Incorporating Shock Events into Aviation Demand Forecasting and Airport Planning (2024)

Chapter: 4 Further Examination of the Impacts of COVID-19: Airport Case Studies

CHAPTER 4

Further Examination of the Impacts of COVID-19: Airport Case Studies

This chapter explores the impacts of the COVID-19 pandemic at 11 airports, captured in key themes told through 10 case studies (two San Francisco Bay Area airports were paired into one study). While all airports and the aviation industry in general were impacted by the COVID-19 pandemic, not every airport was impacted in the same way. The mix of operations and air service markets were major factors in determining how traffic at individual airports was affected by the pandemic. With differences in airport operations mix—passenger, cargo, and GA—airport revenues were impacted in different ways as well.

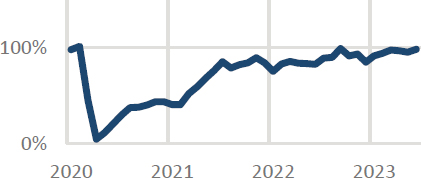

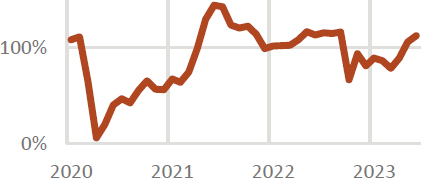

Case Study: San Francisco Bay Area Airports Divergent Recovery Trends

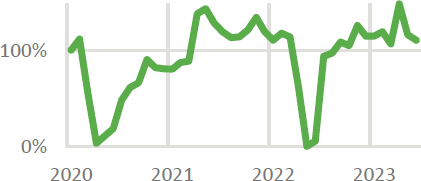

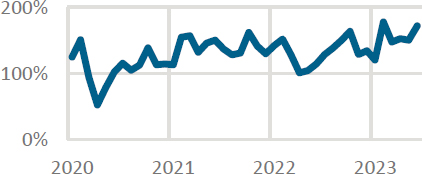

The two largest airports serving the San Francisco Bay area are San Francisco International (SFO) and Oakland International (OAK). SFO is the largest airport in the region, the primary international gateway airport for the region, and a hub for United Airlines and Alaska Airlines. In 2019, 27% of SFO’s passengers were international with a significant air service focus on Asia and trans-Pacific traffic. OAK is the second largest airport in the region, served primarily by low-cost carriers, and a major base for Southwest Airlines.

Among the two airports, OAK’s traffic recovery has outpaced that experienced by SFO throughout the entire pandemic. While OAK does have some international services, those are oriented largely at leisure destinations in Mexico and the Caribbean, which were aligned more closely with the surge in leisure-travel demand in 2021 than the long-haul international services and trans-Pacific markets best served by SFO.

The impacts of COVID-19 on these 11 airports were analyzed through a combination of published data sources, contemporary news stories, and remote interviews involving personnel employed in planning, forecasting, air service development, and finance. Six key themes were identified; they are summarized in the following sections and illustrated with information for selected case study airports.

Table 2 provides an overview of the 11 case study airports. The studies included large, medium, and small hub airports, analyzing the differential impacts on passenger traffic at a variety of airport types. In addition, airports were selected to examine the impact on cargo traffic and GA. The table provides information on the maximum monthly recovery of the relevant activity level—passengers, cargo, or operations—compared to the same month in 2019. While some case study airports have seen their activity grow beyond pre-COVID levels, a number of passenger airports have yet to see recovery to pre-COVID levels as of June 2022.

Key Theme #1: Traffic Reductions and Recovery Rates Depended on Destination Mix and Airline Mix

Throughout the pandemic there was a clear distinction between the impacts and recovery of domestic versus international travel demand and capacity. Across the U.S. aviation industry, domestic passenger traffic recovered faster than international due to the varying range of travel restrictions based on health policies on international travel—from outright travel bans to policies disincentivizing international travel, such as quarantine requirements and testing. Because of these effects, airports that had a high proportion of domestic passengers and service prepandemic (e.g., DEN, OAK) tended to recover faster than airports with a larger international air service market (e.g., SFO, IAD).

Table 2. Comparison of key impact and recovery metrics for case study airports.

| Airport | Airport Type | 2019 Traffic | COVID-19 Impact and Recovery (% Relative to 2019) | Maximum Recovery by June 2023 | Unique Impacts |

|---|---|---|---|---|---|

| Honolulu, HI HNL | Large hub, primary gateway to Hawaii | 10.3 million enplaned passengers |  | 103% | Impacted by state policy to limit visitations in 2021 and slower recovery of international travel demand. |

| San Francisco, CA SFO | Large hub, major transpacific gateway, United Airlines hub | 27.9 million enplaned passengers |  | 89% | Deeply impacted by restrictions on international travel and ongoing slow recovery of Asia market. |

| Oakland, CA OAK | Medium hub, 2nd largest in Bay Area, Southwest Airlines hub | 6.8 million enplaned passengers |  | 92% | Regional LCC focus saw expansion of international services to sunspot leisure destinations. |

| Denver, CO DEN | Large hub, primarily domestic traffic, hub for United Airlines and Frontier | 33.9 million enplaned passengers |  | 117% | High proportion of domestic and LCC traffic led to rapid recovery compared to other large hubs. |

| Washington, DC IAD | Large hub, primary international gateway to DC, 35% of passenger traffic international | 12.0 million enplaned passengers |  | 102% | Large hub with more rapid transcontinental recovery from focus on European market. |

| Airport | Airport Type | 2019 Traffic | COVID-19 Impact and Recovery (% Relative to 2019) | Maximum Recovery by June 2023 | Unique Impacts |

|---|---|---|---|---|---|

| Jackson Hole, WY JAC | Nonhub airport, outdoor leisure-focused destination | 0.5 million enplaned passengers |  | >140% | Outdoor leisure-focused destination in high demand during early pandemic. Temporary traffic shut down in first half of 2022 due to runway rehabilitation project. |

| Birmingham, AL BHM | Small hub, spoke airport | 1.6 million enplaned passengers |  | 99% | Spoke airport with average recovery due to network reorientation by legacy carriers. |

| Fort Myers, FL RSW | Medium hub, leisure destination with international services | 5.1 million enplaned passengers |  | >140% | Injection of LCC traffic to domestic leisure-focused market produced a rapid recovery of passengers but saw a reduction in traffic in 2022/23 as carriers reduced injected capacity as demand diversified from just leisure travel. |

| Pittsburgh, PA PIT | Large hub, cargo | 83 million pounds enplaned air cargo |  | >145% | Expansion of cargo services and major cargo tenants during pandemic helped offset financial impacts of reduced passenger services. |

| Rockford, IL RFD | Nonhub cargo airport, regional integrator/courier hub | 387 million pounds enplaned air cargo |  | >175% | Surge in integrator and e-commerce demand supported strong cargo growth. |

| Van Nuys, CA VNY | Nonhub GA airport, busiest GA airport in the United States | 212,000 aircraft operations |  | >160% | Growth in flight training activity spurred significant increase in operations. |

NOTE: IAD = Washington Dulles International Airport; JAC = Jackson Hole Airport; RSW = Southwest Florida International Airport; RFD = Chicago Rockford International Airport; VNY = Van Nuys Airport.

As the COVID-19 pandemic was a global phenomenon, each country and regional bloc adopted different policies and stances that restricted or enabled travel, either domestically or internationally. This patchwork of policies and regulations led to greater uncertainty for both travelers and airlines in reestablishing international travel. Some nations retained travel restrictions and sanitary policies longer than others, which allowed certain markets to open up faster, while other markets remained slow to recover or effectively closed even into 2022. China, the world’s second-largest aviation market, put in place a “zero COVID” policy that involved effectively closing the nation’s borders to foreign travel for an extended period. By contrast, the United States and Europe saw an earlier opening of borders through a managed set of health policies and risk management but only to certain country and region markets. Therefore, airports that had greater non-stop connectivity or O/D demand to regions or countries that experienced greater travel restrictions and longer returns to allowing discretionary travel, generally experienced greater negative impacts compared to airports with air services and demand oriented toward more rapidly reopening markets.

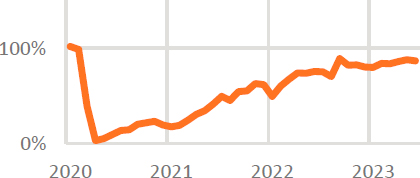

Case Study: Southwest Florida International (RSW) and Jackson Hole Airport (JAC) Leisure-Travel Demand Recovery

Both RSW and JAC are leisure-focused airports, the former located on Florida’s southwestern coast and the latter serving a number of ski resorts and national parks. Leisure demand was one of the first segments of travel demand to return as travel and health restrictions began to be relaxed starting in the summer of 2020. Both case study airports are also gateway destinations for primarily outdoor recreational activities such as beaches, mountains, and national parks rather than dense urban environments.

Both of these airports saw an increase in annual traffic in 2021 compared to 2019 as travelers shifted demand toward domestic destinations amid a period of pent-up demand for leisure travel in 2021 after limitations on travel throughout 2020. Both airports continued to see above-2019 levels of traffic in the first half of 2022 despite dips during the winter season due to the Delta and Omicron waves of COVID-19.

RSW is also an international leisure destination with non-stop air services to Canada and Europe, which grew in 2022 above 2019 levels. As these are leisure-focused services primarily operated by vacation scheduled charter airlines, the airport has been able to grow its international market amid an industry-wide surge in leisure demand in 2021–2022.

Key Theme #2: Traffic Reductions and Recovery Rates Were Influenced by Passenger Market Makeup

Travel patterns and market demand between business and leisure travel were also significantly impacted during the pandemic. As travel restrictions and health policies began to be relaxed starting in the latter half of 2020 and into 2021, leisure travel (including VFR) was one of the first travel segments to begin recovering. Partly as a function of pent-up demand as well as shifts toward domestic leisure travel while foreign markets continued to see travel or health restrictions, the U.S. domestic leisure air travel market saw a relatively quick recovery from the initial impacts of the pandemic.

There was also an observed trend of preference, particularly in 2020 and 2021, for leisure destinations that featured primarily outdoor recreation and activities. With health risks still present and mass vaccination not started or only partially underway, the early phases of the pandemic saw a greater demand for travel to leisure locations with lower population densities than major cities and/or outdoor leisure opportunities. The case studies of Jackson Hole and Southwest Florida are two examples of these types of leisure-focused destinations, with Denver being another case study that capitalized on the outdoor recreation draw of the region. In contrast, Las Vegas (LAS), one of the nation’s top tourist destinations and a major conference and exhibition destination, saw a relatively slow recovery of its traffic demand in 2020 and into 2021. This was likely a combination of the relatively low desirability of Las Vegas’ high-density indoor attractions (e.g., casinos and shows) as well as the restrictions and lack of demand for large-scale conferences and exhibitions during the earlier phases of the pandemic.

In 2020, 2021, and through much of 2022 business and conference travel remained largely below prepandemic levels in the United States and globally. Business travel was impacted by two major factors. First, changes in the ways of working during the pandemic with the rise of work-from-home in the

services sector and the use of video conferencing technologies replaced in-person meetings and visits. Initially, this was due to the necessity of health and travel policies, but as the pandemic progressed, it became more of a norm to conduct business—both internally and externally—virtually rather than in person. The second key factor was company policies that forbade or limited business travel, not only for health safety reasons but also to reduce costs during the economic downturn in the early stages of the pandemic.

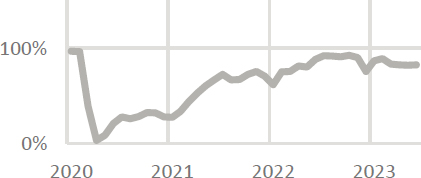

Case Study: Washington Dulles International Airport (IAD) Business Travel Market Impacts

IAD is one of three airports serving the Baltimore-Washington Metropolitan area and the region’s primary international gateway airport. The airport is largely served by network carriers. IAD is also a major connecting hub, especially for international connections as approximately one-third of its prepandemic international passenger volumes were connections. Based on these factors the airport is estimated to have a fairly high proportion of business travelers, also due to its catchment area for the nation’s capital.

Throughout the pandemic, IAD’s traffic recovery lagged behind national averages. The major decline in international travel demand and capacity slowed the airport’s recovery in 2020 and 2021, coupled with an only modest recovery in domestic traffic volumes. A part of this relatively slower recovery than national averages is attributed to the slower progress of recovery in business travel, including government and conference markets.

However, as of 2022, the airport’s international sector experienced a strong uptick in recovery likely related to the ongoing recovery of the international business travel market as well as the airport’s focus on European connectivity, which has recovered faster than Asian air travel markets, especially China.

While the business travel market (in-person conferences, trade shows, and other large meetings) did continue to recover largely in 2022, there remained components of the business travel market—particularly short-haul travel and internal meetings—that were slow to recover.

Key Theme #3: Not All Areas of the Aviation Industry Were Similarly Affected

While global passenger traffic was deeply affected by the impacts of the COVID-19 pandemic, the aviation industry also includes cargo and GA activities that experienced their own unique effects from the pandemic. Chapter 3 provides an overview of the aggregate impacts on cargo tonnage and aircraft operations on the U.S. aviation system. Two case studies—PIT/RFD and VNY—discuss the local impacts of the pandemic on the cargo and GA industries.

Key Theme #4: Localized Pandemic Management Strategies Influenced Impact and Recovery of Aviation Activity

Health policy and regulatory responses to the COVID-19 pandemic saw a significant variation among countries and even within countries themselves. The United States was no exception, with individual states setting their own policies regarding stay-at-home orders, vaccination rollout plans, and travel advisories as public health regulations are generally within the purview of state governments. Across the nation there was a wide range of approaches, with some states adopting stricter measures (e.g., longer stay-at-home orders, limitations on public gatherings, proof-of-vaccination to access businesses or services) while others relaxed measures earlier in the pandemic or never implemented them.

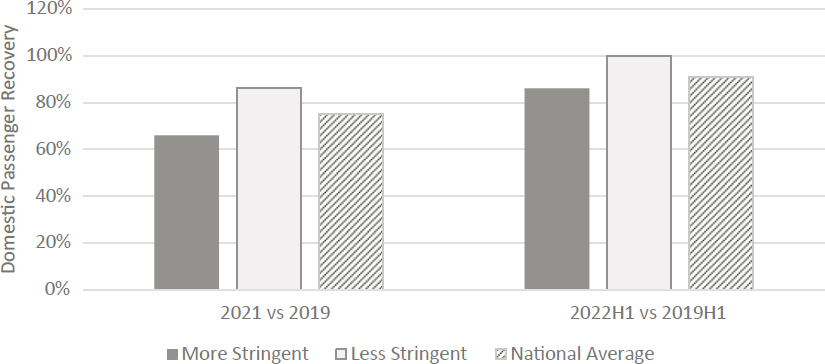

To evaluate the differential impacts of health policy, two sets of states were compared: one group that implemented more stringent restrictions in response to the COVID-19 pandemic and a second group of states with less stringent responses (Figure 15). The “more stringent” group is made up of California, Hawaii, Illinois, New Mexico, New York, Vermont, and Washington, while the “less stringent” group includes Alabama, Florida, Iowa, North Dakota, South Dakota, and Texas (data from Hallas et al. 2021). Analysis of domestic passenger volumes for these two groups reveals that states with fewer restrictions generally recovered traffic faster in 2021 and the first half of 2022 than those states with more stringent public health policies. It should be noted though that the grouping of states is not equally representative in the types of airports and destination markets. States in the more stringent policy response group tended to

Case Study: Cargo Activity at Pittsburgh International Airport (PIT) and Chicago Rockford Airport (RFD)

PIT is a medium hub airport serving the Greater Pittsburgh area with both commercial passenger and cargo services. The airport has developed a cargo market particularly focusing on integrator traffic with UPS and FedEx operations starting in the early 2000s. Like most airports, the COVID-19 pandemic led to a major downturn in passenger activity at the airport, but cargo volumes were maintained throughout 2020 due to growing e-commerce and business-to-business activity. In 2021, PIT annual cargo volumes increased due to expanded UPS operations as well as the planned introduction of Amazon Air. Cargo freighter activity and associated land leasing helped financially offset reductions in passenger-based revenues during the pandemic. The airport evaluated infrastructure plans regarding cargo operations at the airport during the pandemic and designated air cargo as a priority for PIT in planning, focusing on leveraging the airport’s abundant available land for future cargo growth.

Chicago Rockford Airport (RFD) is a nonhub airport located approximately 85 miles northwest of Chicago. The airport has limited passenger services but is UPS’ second largest hub in the United States and is a regional hub for Amazon Air. Both UPS and Amazon Air increased their flight operations and cargo throughput as the demand for air cargo increased during the pandemic, particularly spurred on by the increase in e-commerce demand during 2020. Even though stay-at-home orders were rescinded largely by mid-2020, demand for integrator cargo activity continued to grow at RFD. As of June 2022, cargo volumes remain up more than 25% above prepandemic levels and have consistently been above the national average for cargo volume recovery.

Case Study: General Aviation (GA) at Van Nuys Airport (VNY)

VNY is the nation’s busiest GA airport, located in the San Fernando Valley just north of Los Angeles. In 2019 the airport handled 219,000 aircraft operations and was home to more than 700 based aircraft. Like many GA airports, VNY’s operations are a mix of private operations, noncarrier commercial operations, and business aviation activities.

After initial stay-at-home orders were relaxed in the summer of 2020, VNY experienced a rapid recovery in its aircraft operations—both itinerant and local. Flight schools in the region took advantage of the reduced activity of passenger carriers and the resulting less-active airspace in the busy southern California region, to ramp up training activities. Local aircraft operations at VNY were at times double or triple prepandemic levels in 2020 at a time when passenger carrier activity nationwide was significantly depressed due to the pandemic. There was also a rapid recovery and even growth in business aviation traffic, which was understood to be driven by challenges in the commercial aviation sector regarding capacity and health safety perceptions.

While VNY does not collect landing fees, the rapid recovery in aircraft operations helped produce a quicker recovery in airport revenues through fuel sales as well as supporting local businesses such as fixed-based operators (FBOs) and maintenance businesses. As of 2022 the airport had experienced a 30% increase in annual aircraft operations compared to 2019.

have large hub airports and be more densely populated (e.g., California, New York, and Illinois), whereas the less stringent policy grouping states did not feature large hub airports (e.g., North Dakota, Iowa) or were high leisure destinations (e.g., Florida). While there are a multitude of factors contributing to the recovery of aviation activity at the state level, government policy with respect to health and travel policies was often a contributor to how quickly air travel recovered within a state.

Case Study: State Health Policies on Travel in Hawaii

Daniel K. Inouye International Airport (HNL) serving Honolulu is the largest airport in Hawaii as well as the largest international gateway airport in the state. In addition to domestic and Canadian destinations, HNL had non-stop services to 12 countries in Asia and the Pacific, with Japan being its largest international market. Like all airports, the onset of the pandemic saw a major downturn in demand, but the airport’s international demand recovery was strongly influenced by government policies at home and abroad.

Early in the pandemic, the Government of Hawaii imposed a 14-day quarantine period for visitors (including U.S. residents) and returning residents upon arrival to the state. This policy heavily impacted the tourism industry early in the pandemic, but the introduction of a testing policy—allowing travelers to skip quarantine with a negative test result—starting in October 2020 allowed tourism and travel to resume. All testing and quarantine restrictions for arrivals to the state were not lifted until January 2022.

These health policies have had a notable impact on the recovery of international travel demand and capacity at the airport. As of mid-2022, HNL had recovered less than 30% of its prepandemic international travel demand. This may be attributed both to the travel policies and outbound travel demand and travel policies in HNL’s largest foreign market of Japan. However, with the start of mass vaccinations in 2021 and increased testing capacity, HNL experienced a rapid recovery of its domestic travel market (above 100% of 2019 levels in the winter of 2021/2022) likely spurred by pent-up demand as well as the accessibility of Hawaii as an outdoors domestic destination for U.S. travelers.

Key Theme #5: Financial Recovery Was Aided by Government Support

As the COVID-19 pandemic negatively impacted travel demand and capacity, airports along with the rest of the aviation industry and associated businesses, experienced major downturns in revenues. As previously documented, U.S. airports experienced a significant decline in operating revenues as traffic volumes dropped during the pandemic.

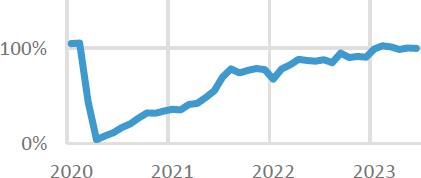

Case Study: Denver International Airport

Denver International Airport (DEN) is a large hub airport serving the metropolitan Denver area and the primary air gateway to the state of Colorado. The airport is a major hub for United Airlines, Southwest Airlines, and ultra low-cost carrier Frontier Airlines.

The airport entered the pandemic in a strong cash position with a number of major infrastructure projects planned and underway that were to revitalize and expand DEN’s terminal facilities. Because of this strong cash position and the presence of federal supports targeting airports and the aviation industry, the airport was able to proactively offer financial support and relief to its airline stakeholders and concessionaires. These airport-level supports and initiatives were part of a strategy to ensure strong stakeholder relations during the challenging times of the pandemic and help position stakeholders to be able to react to the anticipated traffic recovery.

To accomplish this, the airport placed its relief grants into a targeted fund solely for the purposes of debt servicing. This decision allowed the airport to focus its financial activities on supporting local stakeholders (in addition to federal targeted supports such as those directed at airport concessions) and prioritize key capital improvements, such as a major concourse and gate expansion that would be needed as traffic recovered from the impacts of the pandemic.

The U.S. federal government provided a series of financial support packages to the wider economy and specifically to the aviation industry to help provide much-needed financial aid at a time when passenger aviation activity was reduced in part to meet health policy goals. The financial support impacted airports in several ways, including the following.

- Financial aid provided much-needed cash flow to ensure that airports could maintain operations, required maintenance, and debt servicing at a time when revenues were severely depressed due to the downturn in aviation sector activity. This reduced the need to take on other debt through bond issues or other instruments to merely maintain operations. However, many airports did engage in bond refinancing (e.g., OAK, DEN, BHM) as part of a strategy to reduce debt servicing obligations.

- Stipulations on financial aid packages largely required that airport operators could not reduce headcounts to reduce costs. This ensured that airport operators had the necessary staffing levels to provide safe operation of the airport and to provide ongoing financial support to households during a period of industry downturn. Hiring freezes were generally instituted and positions that were voluntarily vacated (e.g., retirement, early retirements, and employees voluntarily changing jobs) were generally not filled back.

- Airline-specific subsidies also required maintaining minimum levels of service early in the pandemic, which provided a base revenue stream for airports. For smaller spoke airports (e.g., BHM or JAC), this was likely more valuable as it ensured levels of service to drive revenues and connectivity for their communities that may have otherwise been threatened if airlines looked to rationalize their networks during the downturn in air travel demand.

- Federal aid programs included requirements targeted to concessionaires, terminal service providers, and ground transportation operators, which helped support associated airport businesses and industries beyond the airport operators themselves. These targeted supports were viewed as important for keeping the airport ecosystem functioning amid a period of unprecedented low demand. Some airports (e.g., DEN and HNL) were able to proactively provide these supports based on strong financial positions entering the pandemic that could be further backstopped through the targeted federal support programs.

Interviews with airports of various sizes and hub types all indicated that the financial support provided by the government was a significant help in maintaining operations and ensuring financial stability during the pandemic. The provision of significant funds for airports, airlines, and associated businesses created stability in the industry in a time of major disruption and was a key source in airports being able to meet the return in demand for air travel as travel picked up in 2021 and 2022. Clauses to ensure that airports could

not reduce headcounts to cut costs were also seen as valuable in ensuring that there were staff available to meet the demands of the traveling public as recovery began.

More cargo-focused airports, such as those in the case studies (PIT and RFD, previously in Key Theme 3) experienced growth in cargo operations, particularly during the early phases of the pandemic. This included increased freighter activity, as cargo capacity previously provided by passenger services was significantly reduced and more business-to-consumer and business-to-business activity moved online. As e-commerce in the United States had been on a growing trend before the pandemic, airports that had an existing base of integrator and e-commerce activity saw increases in activity as the pandemic changed consumption patterns. While lockdown and mobility restrictions were largely lifted in the United States by the end of 2020, e-commerce and integrator air cargo traffic remained strong, enabling growth at airports where they are a focus market for both activity and land use.

Key Theme #6: Airports Implemented Differing Operational and Capital Financial Management Strategies

As the COVID-19 pandemic severely limited air travel demand and capacity in 2020, airports across the United States were forced to develop strategies to adapt to a situation of low revenues while having to remain open and maintain safe operations. While the federal government

Case Study: Birmingham-Shuttlesworth International Airport (BHM)

BHM is a small hub airport and the largest in Alabama, serving the Birmingham Metropolitan Area. The airport is a ‘spoke’ airport with non-stop service primarily to major airline hubs, but also a variety of destinations through low-cost carriers.

In response to the downturn in traffic and revenues from the pandemic, airport staff began an extensive review of all airport contracts and functions resulting in a much leaner and financially streamlined operation. Any capital projects not being funded with federal funds were halted, as was a land acquisition project. Unlike some airports, BHM did not accelerate any planned capital projects as primary planned projects were relating to the terminal, including a passenger lounge project, which were put on hold until traffic levels increased again. Operationally, the airport renegotiated many of its service provider contracts or acquired new service providers and shuttered some of the least profitable concessions at the airport.

Financially, the airport was in a process of restructuring its debt. The airport’s governing authority was able to secure a restructuring program in 2020 which would save $33 million over the lifetime of the bonds. The airport saw operating revenues in FY2020 drop by −15%, with non-aeronautical revenues falling by –20%. This was less than the national average, and generally less severe an impact than was observed at large and medium hub airports. By FY2022, total operating revenues still remained down by −7% compared to FY2019. However, the airport reduced its operating expenses by −24% and significantly reduced its total indebtedness highlighting the success of cost-cutting and efficiency measures undertaken during the pandemic.

provided substantial funding in the form of grants to airports and airlines, in the earliest phase of the pandemic airports were faced with developing strategies to mitigate the major reduction in revenues.

Across the nation, several strategies evolved toward reducing operating and capital costs borne by airports at a time of significantly reduced revenues. Based on interviews with airports and observations of industry data, the following major strategies were observed:

- Closures of concourses and terminals to reduce operating costs. With declines in passenger traffic, particularly international traffic, many airports would close portions of passenger terminals, ranging from a few gates to entire terminals or concourses. Temporary closure of facilities reduced operating and maintenance costs ranging from utilities to janitorial services. When demand began to rise, airports were able to recommission these facilities, often in a staged fashion to meet demand. OAK and HNL both closed entire concourses/terminals. While the former did so to reduce operating costs, the latter closed terminals that were no longer in use due to restrictions on international travel.

- Many airports deferred or delayed capital improvements to trim costs. Airports interviewed for this research indicated that they conducted reviews of existing capital plans to determine which projects could be deferred to a later date, which were necessary (e.g., safety improvements, utility upgrades), and which should be continued as the cost of deferral was deemed to be too high.

- Some airports accelerated infrastructure development plans, particularly those focusing on airside (runway, taxiway, apron) and terminal facilities to take advantage of reduced operations and passenger activity. With fewer operations, airside and terminal construction was less disruptive to airport activities, and schedules for projects were brought up to reduce the cost of disruptions if projects were carried out during periods of normal activity levels. DEN maintained pace on a major concourse and gate expansion project during 2020 as airline stakeholders encouraged the airport to continue with construction to prevent capacity constraints from hindering the recovery of traffic once demand regrew to near prepandemic levels.

- Airport concessionaires asked for, and in many cases received, waivers and relief for contracted Minimum Annual Guarantees. With passenger-based revenue sources being so majorly impacted, concessionaires were often more negatively impacted than the airport operators themselves. Airports that had entered the pandemic in good financial positions with large cash reserves were mostly able to provide support to concessionaires and other service providers before federal grant programs targeting those sectors (CRRSA) were implemented.

- Parking and ground transportation services, such as shuttle buses and valet parking, were reduced or suspended. Many airports closed their long-term parking lots and kept open only the lots or parking garages closest to the terminal during times of major traffic reductions. OAK, DEN, and BHM all engaged in these closures based on the case study research. This was often accompanied by strategies to flatten parking rate structures (e.g., high-value parking garages adjacent to terminals could be used at low-value, long-term parking lot rates as seen at DEN) to improve passenger experience despite missing out on potential revenues. Some airports repurposed temporarily closed parking lots for functions such as COVID-19 testing and vaccination sites or community amenities like temporary drive-in movie theaters.