1966 HUD report (see Figure 6-1 on NFIP legislation).

NATIONAL FLOOD INSURANCE ACT OF 1968

(P.L. 90-448, Title XIII, 42 U.S. Code, sec. 4001 et seq.)

Created the National Flood Insurance Program

Made flood insurance available in communities that agree to adopt and enforce floodplain management ordinances

FLOOD DISASTER PROTECTION ACT OF 1973

(P.L. 93-234, 42 U.S. Code, sec. 4001 et seq.)

Made community participation in the NFIP a condition of eligibility for certain types of federal assistance

Made the purchase of flood insurance a condition for federal and federally related mortgage loans in high-risk flood area.

NATIONAL FLOOD INSURANCE REFORM ACT OF 1994

(P.L. 103-325, 108 Stat., 2255)

Strengthened the mandatory purchase requirements of the 1973 act

Created the Flood Mitigation Assistance Grant Program

Revised the Standard Flood Insurance Policy to include Increased Cost of Compliance coverage

Included the Community Rating System in the statute.

FIGURE 6-1 NFIP legislation.

The NFIP was originally placed under the authority of the Secretary of HUD, who delegated program authority to the administrator of the Federal Insurance Administration (FIA). In 1979, FIA and its programs were transferred to the newly created Federal Emergency Management Agency (FEMA).

STRUCTURE OF THE NATIONAL FLOOD INSURANCE PROGRAM

The NFIP structure includes three essential components: risk identification, hazard mitigation (i.e., actions taken to protect people and property from the flood peril), and insurance. Effective integration of these three components requires cooperation between the federal government, state and local governments, and the private property insurance industry. The authorizing legislation defined a role for each of these, which in some cases has been altered over the program's history.

Risk Identification

One of the major obstacles preventing the private insurance industry from providing flood insurance was its inability to adequately identify all the areas throughout the country that were vulnerable to flood hazards and then to effectively define the nature and extent of the risk. Because of the costs associated with conducting the hydrological studies needed to secure this information and the nationwide scope of the effort, the legislation assigned this task of risk identification to the federal government. Under the program as originally designed, community eligibility was conditioned on the completion of a flood insurance rate study and on a community's adoption of the resultant Flood Insurance Rate Map (FIRM). The FIRM serves both as the guide to the community for purposes of floodplain regulation and overall land use decision making, and as the source of risk information for property insurance agents to accurately rate policies.

The length of time required to produce a FIRM, and the resultant delay in insurance availability, prompted Congress to authorize the Emergency Program in 1969. This measure enabled property owners in a participating community to purchase limited amounts of flood insurance at estimated rates until completion of the FIRM, at which point the community was converted to full coverage under the Regular Program, which uses actuarial rates. Until 1974, both community participation and individual purchase of insurance was completely voluntary, and the studies

conducted and maps produced were only for those communities that had applied for participation in the program.

When Tropical Storm Agnes struck the Eastern seaboard in 1972, it became clear that many communities were either unaware of the serious flood risk to which they were exposed or had been unwilling to take the necessary measures to protect residents of the floodplain. Very few of the communities affected by the storm had applied for participation in the NFIP, and even in these participating communities owners of most flood-prone property opted not to purchase flood insurance. This lack of response to the NFIP perpetuated the reliance of flood victims on federal disaster assistance to finance their recovery.

Because of this minimal participation, the 1973 Flood Disaster Protection Act made the NFIP responsible for identifying all communities nationwide that contained areas at risk for serious flood hazard. The NFIP was also required to notify these communities of their choice of applying for participation in the NFIP or forgoing the availability of certain types of federal assistance in their community's floodplains. This NFIP effort identified over 21,000 flood-prone communities in the 50 states and the District of Columbia. It also identified one community each in American Samoa, Guam, Puerto Rico, Territory of the Pacific, and the Virgin Islands. As of March 1998, 18,760 communities, including one each in the territories, had joined the NFIP. Most flood-prone communities that have elected not to participate are communities whose areas of serious flood risk are either very small or have few if any structures. The dramatic increase in community participation stemming from this nationwide notification has had the further result of increasing the number of detailed flood studies that the government has been required to complete. Although the hazard identification process identified all communities having any areas subject to serious flood risk, regardless of the size of such areas, not all communities have required a detailed study in order to participate in the NFIP.

The NFIP conducts two general types of flood studies, approximate and detailed. Detailed studies are conducted for communities with developing areas—that is, areas where industrial, commercial, or residential growth is beginning and/or where subdivision is under way, and where the development or subdivision is likely to continue. Communities with minimal flood risk have been brought into the program without such a detailed study being conducted. Approximately 6,300 of the 18,760 participating communities are in this low-risk category. Through fiscal year 1997, the cost of this massive study effort has been about $1.154 billion.

For purposes of risk identification, the NFIP uses as the standard of risk the "100-year flood," also referred to as the one percent flood or the base flood. This is a degree of flooding that has a one percent chance of occurring in a given year. On most community FIRMs the 100-year flood is indicated in terms of flood elevations in feet relative to mean sea level. In coastal areas, which are exposed to the additional hazard of wave action, the base flood includes the height of the waves above the stillwater elevation. The term "100-year flood" is problematic for the NFIP. It is a term of convenience intended to convey probability but has had the adverse effect of giving floodplain residents, who tend to interpret it in chronological terms, a false sense of security.

Hazard Mitigation

No program of insurance against flood damage is considered feasible without the assurance that over time the risk exposure that the program takes on will be reduced through responsible mitigation actions. The standards established by the NFIP are based on a nonstructural approach to floodplain regulation and are designed to supplement the federal government's program of structural flood works. While demand continues for the construction of floodworks to provide protection to floodplain residents, many are still skeptical about the efficacy of such structures. Although the NFIP has adopted a nonstructural approach to floodplain management, the NFIP rate structure gives credit to structural flood works if they are certified to protect against the base flood.

The responsibility for hazard mitigation under the NFIP is split between the federal government and the local participating community. The NFIP enters into an arrangement with the local community whereby structures built in the floodplain without full knowledge of their degree of flood risk can be insured at less than full actuarial rates. In exchange, the local community makes a commitment to regulate the location and design of future floodplain construction in a way that results in increased safety from flood hazards. The federal government has established a series of building and development standards for floodplain construction to serve as minimum requirements for participation in the program. These standards use the 100-year flood as the basis for regulation. The primary mitigation action required by the regulations is elevation of the lowest floor of a structure above the level of the base flood as determined by the Flood Insurance Rate Study and shown on the FIRM. The rates for coverage of structures built or substantially improved after the date of the FIRM are based on this elevation.

The local community is responsible for adopting and enforcing these floodplain management standards, and compliance is accomplished through the building permit process. Since local governments have jurisdiction over land use and development, it is only at the local community level that the implementation of standards will be effective. FEMA, working with the state government, conducts periodic reviews at the local level to assess the local community's enforcement of NFIP standards. A determination that a community is not adequately enforcing local ordinances can result in a period of probation, during which a surcharge is added to insurance premiums on all NFIP policies in the community. If the community fails to take corrective actions during this probation period, it can be suspended from the program, which means that NFIP coverage becomes unavailable.

Periodically, there have been proposals that the federal government be authorized to override local regulation when the local government has refused to participate in the NFIP, thereby denying insurance protection to its citizens, or when a local government does not adequately enforce its floodplain regulations. The NFIP, however, has consistently taken the position that federal land use regulation at the local level is illegal, and, in any case, would be unworkable.

While the NFIP compliance process has identified a number of violations of program standards at the local level, there has never been a comprehensive assessment of the level of compliance nationwide or of the overall effect of program standards on local development patterns. Nevertheless, certain limited assessments have been done and a certain amount of data relevant to the issue has been collected. The Natural Hazards Research and Applications Information Center (NHRAIC) prepared a report in 1992 for the Federal Interagency Floodplain Management Task Force noting a number of significant achievements in floodplain management, including more widespread public recognition of flood hazards, as well as reduced development and losses in many localities. Much of these accomplishments can be attributed to the NFIP. But the report also found that "a considerable distance remains between the status quo and the ideal that can be envisioned" (NHRAIC, 1992). The report acknowledges the difficulty in assessing the effectiveness of floodplain management, stating "that there are few clearly stated, measurable goals, and that there is not enough consistent reliable data about program activities and their impacts to tell how much progress is being made in a given direction" (NHRAIC, 1992).

In 1994, the Interagency Floodplain Management Review Committee

(IFMRC) studied the causes and consequences of the 1993 Midwest flooding. The committee's report, while recognizing that NFIP requirements are minimum standards that are applied to areas subject to very different flooding conditions, noted that "in the Midwest, the NFIP tends to discourage floodplain development through the increased costs in meeting floodplain management requirements and the cost of an annual flood insurance premium, although this may not be the case elsewhere in the nation. Individuals and developers appear to choose locations out of the floodplain to avoid these costs. Developers have the added incentive of wanting to avoid marketing flood-prone property. Many communities visited by the Review Committee actively discourage floodplain development" (IFMRC, 1994, p. 97).

An analysis of loss experience from 1978 to 1994 also provides some indications of the effectiveness of the program's standards. The figures show that, in general, structures built before 1975, which were subject to no NFIP standards, suffered about six times more damage from flooding than those built after NFIP mitigation requirements became effective.

Figure 6-2 shows the distribution of NFIP flood claims made from the beginning of the program through December 31, 1997.

Insurance—Rates

Since the NFIP began, its insurance structure has included two general classes of properties: those insured at full actuarial rates and those that, because of their date of construction, are statutorily eligible to be insured at lower, "subsidized" rates—that is, rates that do not reflect the full risk to which a property is exposed. Actuarial rates for coverage are charged to property owners living outside 100-year flood hazard areas and to those living within 100-year areas who built or substantially improved structures after the federal government provided complete risk information from the Flood Insurance Rate Map.

The date of this map differentiates the two classes of properties. Properties built prior to the availability of this information (known as pre-FIRM structures) are insured at "subsidized" rates which, while they represent some contribution on the part of the property owner to his or her financial protection, do not reflect the full risk to which the property is exposed. The 1966 HUD study considered such a "subsidy" to be important in providing an incentive to local communities to participate in the NFIP and regulate future floodplain construction.

The concept of "subsidy" as applied to the NFIP is often misunderstood.

The subsidy does not refer to a direct infusion of taxpayer dollars to offset the shortfall in premium from properties paying this lower rate. Rather, it prevents the program from building a catastrophe reserve that can be used to pay claims in heavier loss years; the NFIP has been required to exercise its borrowing authority from the U.S. Treasury to pay such claims.

While the law calls for a lower-than-actuarial rate to be charged to pre-FIRM structures in the floodplain, it does not specify the actual rate. During the 1970s, when the primary program objective was to enlist communities to participate in the NFIP, these rates were substantially lower than the actuarial rates. In 1981, the program began a process of gradually increasing the rates charged for existing construction in order to reduce the amount of subsidy and attempt to render the program self-supporting for the average historical loss year. In 1981, rates for pre-FIRM structures were increased 19 percent, and in 1983 they were increased another 45 percent. From 1983 through 1995, eight increases in rates for both structures with subsidized and actuarially based rates averaged about 8 percent each. As the subsidized rates for existing structures have been raised, the number of properties requiring a subsidy has also continued to decline over the years, going from about 75 percent in 1978 to about 35 percent in 1997. The premiums paid by this group of insureds are estimated to be about 38 percent of the full-risk premium needed to fund the long-term expectation for losses.

Insurance—Private Industry Participation

Under the NFIP's original 1968 design, the private insurance sector marketed flood insurance to floodplain occupants through a consortium of 125 insurance companies called the National Flood Insurers Association (NFIA). The NFIA not only sold and serviced flood insurance policies through licensed property insurance agents, it also underwrote the coverage, with the federal government providing premium equalization payments to offset underwriting losses due to the inability to charge full actuarial rates on existing properties in high-hazard areas. This was the program structure recommended in the 1966 study. In 1977, the government, because of problems of financial control and a dispute over program authority, exercised its option under the act to make the program an all-federal program, using private insurance agents and adjusters to sell and service the policies directly through the NFIP. This form of insurance operation prevailed until 1983.

Write-Your-Own Program

In 1983, private insurance companies again became involved in the NFIP through the Write-Your-Own (WYO) Program, an arrangement by which the private insurers sell and service federally underwritten flood insurance policies under their own names, retaining a percentage of premium (currently 31.9 percent) for administrative and production costs. The WYO arrangement, signed every year by participating companies, specifies the responsibilities of both the insurers and the federal government. WYO companies are required to comply with standards outlined in the WYO Financial Control Plan, which covers all aspects of their operations, including underwriting, claims, cash management, and financial reporting. Company representation in the administration and oversight of the program is accomplished through the Institute for Business and Home Safety's Flood Committee, and through company representation on the WYO Standards Committee. In addition, the Flood Insurance Producers National Committee serves as an advisory group to represent the interests of property insurance agents who sell and service NFIP policies.

One hundred sixty-seven companies now participate in the WYO program. Over the 15-year period since WYO's inception, a growing percentage of total program policies have been written by WYO companies. At present, WYO companies write about 92 percent of NFIP policies, the remainder still being written by agents who deal directly with the federal government.

COMMUNITY RATING SYSTEM

The Community Rating System (CRS) was created by the FIA in 1990 as a mechanism for recognizing and encouraging community floodplain management activities that exceed the minimum NFIP standards. The three goals of the CRS are to reduce flood losses, to facilitate accurate insurance rating, and to promote the awareness of flood insurance. When a community's activities meet these three goals, its flood insurance premiums are adjusted to reflect the resulting reduction in flood risk.

In order to recognize community floodplain management activities in this insurance rating system, they must be described, measured, and evaluated. A community receives a CRS classification based upon the scores for its activities. There are ten CRS classes: Class 1 requires the most credit points and results in the greatest premium reduction; Class

10 receives no premium deduction. A community that does not apply for the CRS or does not obtain a minimum number of credit points is a Class 10 community.

Community application for the CRS is voluntary. Any community that is in full compliance with the rules and regulations of the NFIP may apply for a CRS classification better than Class 10. A community applies for a CRS classification by sending completed application worksheets with appropriate documentation that it is doing activities recognized by the CRS. This documentation is sent to the community's regional FEMA office.

A community's CRS classification is assigned on the basis of a field verification of the activities included in its application. These verifications are conducted by the Insurance Services Office, Inc. (ISO), an organization providing standardized forms, and rating and actuarial services to firms in the insurance industry. The ISO has been conducting community grading for fire insurance for many years and is now rating communities under the newly implemented Building Code Effectiveness Grading Schedule discussed below. This organization's available resources enable it to carry out the fieldwork involved with the CRS.

There are currently 912 communities participating in the CRS.

SIDEBAR 6-1Creditable Activities for the CRS Credit points are based on how well an activity meets the three goals of the CRS mentioned in the text, and are calculated for each activity using formulas and adjustment factors. The CRS recognizes 18 creditable activities organized in four categories:

|

Tulsa, Oklahoma, and Sanibel Island, Florida, are, at Class 5, the two best-rated CRS communities (25 percent premium discount). Part of the underlying strategy of the CRS is to have communities join and to improve their classifications. In fact, over 32 percent of all CRS communities are a Class 8 or better.

While these 912 CRS communities are only 5 percent of the total NFIP participating communities, they represent over 63 percent of all policyholders. It is important to note that these 912 communities must undertake and demonstrate flood loss mitigation activities above and beyond the significant level of activities already required for minimum community NFIP participation. Even communities that are in Class 10 and in good standing with the NFIP carry out significant flood loss reduction activities. Sidebar 6-1 describes the type of activities that earn CRS credits.

Relationship to Other Insurance Grading Systems

The CRS for flood insurance was inspired by the Public Protection Grading System (PPGS) used by the insurance industry to adjust fire insurance premiums according to a community's firefighting and prevention

Some of these activities may be implemented by the state or by a regional agency rather than at the community level. For example, some states have disclosure laws that are creditable in the flood hazard disclosure category. Any community in those states will receive those credit points if it demonstrates that it effectively implements the law. The CRS recognizes some established methods for obtaining credits in each activity, although communities are invited to propose alternative approaches to these activities in their applications. |

capability. The grading system approach has been employed and refined for fire insurance since 1912. The expertise and advice of the Insurance Services Office, the industry entity responsible for administering the PPGS, played a valuable part in the development and implementation of the CRS. But whereas the PPGS addresses the engineering aspects of a community's loss reduction capability, the CRS expands the community grading concept to include ordinances and codes that are being enforced by communities and that result in a reduction in flood losses. The insurance industry has developed, and is now in the early stages of implementing, a Building Code Effectiveness Grading Schedule (BCEGS). This system, developed in the wake of the devastating losses caused by Hurricane Andrew, grades communities on their adoption and enforcement of building codes that affect losses from natural hazards for which the private sector is providing insurance. It is safe to say that the successful implementation of the CRS encouraged this expanded community grading concept for use in adjusting private sector insurance rates. This cross-pollination of ideas has been an important and valuable benefit of the private and public sector involvement in the CRS, the NFIP, and other natural hazard mitigation efforts.

PROGRAM FUNDING

The NFIP is funded through the National Flood Insurance Fund, which was established in the U.S. Treasury by the National Flood Insurance Act of 1968. Collected premiums are deposited into the fund, and losses, operating costs, and administrative expenses are paid out of the fund. The National Flood Insurance Program also has the authority to borrow up to $1 billion from the Treasury. During the early years of the program, when the private insurance sector underwrote the coverage, the government called upon its borrowing authority regularly to make the premium equalization payments to the industry pool. This was necessary because no funds had been provided by the act to capitalize the program initially. The NFIP experienced annual operating losses during the period 1972–1980 ranging from $5,400,000 to $323,228,000. Cumulative operating losses from the beginning of the NFIP in 1969 to 1980 totaled about $817,680,000.

Congressional appropriation to repay borrowed funds was first requested in 1981 and the program received an appropriation to repay borrowed funds each year until 1986. The total amount borrowed from the Treasury prior to 1986 was $1.2 billion, all of which was repaid

through a series of appropriations. During this same period, from 1981 through 1986, only 1983 and 1984 experienced a negative operating result. Between 1987 and 1996, negative operating results were experienced in 1989, 1990, 1992, 1993, 1995, and 1996.

As noted previously, before 1981 no action was taken regarding the level of subsidy being accorded existing properties in high-risk areas, the program focus being primarily on promoting community participation. Consequently, program expenses inevitably exceeded income. In 1981, the administrator of the FIA established a goal of making the program self-supporting for the average historical loss year by 1988. Note that the goal was that the program be self-supporting, not that it be actuarially sound.

The continuing statutory requirement to ''subsidize" certain existing properties in high-hazard areas still makes actuarial soundness an unrealistic goal at this point in the program's history. "Self-supporting" means that in years where losses are less than the historical average, the program builds up a surplus to be used in years when losses exceed that average. However, even though the premiums for existing buildings have been regularly raised to the point where they are now higher, on average, than the premiums paid for new construction, they still represent only about 38 percent of the full-risk premium for these properties. These properties currently make up about 35 percent of the NFIP book of business. This shortfall in premiums prevents the program from accumulating the kind of catastrophe reserves that would reduce the need to borrow. The premium shortfall also makes it more difficult for the NFIP to repay funds when borrowing becomes necessary.

Nevertheless, even with the statutory subsidy, from 1986 until 1995 the program operated with a positive cash balance except for a brief period beginning in December 1993, when the NFIP borrowed $11 million from the Treasury to pay claims. The borrowed funds were repaid in six months. However, in the four fiscal years from 1993 through 1996, the program experienced over $3.4 billion in losses, and beginning in July 1995 the program has had to borrow substantial funds from the Treasury. The level of borrowing reached $917 million in June 1997, but by March 1998, the level had been reduced to $810 million through repayments, including $45 million in interest. The outstanding amount borrowed as of April 30, 1997, was $880 million. It is significant to note that from 1969 through 1997, almost $10 billion in premiums was collected from policyholders, and over $8 billion was expended by the program for loss payments and loss adjustment expense.

Until 1986, federal salaries and expenses, as well as the costs associated with flood mapping and floodplain management, were paid by an annual appropriation from Congress. From 1987 to 1990, however, Congress required the program to pay these expenses out of premium dollars without giving the program the opportunity to adjust the rate structure to reflect these costs. This resulted in a loss of about $350 million in loss reserves available to pay claims. Beginning in 1990, a federal policy fee of $25 (now $30) was levied on most policies in order to generate the funds for salaries, expenses, and mitigation costs.

ISSUES

The remainder of this chapter describes issues confronting the National Flood Insurance Program at this writing, their background and possible solutions.

Interrelationship of Insurance, Risk Assessment, and Mitigation

The key to any success that the NFIP has been able to achieve is the close integration of the three critical program components: risk identification, hazard mitigation, and insurance. The NFIP has been able to integrate these components to some extent, and has been held up as a model for addressing other hazards, such as earthquake, that present some of the same problems of insurability. However, within the current FEMA structure, the risk identification and mitigation responsibilities are organizationally separated from the insurance operation. The two offices have established procedures to assure ongoing coordination of policy decisions, but continued coordination will require a level of effort beyond that needed when the three components were in the same office.

Mandatory Purchase

The 1966 HUD report recognized the importance of the lending industry to the success of a flood insurance program: "The degree to which lenders of all kinds encouraged or required flood insurance as a condition of loans in high-hazard areas would have a great deal to do with its acceptance" (U.S. Department of Housing and Urban Development, 1966, p. 83). The report assumed that lenders would treat flood insurance like other forms of hazard insurance in their mortgage activity. The fact that lenders failed to do so became obvious when Tropical Storm

Agnes struck in June 1972. At the time, there were less than 200,000 flood insurance policies in force (PIF) nationwide, and very few in the areas affected by the storm (29 in Wilkes-Barre, Pennsylvania, one of the worst hit communities). This was one of the major factors that prompted Congress to enact the Flood Disaster Protection Act of 1973, which made participation in the NFIP a prerequisite for eligibility for certain kinds of federal assistance used in floodplains. It made the purchase of flood insurance a mandatory condition of any federally related mortgage on a property in an identified flood hazard area.

Even after the legislative requirement was in place, the spread of coverage to other properties in the nation's floodplains has not been proportionate to the level of mortgage activity in those areas. While the policy count grew significantly in the years immediately following the 1973 act, the annual growth rate since 1980 has averaged only about 3 percent. Florida has 1.5 million PIF, followed by Louisiana's 300,000, Texas's 250,000, California's 235,000, and New Jersey's 155,000. Data on the reasons for this slow growth have been hard to come by. Some evidence indicates that, while lenders have been requiring flood insurance at the point of loan origination, they have not been vigilant in ensuring that the mortgagor renews the policy in subsequent years.

In the light of this evidence, the National Flood Insurance Reform Act of 1994 focused on lender compliance as one of the major program areas requiring attention. The 1994 act expands the mandatory purchase provisions in a number of areas, as follows:

It requires that lenders who establish escrow accounts for hazard insurance and taxes include flood insurance premiums in such accounts. Allowing the homeowner to pay a portion of the premium each month as part of a mortgage payment eliminates the annual temptation to drop the coverage.

The act calls for lenders to require flood insurance to be purchased during the life of a loan, whenever it becomes known that the property is located in an identified special flood hazard area. The 1973 act required purchase of insurance only at loan inception.

In cases where borrowers who are required to purchase flood insurance fail to do so, the act gives lenders the authority to purchase the coverage on behalf of the borrower, that is, to forceplace it.

Unlike the 1973 act, the 1994 Reform Act provides for financial

penalties for noncompliance. The absence of real consequences for lenders not requiring flood insurance had created a situation where the importance of flood coverage as mortgage protection was recognized only at the time of an actual flood, too late to benefit victims.

Mitigation and Existing Structures

A major issue to be dealt with in the area of mitigation is the matter of existing structures. The NFIP floodplain management requirements are primarily directed toward guiding future construction in the floodplain. The 1966 HUD report projected that subsidies for existing high-risk properties would be needed for about 25 years. This was based on the assumption that a turnover in housing stock, particularly those structures most exposed to serious flood hazard, would, over that time, result in the large majority of structures being rebuilt in compliance with NFIP building standards and insured at full actuarial rates. However, modern construction and renovation techniques have greatly extended the useful life of buildings, with the result that the replacement of this older housing stock has not occurred as quickly as anticipated by the feasibility study.

The most serious problem presented by existing flood-prone structures has to do with buildings that are damaged repeatedly but not beyond 50 percent of their value, the threshold that triggers the requirement to rebuild to specified safer elevations. Varying definitions of repeated damaged structures have been used over the years. For purposes of establishing eligibility for increased cost-of-compliance coverage, the 1994 Reform Act defines a repeatedly damaged structure as one "covered by a contract for flood insurance under this title that has incurred flood-related damage on two occasions during a 10-year period ending on the date of the event for which a second claim is made, in which the cost of repair, on the average, equaled or exceeded 25 percent of the value of the structure at the time of each flood event."

This definition, which applies only to properties experiencing 25 percent or more damage at the time of each loss, is more limiting than the one that the program has historically used to track repetitive losses. Properties falling within the 25 percent threshold number about 9,000. If the 25 percent threshold is not used, the number rises to 76,000. However, these properties account for over 200,000 paid losses, almost one-third of the program's total paid losses, and the $2.8 billion paid on

these losses represents about 35 percent of the $8 billion paid over the history of the program. One hopeful sign is the fact that less than half of the 76,000 buildings that have experienced multiple losses are currently insured by the NFIP. This suggests that these properties are gradually being removed from the floodplain either by demolition or relocation, consistent with program intent.

Section 1362 of the NFIP legislation was intended to partially address existing floodplain structures. This provision authorized the NFIP to purchase certain insured properties that had been either substantially or repeatedly damaged and transfer the land to a public agency for sound floodplain use. Funds were appropriated for Section 1362 annually from 1980 until 1994, when the Section 1362 program was replaced by the Mitigation Grant Program. Over the period during which funds were available, approximately 1,400 properties were purchased at a total cost of about $51.9 million. Properties were purchased in 28 states, with the largest number in Texas, Illinois, Missouri, Oklahoma, and Mississippi.

While Section 1362 has been of some use in reducing the program subsidy, the 1994 Reform Act focused on the need to provide additional mitigation tools both to protect the financial stability of the National Flood Insurance Fund and to promote a more rapid accomplishment of the floodplain management goals of the program through addressing existing flood-prone structures. The Reform Act's three major provisions were:

The establishment of a national Flood Mitigation Fund to provide grants to states and municipalities for a variety of measures to address local circumstances related to serious flood hazard. The funds for these grants come from the federal policy fee and from financial penalties imposed on lenders found to be out of compliance with the mandatory purchase provisions of the act. [The NFIP interpreted the Omnibus Reconciliation Act of 1990 as requiring that the mitigation grant program funds, like other mitigation costs, come from the federal policy fee rather than from premiums (P.L. 101-508).] The Mitigation Grant Program replaces two mitigation programs: the previously described purchase of property under Section 1362 of the act, and the Upton-Jones program (discussed below). It also expands the latitude available to local communities in the use of such funds.

Extension of coverage under a flood insurance policy to include the additional cost needed to meet NFIP building standards after

a flood (i.e., increased cost of compliance coverage). Prior to the legislation, the flood policy could only provide coverage to restore a damaged property to its pre-flood condition. This created the awkward situation for the NFIP of requiring that substantially damaged structures meet the program's elevation standards without making available the financial resources necessary for reconstruction. As noted above, the act extended the coverage not only to properties suffering substantial damage (i.e., damage in excess of 50 percent of their value), but also to repetitively damaged properties.

Statutory recognition of the Community Rating System. As described previously, the CRS was initiated in 1990 and puts into practice the recommendation of the 1966 report for incentives to states and local governments for wise management of flood-prone areas.

There have been other efforts over the years to address the problem of existing flood-prone structures. In the 1970s, following a severe coastal storm, the NFIP experienced a number of claims on damaged properties in the Outer Banks of North Carolina whose locations made repair and reconstruction on the same site problematic. Ongoing erosion and the structures' locations relative to the shoreline made it virtually inevitable that another storm would damage them again, at further cost to the NFIP. The administrator of the FIA decided that it would be more cost-effective in the long term to authorize an additional expenditure under the policy to move the structures back away from the coast on the same lot rather than simply rebuilding them in the same place.

A later legal opinion by the Office of General Counsel held that such a decision could not be left to the discretion of the administrator unless criteria were established that would make any insured property in a similar circumstance eligible for such a benefit. The use of the policy contract in this manner to promote mitigation objectives generated a certain amount of controversy, and it was decided that it would be too difficult to develop a program that would result in the kind of consensus needed to be effective.

Erosion

One of the major issues that faces the NFIP in coastal states is the problem of erosion, of which the state of North Carolina provides a good illustration.

The North Carolina Division of Coastal Management determined in 1986 that, of the 237 miles of North Carolina's oceanfront shoreline surveyed, approximately 73 percent was eroding, with almost 5,000 buildings inside the 60-year setback line, and 777 inside the ten-year line. The state of North Carolina has an active coastal zone management program under the auspices of the Coastal Resources Commission (CRC), which has designated "areas of environmental concern" (AEC) in which uncontrolled development might cause irreversible damage to property, public health, and the natural environment. One of the four categories of AEC is the ocean hazard system that covers lands that are along the oceanfront and inlets and are vulnerable to storms, flooding, and erosion.

With respect to the erosion hazard specifically, the CRC in 1977 adopted coastal erosion hazard regulations and established statewide oceanfront setback standards. The setbacks are based on average annual long-term erosion rates, natural features at the site, and the type of development. The erosion setback line extends landward from the first line of natural vegetation to a distance equal to 30 times the average annual erosion rate at the site. Large-scale development, such as motels and condominiums, must meet an additional setback requirement.

The current statute governing the NFIP does not allow the rate structure to reflect the erosion hazard, which prevents the program from buttressing local coastal regulation with a financial leverage. The bill that eventually became the 1994 Reform Act originally contained a provision that would have allowed the program to charge for the erosion hazard and to impose setback requirements on erosion-prone properties. This provision was removed from the final version and replaced by a section calling for a study of the economic effects of such a provision.

The 1973 act added flood-related erosion as a covered peril under the NFIP, and in 1985, the Upton-Jones provisions were added to the act, extending coverage to structures whose foundations were being gradually undermined by erosion, but which had not yet suffered any actual physical damage that could qualify as the basis for a claim. Upton-Jones made coverage available under the NFIP so that properties "in imminent danger of collapse" due to flood-related erosion could be either demolished or relocated to a safer site before experiencing a flood.

The effectiveness of the Upton-Jones provisions as a mitigation tool has been questioned. A 1988 Congressional Research Service report to Congress noted that "some critics of the Upton-Jones amendment point out that it does not provide an appropriate quid pro quo: the NFIP provides

an increased benefit of insurance coverage for erosion-threatened structures; but beneficiaries do not pay the cost of this benefit, either (for policyholders) through increased premiums related to increased risk, or (for communities) through increased mitigation action to prevent future losses" (Simmons, 1988).

The Upton-Jones provision was eliminated by the National Flood Insurance Reform Act of 1994 and subsumed into the new Mitigation Grant Program. During the period when benefits were available under Upton-Jones, 385 structures were demolished, at a cost of $29.9 million, and another 141 structures were relocated, at a cost of $5.2 million. A small number of claims remain to be closed.

Coastal Barrier Resources System

In 1982 Congress enacted the Coastal Barrier Resources Act (CBRA) (P.L. 97-348, 16 U.S. Code, sec. 3501 et seq.), which was amended in 1990 by the Coastal Barrier Improvement Act (P.L. 101-591, 104 Stat., 2931). This legislation was implemented as part of a Department of the Interior (DOI) initiative to preserve the ecological integrity of the barrier islands—areas that serve to buffer the U.S. mainland from storms and provide important habitats for fish and wildlife. In order to discourage further development in certain undeveloped portions of the islands, the law prohibits new federal financial assistance, including federal flood insurance, in areas that DOI designates as part of the Coastal Barrier Resources System (CBRS). The CBRS was originally composed of 186 units and was expanded to 560 units in 1990. There are CBRS units in 22 states, Puerto Rico, and the Virgin Islands.

The NFIP implements the coastal barrier legislation by amending the flood insurance rate maps (FIRMs) of affected communities to show the CBRS areas, and issues no policies in those areas. Consistent enforcement, however, is difficult. Since flood insurance applications are processed on the basis of community numbers, and portions of communities having CBRS units eligible for insurance, the NFIP must depend on the vigilance of insurance agents to distinguish which areas of a community are eligible for coverage and which are not.

A review conducted in 1992 by the General Accounting Office (GAO) found not only that significant new development continued to occur in certain CBRS units after the law was enacted, but also that NFIP coverage was written on 9 percent of the residences in the units sampled. Unable to rely on total accuracy of underwriting information at the point

of application, the NFIP has depended on post-claims underwriting to deny claims on CBRS properties ineligible for coverage, but the GAO has found this to be a less than ideal response to the problem. The NFIP continues to face a challenge in this area.

Map Revisions

One of the NFIP's important ongoing responsibilities is the updating of FIRMs. These maps need to be updated because of changes in stream channels, local development, coastal erosion, or construction of floodworks. In addition, the 1994 Reform Act required that every community be screened at least once every five years to determine the need for a map revision. Since funds for these revisions are limited, they are prioritized based on a cost-benefit analysis of candidate communities, with the most weight given to communities where development is greatest or most likely.

A particular form of map revision that does not result in the issuance of a new map is the Letter of Map Change (LOMC), which can be either a Letter of Map Amendment (LOMA) or a Letter of Map Revision (LOMR). LOMCs are issued to accommodate properties in special flood hazard areas that are elevated above the base flood level either because of natural topography (in which case the LOMA is issued) or through the use of fill (LOMA-F). In these situations, revisions are generally requested by property owners who want to be exempted from the mandatory purchase of flood insurance. While the LOMA issued because of local topography reflects natural conditions, the LOMA-F based on fill tends to encourage the shift of risk from the elevated property to other properties in the area.

Requests for LOMCs have steadily increased over the past five years. In 1993, there were about 2,800 such requests; in 1997 the number exceeded 11,000. Because the primary purpose for requesting a Letter of Map Change is to excuse the owner from purchasing flood insurance, the entire LOMC process represents a rather shortsighted attitude toward the value of insurance as well as an under appreciation of the flood peril.

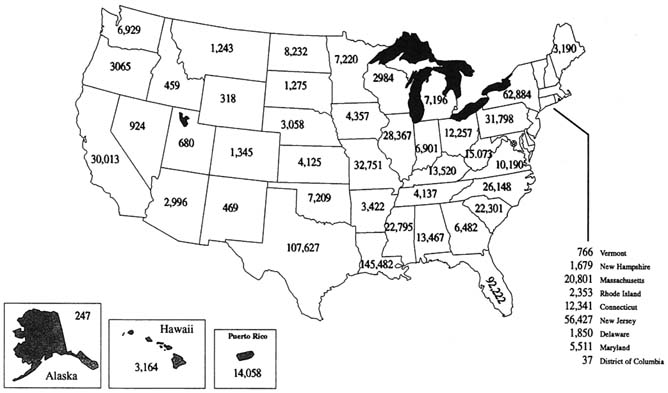

Market Penetration

As shown in Table 6-1, NFIP policies in force stand at about 4 million as of January 31, 1998, with total premiums of $1.5 billion and

TABLE 6-1 NFIP Policies, as of January 31, 1998

State Name | Policies | Contracts | Coverage | Premium |

Alabama | 31,267 | 23,693 | $3,040,828,800 | $12,590,206 |

Alaska | 2,269 | 2,124 | 253,792,900 | 894,127 |

American Samoa | 177 | 147 | 22,725,800 | 80,057 |

Arizona | 25,844 | 25,061 | 2,787,814,000 | 9,370,586 |

Arkansas | 13,132 | 12,994 | 830,143,900 | 4,804,696 |

California | 379,227 | 361,986 | 54,938,258,200 | 148,117,394 |

Colorado | 14,601 | 13,010 | 1,604,555,200 | 6,393,360 |

Connecticut | 26,607 | 22,093 | 3,422,757,700 | 15,770,825 |

Delaware | 14,216 | 10,543 | 1,766,024,500 | 6,384,508 |

District Columbia | 335 | 86 | 19,704,400 | 83,424 |

Florida | 1,635,721 | 1,102,863 | 190,579,653,100 | 526,508,110 |

Georgia | 51,823 | 49,362 | 6,774,150,700 | 22,160,783 |

Guam | 155 | 155 | 18,201,200 | 103,000 |

Hawaii | 45,536 | 14,117 | 5,334,955,100 | 13,713,026 |

Idaho | 8,128 | 8,016 | 1,228,966,300 | 2,787,577 |

Illinois | 46,254 | 42,595 | 3,995,726,500 | 19,576,667 |

Indiana | 25,216 | 25,178 | 1,731,097,400 | 10,674,440 |

Iowa | 9,763 | 9,749 | 721,136,400 | 4,616,649 |

Kansas | 10,069 | 10,032 | 710,527,200 | 4,158,461 |

Kentucky | 22,264 | 21,979 | 1,350,636,100 | 8,598,709 |

Louisiana | 334,045 | 327,369 | 32,888,330,600 | 119,883,650 |

Maine | 6,443 | 6,029 | 652,649,200 | 3,524,444 |

Maryland | 45,678 | 27,843 | 4,516,394,900 | 14,800,547 |

Massachusetts | 35,098 | 31,007 | 4,162,194,200 | 21,558,946 |

Michigan | 26,293 | 25,019 | 2,241,978,500 | 11,341,981 |

Minnesota | 13,184 | 12,889 | 1,137,582,800 | 4,572,150 |

Mississippi | 41,378 | 40,606 | 3,491,664,200 | 15,302,304 |

Missouri | 22,754 | 22,636 | 1,897,445,800 | 11,454,638 |

Montana | 9,570 | 9,397 | 976,254,500 | 2,919,701 |

Nebraska | 11,941 | 11,888 | 854,533,700 | 4,776,598 |

Nevada | 11,877 | 11,791 | 1,575,761,300 | 4,993,559 |

New Hampshire | 4,211 | 3,673 | 393,918,500 | 2,097,915 |

New Jersey | 157,534 | 133,893 | 19,332,025,400 | 81,685,889 |

New Mexico | 10,373 | 10,266 | 812,552,600 | 3,824,770 |

New York | 87,543 | 82,833 | 10,876,776,400 | 49,791,682 |

North Carolina | 73,660 | 65,141 | 8,843,212,300 | 31,423,193 |

North Dakota | 12,686 | 12,497 | 1,257,150,200 | 3,949,441 |

Ohio | 33,144 | 31,864 | 2,386,721,400 | 14,329,736 |

Oklahoma | 14,182 | 14,022 | 1,076,584,300 | 5,532,267 |

Oregon | 21,159 | 20,313 | 2,675,936,700 | 9,423,163 |

Pennsylvania | 62,885 | 61,536 | 5,590,188,100 | 29,312,187 |

Puerto Rico | 41,179 | 36,574 | 2,118,391,800 | 12,103,412 |

Rhode Island | 10,579 | 9,176 | 1,260,573,200 | 6,668,231 |

South Carolina | 105,847 | 74,823 | 14,796,686,500 | 43,794,852 |

South Dakota | 4,528 | 4,528 | 456,029,100 | 1,705,060 |

Tennessee | 13,104 | 12,725 | 1,262,243,700 | 5,472,716 |

Texas | 280,215 | 265,240 | 32,721,302,200 | 102,971,224 |

State Name | Policies | Contracts | Coverage | Premium |

Trust Terr. of Pacific | 1 | 1 | 319,900 | 496 |

Utah | 2,369 | 2,015 | 273,127,800 | 909,735 |

Vermont | 2,422 | 2,375 | 202,402,600 | 1,247,577 |

Virgin Islands | 2,458 | 2,169 | 233,525,300 | 1,292,508 |

Virginia | 63,200 | 55,054 | 7,364,603,500 | 23,198,088 |

Washington | 25,757 | 25,093 | 2,883,529,900 | 11,054,833 |

West Virginia | 18,072 | 18,033 | 1,034,512,200 | 7,729,741 |

Wisconsin | 11,707 | 11,584 | 865,058,800 | 5,028,062 |

Wyoming | 2,818 | 2,812 | 388,351,800 | 1,092,419 |

Unknown | 58 | 40 | 5,992,600 | 20,756 |

TOTAL | 3,982,556 | 3,240,537 | $454,638,161,900 | $1,488,175,076 |

Source: National Flood Insurance Program. | ||||

aggregate coverage of $455 billion. Single-family residences account for almost two-thirds of all policies in force (PIF). Nonresidential (commercial) structures account for only about 4.3 percent of all PIF. Definitive figures on the potential market for flood insurance are difficult to obtain. A conservative estimate is that the current 4 million NFIP policies represent less than half of those property owners who should carry the coverage. The reasons that have been given for this low market penetration are varied:

Many floodplain residents underestimate the seriousness and likelihood of flooding.

Lenders have not been especially zealous in requiring the purchase of flood insurance as the law requires.

NFIP policies are unique, difficult for insurance agents to write, and therefore not marketed aggressively. Because they are single-peril policies, they are viewed as more costly than other lines of coverage.

Many potential consumers expect that federal disaster assistance will adequately provide for post-flood recovery.

Many people are simply misinformed about or unaware of the availability of national flood insurance.

The 1994 Reform Act was intended to address some of these factors. The NFIP has also launched a series of initiatives to simplify the process

of writing a policy, and to market the product on a scale comparable to other insurance products. While the role of lenders is critical to public acceptance of flood insurance as a routine means of financial protection, there is continuing evidence that floodplain residents need to be better informed about both the availability and the value of flood insurance.

In 1995, the NFIP hired the advertising firm Bozell Worldwide to conduct a major marketing campaign called ''Cover America" to raise the national consciousness on the matter of flood insurance and to increase the NFIP policy base. In the first two years of this campaign, the policy base increased by about 20 percent, which compares with an average annual growth rate of about 4 percent.

Subsidy Reduction

Currently, about 35 percent of NFIP policies are subsidized to some degree, which costs the program approximately a half billion dollars in annual premiums. Subsidization was built into the program both to avoid unfairly burdening existing floodplain residents who had built without full knowledge of the risk, and as an incentive to communities to regulate the location and quality of future floodplain construction. To the extent that the mitigation components of the program are effective, the subsidy will necessarily shrink. There have been impressive examples in recent storms demonstrating that mitigation measures that meet program standards are effective in reducing losses. However, the turnover in subsidized housing stock has not occurred as anticipated. Further, a relatively small number of structures that have suffered repetitive damage over the years, but not to a level exceeding 50 percent of their value, have accounted for a disproportionate percentage of the program's total losses. These structures continue to qualify for subsidization, a circumstance addressed by the Reform Act.

Acknowledging the requirement to provide some level of subsidy to existing structures, the program has attempted, since 1981, to accelerate the reduction of the amount of subsidy on individual policies without raising premium costs past the point of reasonableness. The annual rate review continues to result in reduction of subsidies.

Any strategy to reduce the subsidy is influenced by the political climate in which the program has to operate. There are conflicting pressures to both reduce and maintain the subsidy, and the public attitude toward subsidies varies with the national mood at the moment. In the immediate aftermath of a major event like the Midwest flooding of 1993,

Midwest floods of 1993. Houses protected by levees, St. Genevieve, Missouri (FEMA, Andrea Booher).

there is often a general lack of support for allowing people to continue to occupy the floodplain with no financial consequences. However, when measures are proposed to address the problem, the public has often for-gotten the storm and changed its sentiments.

Reducing the program subsidy without losing public support for the program will depend on remaining attuned to the public mood at the time. Of course, an elimination of the subsidy that pushes premiums to levels that are unaffordable for many would also likely increase the demand for alternative forms of public assistance, which in the long run are more costly than the subsidy. The 1994 Reform Act authorized a study to assess the economic effects of eliminating the program subsidy. This study is being conducted by Price Waterhouse and is scheduled for completion in summer of 1998.

Relationship to Federal Disaster Assistance

The effect of federal disaster assistance on the NFIP is more complex than may at first be apparent. The availability of federal disaster assistance is often cited as a reason why floodplain residents do not purchase flood insurance. For example, one of the recommendations of the Interagency

Floodplain Management Review Committee, which studied the 1993 Midwest flooding, was that post-disaster benefits to those eligible to buy insurance be reduced. The prevailing public impression is that federal disaster assistance is generally equivalent to the financial protection provided by hazard insurance. In reality this is not the case. In most flood disasters, the primary mode of federal assistance provided to property owners after a disaster is a low-interest loan from the Small Business Administration (SBA). Disaster victims who are deemed unable to repay an SBA loan can receive an Individual and Family Grant (IFG) from FEMA. However, the amount of these grants is limited to a maximum of $13,000, and they are intended to address reasonable needs and necessary expenses, not to make the grant recipient "whole."

Despite the fact that insurance protection is preferable to either a loan or a grant, the public often perceives otherwise, and this public perception serves as a deterrent to the purchase of flood insurance. Lack of interest in coverage is also due to the attitude expressed by many residents of hazard-prone areas that "it can't happen to me," so why think about protection from disasters? In addition, personal budget limitations can prevent many individuals from voluntarily investing in insurance and other mitigation measures (Kunreuther, 1996). The NFIP's marketing campaign has attempted to reveal the relative inadequacy of federal disaster assistance compared with flood insurance and the reality of the risk facing those who live in high-hazard areas.

A less frequent but more problematic form of federal disaster assistance is the buyout program authorized by the Robert T. Stafford Disaster Relief and Emergency Assistance Act. Buyouts are one of the eligible activities of the Hazard Mitigation Grant Program. This program makes available an additional 15 percent of the total federal disaster expenditures in a given disaster to be used for mitigation purposes. The objective of the buyout program following a flood is to use the opportunity presented by a serious flood to pay for the relocation of victims out of the floodplain, thereby reducing the costs of future flood disasters. This program was used extensively after the 1993 Midwest floods, and it was employed in the wake of the 1997 floods in North Dakota, Minnesota, and South Dakota. The city of Grand Forks, North Dakota, was especially hard hit by the 1997 floods and the buyout process is still ongoing for much of the affected area.

When buyouts are authorized, they are available to all affected residents of a targeted area, whether they are insured or not. While the NFIP can accurately claim that insurance coverage is preferable to a disaster

loan or grant, a buyout results in a much larger payment to the property owner than an insurance policy. To the extent that floodplain residents begin to presume the availability of buyouts in the event of a flood, the incentive to purchase flood insurance is significantly reduced. Residents of Grand Forks who purchased flood insurance in response to a January 1997 NFIP marketing campaign have voiced this very concern. FEMA is analyzing ways to better coordinate both programs.

The 1973 Flood Disaster Protection Act required recipients of federal disaster assistance who live in the floodplain to purchase flood insurance as a condition of the assistance. The 1994 Reform Act reinforced, and in fact strengthened these requirements by including a provision denying any future assistance to anyone who receives federal disaster assistance in the aftermath of a flood and fails to purchase and maintain flood insurance in force. While this provision is designed to promote the purchase of flood insurance, it has its greatest potential impact on grant recipients, who are generally in lower-income categories than those receiving loans and thus less likely to be able to afford insurance. Whether the threat of denial of future federal assistance will have the intended effect of promoting insurance purchase among this segment of the population remains to be seen. The question must be raised as to whether insurance is the mechanism best suited to provide financial protection to a low-income population.

Future Role of the Private Insurance Industry

As discussed above, the original role contemplated for the insurance industry in the NFIP was to underwrite the coverage, with financial backing as needed from the government. That arrangement ended in 1977, and since that time the industry has performed in various ways in the role of fiscal agent to the program, even with the more extensive involvement of the industry under the WYO program. Initiatives have been proposed to formulate an all-hazards type of insurance that would cast the industry into the role of underwriting the coverage, with provisions for the government to reinsure losses over a certain level. The most recent proposal did not include flood insurance and presumed the continuation of the NFIP. At this point, these initiatives seem to be making little progress. As we gain more and more experience with the flood program, if the subsidy continues to recede, and if the insurers remain committed to the program, it is inevitable that the feasibility of having private insurance companies again underwrite a significant portion of the coverage

will surface for discussion. Lloyd's of London, for one, is now able to provide a certain level of private flood coverage because of the more favorable market environment created by the NFIP. One of the concerns expressed over the privatization of flood insurance is whether the vital connection between the availability of flood insurance and the local community enforcement of floodplain management provisions can be maintained. Unless this local enforcement continues, any significant privatization of flood insurance is not likely to be financially feasible.