Paying the Price: The Status and Role of Insurance Against Natural Disasters in the United States (1998)

Chapter: 3 Demand for Disaster Insurance: Residential Coverage

CHAPTER THREE

Demand for Disaster Insurance: Residential Coverage

RISA PALM1

WHY IS THERE LIMITED DEMAND for disaster insurance? If people understood that they can protect themselves from catastrophic losses with a small investment in insurance, would they purchase coverage? Several studies on how people make decisions when faced with unlikely, but possibly disastrous events provide considerable insight into why many residents in hazard-prone areas do not purchase insurance voluntarily to protect themselves against losses from future disasters (Camerer and Kunreuther, 1989). Despite the intuitive appeal of the axioms associated with normative models of choice, the plain fact is that few individuals behave according to expected utility theory—that is, most individuals do not select the strategy that maximizes expected utility. Instead, it appears that the weights on probability and outcomes in judging different alternatives are contingent on the problem context or the framing of different options (Tversky and Kahneman, 1981). What are the factors that affect the decision to purchase disaster insurance? And, more generally, how do human beings adjust to risks in their environments?

FACTORS INFLUENCING THE PROTECTION AGAINST HAZARDS

Survey research has explored the relationship between protection against specific risks and a series of factors such as income level, age, gender, and prior experience with the hazard. In general, empirical research has found that lower-income persons, non-white individuals, women, the elderly, and persons with previous disaster experience will show greater fear of the hazard. In some, but only some, of these cases this fear will also be translated into the adoption of measures to avoid losses, such as buying disaster insurance. Frequently survey research findings have been contradictory, and, even more frequently, have not been explained by reference to an overarching theoretical perspective (Drabek, 1986).

Another line of research, more theoretically based, goes beyond individual characteristics or experience to describe the process of decision making. The simplest theoretical framework for predicting the purchase of insurance is an analysis of the ratio of expected benefits to certain costs. In theory, it is possible to assess the probability of losses of different magnitudes for a piece of property in a given year, and then calculate the relative costs of purchasing insurance and receiving claim payments. The property owner could then compare this amount to the estimated cost of no insurance premium combined with absorbing the costs of repairs oneself should the property be damaged. For this type of cost-benefit analysis to predict not only the ''ideal" practice, but also the observed practice, the decision maker must have the goal of maximizing expected utility and must possess all relevant information about costs and benefits in an uncertain world. Since these assumptions about omniscience cannot be met in actuality, this conceptualization is modified into one of subjective expected utility (Edwards, 1955; Friedman and Savage, 1948; Mosteller and Nogee, 1941).

However, even with this modification, empirical studies show that besides a lack of information, other factors prevent decision makers from undertaking even simple cost-benefit analysis. For one thing, individuals often exhibit a set of biases with respect to their estimates of the probability in making judgments under uncertainty. For example, they may be prone to the gambler's fallacy—believing that if a low-probability event has occurred recently, it is unlikely to occur again soon and therefore can be treated as an event with a probability of zero (Slovic et al., 1974).

Individuals may utilize a set of probability rules through an editing procedure to simplify the choice process. For example, decision makers may equate low probability with zero probability, which enables them to ignore certain alternatives (Kahneman and Tversky, 1979; Slovic et al., 1977). They may anchor their estimate of a loss on a salient figure and then adjust their estimate around this first approximation—an approximation that may be highly inaccurate and will bias later estimates (Einhorn and Hogarth, 1985; Tversky and Kahneman, 1974). In short, the notion that individuals calculate the costs and benefits of various alternatives and decide on some set of "rational" adaptations to the environment does not fit the empirical reality of complexity in decision making. Individuals not only lack complete knowledge of alternatives, but also demonstrate patterns of consistent "errors" in risk calculation.

Kunreuther (1996) argues that individuals tend to make different trade-offs between such issues as the probability of the event or its likely outcomes depending on the context of the problem and the means used to communicate the information. "People often weight these dimensions differently than would be suggested by normative models of choice such as expected utility theory or benefit cost analysis" (Kunreuther, 1996, p. 175). For example, some people may show little interest in adopting insurance against natural hazards because they believe that it "cannot happen to me." People may not adopt protective measures because they are myopic in their view of the future and are therefore unprepared to pay the relatively high up-front cost in relation to these perceived short-run benefits.

On the other side of the coin, the decision to purchase earthquake insurance is a specific example of what Hogarth and Kunreuther label "decision making under ignorance," where both costs and benefits are unknown to the decision maker. In such conditions, these authors argue, "people determine choices by using arguments that do not quantify the economic risks and may reflect concerns that are not part of standard choice theory" (Hogarth and Kunreuther, 1995, p. 16). Instead, people justify their decisions using arguments that may seem far-fetched or may not resemble normative models of choice.

Individual decision making may also take place in cultural contexts that constrain or enable the range of available choices. The cultural context may increase or reduce awareness of risk, and condition the range of acceptable responses. Wildavsky and Dake (1990) note that personality structures are neither risk-averse nor risk-taking in all situations, and therefore tests of such factors cannot predict hazard response. Instead,

"cultural biases provide predictions of risk perceptions and risk-taking preferences that are more powerful than measures of knowledge and personality" (Wildavsky and Dake, 1990, pp. 171–172).

A specific example of the impacts of cultural context on hazard response is the research related to "optimism." A number of studies suggest that, in comparing themselves to others, Americans see themselves as living longer, as being younger for their age, and as less likely to die from cardiovascular diseases or accidents (Myers, 1992). Garrison Keilor's claim that all children of Lake Wobegon are "above average" pokes fun at this tendency. Researchers find an absence of this optimistic bias among Japanese college students (Heine and Lehman, 1995; Markus and Kitayama, 1991).

This American optimism about personal well-being could also affect perceived vulnerability and the propensity to protect oneself from risk by purchasing insurance or taking steps to protect one's home from future disasters. Empirical findings from surveys of Japanese and California homeowners showed that Californians tended to be overly optimistic, to believe their own neighborhoods were safer and better prepared for earthquakes than other areas in their city or region, while Japanese believed their own areas were more at risk and less well prepared (Palm and Carroll, 1998).

FLOOD AND EARTHQUAKE INSURANCE

Many risks stemming from the environment, broadly defined, confront homeowners, from toxic waste spills to civil disorder. This chapter focuses on two major natural hazards facing households—flooding and earthquakes—and, specifically, on the decision to purchase insurance against the damage caused by these hazards. Although wind and tornadoes can cause destruction to residential property, insurance against such damage is usually included in the general homeowners' policy, as pointed out in the previous chapter.

Empirical Evidence Concerning Flood Insurance Purchase

Floods account for more losses than any other natural disaster in the United States, and for more federal disaster assistance in most years. Riverine floods threaten every part of the United States, although damage is highly dependent on local variables.

Since 1968, flood insurance has been provided by the federal government

under the National Flood Insurance Program (NFIP) through the Federal Emergency Management Agency (FEMA). (See Chapter 6 for a comprehensive description of the NFIP.)

Congress sets the rates and terms of flood insurance under the NFIP. The program specifies requirements for building in the floodplain and provides subsidized insurance rates for structures in existence before these requirements were adopted. Federally regulated or insured lending institutions offering home mortgages on property in the 100-year floodplain must require flood insurance as a condition for granting an initial mortgage loan. However, in the past, lenders have permitted mortgage holders to let their flood insurance policies lapse. A recent survey estimates a 70 to 80 percent lapse rate among policyholders after the initial years of the mortgage (KRC Research and Consulting, 1995). Further, since no fine was levied on lenders who failed to comply, there was no economic incentive for them to follow the requirement (Federal Interagency Floodplain Management Task Force, 1992). This has since been corrected by passage of the National Flood Insurance Reform Act of 1994 (P.L. 103-325, 108 Stat., 2255).

During the first four years of the subsidized flood insurance program fewer than 3,000 out of 21,000 flood-prone communities entered the program, and fewer than 275,000 homeowners voluntarily bought a flood insurance policy. Insurance agents had little economic incentive to sell this separately marketed insurance since their commissions were low relative to the time required to market coverage (Kunreuther et al., 1978). By 1992, a conservative estimate of coverage suggests that less than 20 percent of the homes located in the floodplain were covered by flood insurance (Kusler and Larson, 1993). The Federal Insurance Administration estimates that as of 1997 about 27 percent of households living in high-risk flood areas are insured. This estimate is based on about 10 million total households in high-risk zones, with 2.7 million policies in force. About 1 million policies have been sold outside high-risk areas.

The NFIP requires participating communities for which flood maps have been developed to have minimum building codes and standards. Although mapping is completed in most of the communities undergoing development, those unmapped communities cannot implement these building standards (Kusler and Larson, 1993). Thus, new development continues in areas potentially at risk from flooding.

In 1995, the Federal Emergency Management Agency commissioned a study to "facilitate its efforts to sell flood insurance to the public nationwide." KRC Research and Consulting conducted 27 interviews in

August 1995 with lenders, realtors, community officials, and advisory board committee members (KRC Research and Consulting, 1995). Among other things, they found that the public still has little knowledge about flood insurance coverage, just as the Kunreuther team found 20 years earlier (Kunreuther et al., 1978). Individuals purchase policies primarily to comply with regulations rather than because of perceived risk or a desire for the insurance per se.

Empirical Evidence Concerning Earthquake Insurance Subscription

Earthquakes are also a national problem. The highest magnitude (M) earthquake on the Richter scale within North America in the twentieth century occurred in Alaska in 1964 (M = 8.4), and more earthquakes of similar magnitude are predicted for that region. Within the lower 48 states, the highest magnitude earthquake occurred near New Madrid, Missouri at the beginning of the nineteenth century (M = 9.2 in 1812). A recurrence of such an earthquake in this region would wreak havoc, particularly given the relative lack of adequate local construction standards and preparedness.

Earthquake insurance, unlike fire insurance, is not generally required by mortgage lenders as a condition for a mortgage loan. A survey of lenders conducted in 1982 (Palm et al., 1983) found that a majority of home mortgage lenders in California stated that they rarely or never make adjustments in lending terms simply because property is in a landslide-prone area, a special earthquake studies zone, or an area known to be underlain by a surface fault trace, or because of evidence of seismic damage. Lenders in California as well as the state of Washington ranked earthquake hazards as the least likely of five possible causes of mortgage defaults. They report that it is far more likely that default would follow unemployment, divorce, a house fire, or a major flood rather than an earthquake.

Lenders gave several reasons why property owners ignored the earthquake risk. First, most loans are made on post-1940 houses. These houses were built according to some seismic building code, resulting in less vulnerability to major earthquake-related damage. Second, even if the property sustained major damage, lenders believe that there is little probability that the borrowers would default on the mortgage loan as long as they have positive net equity in the home. Third, lenders believe that they spread their vulnerability over such a wide range of investments, and over a sufficiently large geographic area, that even if a major earthquake

occurred in one part of the state, their portfolios would not be subject to major losses. Fourth, lenders who participate in the secondary mortgage market have passed the risk on to others. Fifth, lenders may not use geologic information for lending decisions because of state and federal anti-redlining legislation preventing geographic mortgage lending discrimination. In the 1982 survey, lenders used one or more of these arguments to justify their ignoring of seismic conditions in making loan decisions in California.

Looking at homeowners' decisions to purchase earthquake insurance, we would expect that because of the national distribution of earthquake risk there would also be a national demand for earthquake insurance. However, most of the actual demand is in the state of California, and to date the most comprehensive cross-sectional studies on the demand for disaster insurance have been undertaken in California. At the time of the first systematic survey of earthquake insurance purchase (Kunreuther et al., 1978), only five percent of homeowners were insured against this risk. Over the 20-year period since that survey, several events have occurred that impact insurance adoption: (1) passage of legislation requiring the disclosure of information on earthquake risk and on the availability of earthquake insurance, and (2) the occurrence of several moderate-scale earthquakes.

Hazard Disclosure Legislation

The two most relevant legislative acts are the Alquist-Priolo Special Studies Zones Act and a state law requiring the earthquake insurance disclosure. The Alquist-Priolo Act was passed in March 1972 in response to the San Fernando earthquake of February 1971. This act was intended to prevent new large-scale development or siting of facilities, such as hospitals and schools, in areas particularly susceptible to fault rupture. In 1975, the act was amended to require disclosure that a property was in a special earthquake studies zone: "A person who is acting as an agent for a seller of real property which is located within a delineated special studies zone, or the seller if he is acting without an agent, shall disclose to any prospective purchaser the fact that the property is located within a delineated special studies zone" (California Public Resources Code, sec. 2621.9).

The amended act required purchasers of property within one-fourth mile of an active surface fault trace to be informed about the hazard from fault rupture. The Alquist-Priolo Act was amended again in 1990

to extend the nature of the hazard zones and to mandate disclosure of these new zones. The new law required the State Mining and Geology Board to develop guidelines for the preparation of maps of seismic hazard zones by January 1, 1992, and required the seller or the agent of the seller to disclose "to any prospective purchaser the fact that the property is located within a seismic hazard or delineated special studies zone, if the maps or information contained in the maps are reasonably available." The legislation mandates the mapping of seismic hazard zones, including areas susceptible to "strong ground shaking, liquefaction, landslides, and other ground failure," and specifies additional information that must be disclosed to the potential new purchaser of property.

It is unclear how this new information is being used in the purchase process. An early study of the impacts of special studies zones disclosure on home buyer behavior showed that most buyers did not understand or remember the disclosure (Palm, 1981). The question of whether the modified hazard disclosure mandated in the 1990 legislation results in increased awareness of individual risk exposure merits future study. Because of the required disclosure to prospective property purchasers in the special studies zone, it might be expected that home buyers would translate this increased awareness of the earthquake hazard into the adoption of mitigation measures as well as the purchase of insurance. Although evidence shows an increase in demand for insurance, the specific causes have not been pinpointed.

A second form of disclosure legislation was aimed more broadly at all property owners who carry homeowners' insurance, normally required as a condition for a mortgage loan and purchased by most owners without a mortgage. Insurance companies were required to mention the availability of earthquake insurance and to make clear that fire insurance policies do not cover earthquake damage. The relevant statute (California Insurance Code, sec. 2, 1081) went into effect in 1984. It requires homeowners to be informed biannually of the availability and cost of earthquake insurance and thus might motivate some homeowners to consider purchasing this coverage.

Earthquake Experience

The occurrence of several moderate earthquakes in California between 1983 and 1994 could be expected to have influenced the purchase of earthquake insurance. People do more to prepare for future earthquakes, including buying insurance against them, just after an earthquake

than at any other time. As the memory of the earthquake fades, the motivation for preparedness decreases.

Between the Kunreuther survey in 1974 and the last of the Palm surveys in 1995, six moderate-scale earthquakes occurred. The first was the 6.7 magnitude earthquake at Coalinga in 1983, causing $31 million in property damage and 205 injuries. This earthquake damaged approximately 1,000 housing units, about 40 percent of the total in the city. The 1987 Whittier Narrows earthquake had a lower magnitude (5.9) and resulted in no deaths or serious injuries, but it damaged 5,000 buildings and caused losses of approximately $358 million. The Loma Prieta earthquake of 1989 was a magnitude 7.1 earthquake, which resulted in 62 deaths, 3,000 injuries, damage to 18,300 houses, and property damage of approximately $6 billion.

In 1992, California earthquakes occurred in several locations: the Cape Mendocino earthquake near Petrolia (magnitude 7.0), which damaged numerous historic dwellings, and the Landers/Big Bear earthquake (with magnitudes of 7.6 and 6.5, respectively). The Landers/Big Bear earthquake sequence was the strongest to occur in the state since 1952. It caused 1 death and 25 injuries, and resulted in property losses to private and public buildings in excess of $90 million (Earthquake Engineering Research Institute, 1992).

The most recent damaging earthquake was the magnitude 6.7 Northridge earthquake of January 1994, which resulted in 33 fatalities, most caused by structural failure (Earthquake Engineering Research Institute, 1994). Fifteen people died in a "dingbat" style, three-story wood frame apartment building in Northridge. Although the death count in the Northridge earthquake was very low, the economic consequences of this earthquake were staggering: insured losses topped $12.5 billion (California Insurance Department, 1995), with total losses exceeding $50 billion (Risk Management Solutions, 1995a). Publicity about the disaster raised the awareness of California residents concerning their vulnerability to earthquake damage.

As a result of the increase in seismic activity in California, there was a significant demand for earthquake insurance between 1983 and 1995. In the 1970s less than 10 percent of the homes were insured against earthquake damage. By 1995 over 40 percent of the homes in many areas along the coast were insured against earthquake damage. Since the threat of earthquake damage is much less in the interior of the state, fewer homes are insured for earthquake damage in inland cities such as Fresno and Sacramento.

Survey Findings on Insurance Purchase

Three surveys of a population of owner-occupiers in Contra Costa, Santa Clara, Los Angeles, and San Bernardino Counties in 1989, 1990, and 1993 showed a dramatic increase in earthquake insurance purchase from the 1973–1974 baseline, and a gradual increase in all these counties over the four-year study period (Palm, 1995).

Contra Costa County had the lowest percentage of earthquake insurance purchase, starting at 22 percent insured in 1989 and ending with 37 percent insured in 1993, as shown in Table 3-1. The highest percentage of earthquake insurance purchase was in Santa Clara County, with the percentage of insured properties jumping more than 10 points in the single year following the Loma Prieta earthquake of 1989.

There was a major increase in San Bernardino County, also related to the Landers/Big Bear earthquake sequence. Los Angeles County respondents showed a steady increase in insurance purchase, to a slight majority insured by 1993. Overall, earthquake insurance purchase has increased. However, a large number of households—a majority in San Bernardino and Contra Costa Counties—remain uninsured. An even more comprehensive census of earthquake insurance purchase shows heavy concentrations of insured households in urbanized coastal counties where vulnerability is high.

Reasons for Insurance Purchase

In the 1989–1993 surveys, those who purchased insurance were asked to assess factors that affected their purchase decision. Figure 3-1 shows that the most important motivating factors for those who purchased insurance, in order of importance were: (1) "worry that an earthquake will destroy my house or cause major damage in the future"; (2)

TABLE 3-1 Percent of Survey Respondents Purchasing Earthquake Insurance

|

County |

1989 |

1990 |

1993 |

|

Contra Costa |

22.4 |

29.3 |

36.6 |

|

Santa Clara |

40.4 |

50.9 |

54.0 |

|

Los Angeles |

39.6 |

45.8 |

51.6 |

|

San Bernardino |

29.2 |

34.6 |

42.6 |

FIGURE 3-1 Factors that influenced the decision to purchase earthquake insurance, 1989–1993. Note: CRERF = California Residential Earthquake Recovery Fund (see below).

"most of our family wealth is tied up in the equity of our house, which might be lost if an earthquake destroyed or damaged it"; (3) "if a major earthquake occurs, the damage to my house will be greater than the deductible, so insurance is a good buy"; and (4) "if a major earthquake occurs the grants or loans available from the federal or state government will not be sufficient to rebuild my house." The mean score for each of these factors was at least 3.5 (where 5 was "very important" and 1 was ''not at all important").

The least important reasons for purchasing insurance were "my neighbors or friends or relatives or colleagues convinced me to have earthquake insurance," "my real estate agent encouraged me to buy it," and "my mortgage lender suggested that I have it." Insurance purchase was thus motivated by anticipated losses, fear that governmental aid will be unavailable or insufficient, and an estimate of likely damages as opposed to the cost of premiums. The influence of family, friends, real estate agents, or mortgage lenders was negligible.

These findings represent a change in the factors influencing the purchase decision since the time of the Kunreuther survey of 1973–1974. In the earlier survey, knowing someone with insurance and talking about insurance with someone were among the most influential factors in causing the household to consider insurance and to purchase it. The shift from the influence of friends and neighbors to more economic motivations (the subject's own judgment about anticipated losses, potential government

aid, and the probability of an earthquake) may be due to the passage from an early stage of the diffusion of an innovation to a later stage in the adoption process, demonstrating the existence of a more mature market for earthquake insurance. That is, when earthquake insurance was relatively new and uncommon, it took a personal acquaintance with an insured individual to motivate the spread of insurance among California households. At present, since so many people already have earthquake insurance, assessments of risk and cost have become the motivating factors.

Insuring the Deductible

In 1992 the State of California experimented with a fund to provide insurance of up to $15,000 to cover losses associated with the deductible on catastrophe insurance. The California Residential Earthquake Recovery Fund (CRERF) levied a surcharge of from $12 to $60 (depending on location and type of dwelling) on residential and mobile home insurance policies. Coverage of up to $15,000 would be guaranteed only for the structure, with deductibles of $1,000 to $3,500 depending on the value of the house. As pointed out in Chapter 4 (p. 73), an estimated 90 percent of California homeowners paid the surcharge for this program, but the program was repealed in September 1992.

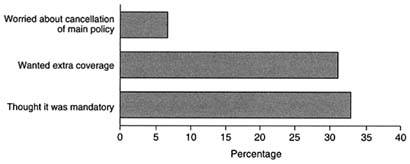

The 1993 survey asked homeowners whether they had paid this surcharge and the reasons for their decision. Although the program was short-lived, and perhaps of only historic interest, their responses have important implications for the success of future programs, whether marketed through private insurance companies or again through governmental guarantees. In the 1993 survey, overall 59 percent of the respondents said that they had paid the surcharge. (This is less than the 90 percent participation mentioned earlier because it includes policies that went into effect after 1992 and were thus ineligible for CRERF coverage.) Contra Costa County respondents showed the lowest purchase percentage (54 percent), and Santa Clara, Los Angeles, and San Bernardino Counties ranged from 61 to 62 percent subscription to the CRERF. As depicted in Figure 3-2, most of those who paid the CRERF surcharge did so because they wanted the extra coverage and/or they thought it was mandatory.

In contrast, those who did not pay the surcharge had a variety of reasons—primarily they believed they did not need this type of policy, or they doubted the permanence or soundness of the program (see Figure 3-3).

FIGURE 3-2 Why respondents paid CRERF surcharge.

These survey findings suggest that any future program, even with relatively low premiums and covering most of the potential losses, must seem dependable to the potential purchasers or the program will not be adopted.

Who Purchases Insurance?

The 1989–1993 surveys found that the propensity to buy insurance was not consistently or systematically related to the demographic or economic characteristics of the homeowners. Although factors such as income, age, and length of residence in California might be statistically associated with earthquake insurance purchase in one county or another, these variables did not, individually or collectively, distinguish the insured from the uninsured in the four counties surveyed. However, individual estimation of potential destruction of the home by an earthquake was the variable most closely associated with the purchase of insurance.

Surveys in 1994 and 1995

More recent information has been collected about insurance purchase behavior of Californians. The general purpose of this study was to compare the possible impacts of culture-based personality factors on earthquake hazard response and the adoption of mitigation measures in areas of similar hazard in California and Japan (Palm and Carroll, 1998). The California study areas—Cupertino, Redlands, and portions of the western San Fernando Valley—were selected as areas of predominantly owner-occupiers, who were also white and middle class. Table 3-2 shows

FIGURE 3-3 Why respondents did not pay CRERF surcharge.

that earthquake insurance purchase ratios were quite high in all three study areas, exceeding two-thirds of the respondents in the case of Cupertino.

As in previous studies, perceived risk was strongly related to the tendency to adopt earthquake insurance: those who were more worried about earthquakes, and who believed that their own homes were likely to be damaged by an earthquake in the next ten years, were also more likely to purchase earthquake insurance.

In order to assess the types of measures individuals and households in the study areas adopted, we presented them with a checklist derived from a composite of the various measures suggested in the Homeowner's Guide to Earthquake Safety developed by the California Seismic Safety Commission in response to 1991 legislation (Government Code, Title

TABLE 3-2 California Earthquake Insurance Purchase in 1995

|

Study Area |

Percentage Who Purchased Earthquake Insurance |

|

Cupertino |

67.2 |

|

Redlands |

47.7 |

|

Western San Fernando Valley |

53.9 |

The Northridge Meadows Apartments, where 16 people were killed in the Northridge earthquake of 1994. The top two stories collapsed onto the first floor, which had garages at either end, with apartments in the middle. The apartment buildings were constructed with joist hangers that were too small, and joists were not nailed to hangers. Shear walls were not made of plywood but gypsum board. There was reduced shear strength on the lower floor because of the garages. Steel supporting beams bent and collapsed (USGS, J. Dewey).

21, Division 1, Chapter 1.38). Other items were added or deleted in response to suggestions by members of the advisory committee to create a final list of eleven items ranging in cost from strengthening the house itself to cost-free items such as making plans for reuniting the household after an earthquake or planning an escape route.

We found that the purchase of earthquake insurance was positively associated with certain mitigation measures taken in the home, such as arranging heavy objects so that they were less likely to fall, participating in earthquake drills, purchasing a fire extinguisher, and investing in measures that would strengthen the house. Earthquake insurance purchase, however, was not related to the adoption of mitigation measures such as preparing an escape plan, storing food and water, making plans for family reunions after the earthquake, storing items in a container for evacuation, knowing how to turn off gas and other utilities, or having a first aid kit.

CONCLUSIONS ABOUT EARTHQUAKE INSURANCE PURCHASE

Empirical research has demonstrated that the demand for one form of disaster insurance—insurance against catastrophic losses associated with earthquakes—has greatly increased in recent years. However, there seems to be some limit to demand for this insurance given budget constraints, current premium rates, and perceptions on the part of at least a portion of the population at risk that the probability of disaster is so small that "it cannot happen to me." Those who purchase insurance are worried about destruction from a future earthquake; those who eschew insurance believe it is too expensive, and that their houses are not susceptible to major damage. Clearly, universal, voluntary insurance coverage, even in an area at risk from earthquakes such as metropolitan southern California, is unlikely to be realized.

One should note that the survey data on earthquake coverage reported here only reflects homeowners' decisions in one area of the United States at one period of time (1989–1995). Since that time, the California Earthquake Authority has replaced the private insurance market mechanism with respect to this type of coverage in California. Chapter 4 provides more detailed evidence on the demand for insurance under this new program.

Finally, the decision processes by firms and business organizations in the private and public sectors in other parts of the United States and the world may be very different from those in California. Also, significant cultural differences may affect the decision to purchase coverage in other countries, particularly in non-Western nations.