Pathways to Reduce Child Poverty: Impacts of Federal Tax Credits (2026)

Chapter: 2 Key Provisions of the EITC and CTC Including Changes Under the TCJA and ARPA

2

Key Provisions of the EITC and CTC Including Changes Under the TCJA and ARPA

The committee was charged with assessing the impact of the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) on child poverty in 2021. The committee was also charged with assessing what changes to the provisions of the EITC and CTC, if implemented, would further reduce child poverty. To provide background for these analyses, this chapter summarizes the rules and eligibility criteria of these two credits under two different time periods: 2018, which includes changes to the CTC under the Tax Cuts and Jobs Act (TCJA) of 2017,1 and 2021, when these two credits were temporarily changed under the American Rescue Plan Act (ARPA).2

In contrast to other “safety net” policies, the EITC and CTC are administered by the Internal Revenue Service (IRS), rather than through other government or state agencies. Over the past few decades, the IRS has increasingly become one of the key federal agencies delivering cash assistance to low-income households (Holt, 2016). Key features of the administration

___________________

1Note that a tax year (TY) is generally the same as a calendar year. So, TY 2018 describes the tax law provisions in effect from January through December of 2018. However, benefits accrued during a tax year are generally not received until the subsequent year when a tax return is filed. For example, a TY 2018 return is generally filed in the first quarter of 2019, so a TY 2018 EITC benefit is received in 2019.

2In contrast to the EITC, the CTC provisions in the 2017 TCJA legislation were temporary and set to expire. However, P.L. 119-21 made the temporary TCJA changes to the CTC permanent, while modifying several of them. Notably, the law permanently increased the maximum credit per child to $2,200 beginning in 2025 and indexed it to inflation starting in 2026 and now requires that tax filers who claim the CTC have a Social Security Number (SSN; among married joint filers, at least one spouse must have an SSN).

of these tax credits include that households must generally file a federal income tax return to receive tax benefits, eligibility for tax benefits is based on the prior year’s income and family structure (e.g., number of children and marital/filing status), and tax benefits are received as a lump sum as part of an annual tax refund. Chapters 4 and 5 expand upon the role of the IRS in administering the EITC and CTC and consequences for households’ access to these credits. Chapter 4 also describes the number of tax returns claiming the EITC and CTC in TY 2021, as well as the total amount of each credit claimed.

Main messages from this chapter are highlighted in Box 2-1.

THE EARNED INCOME TAX CREDIT

Overview

When first enacted on a temporary basis in 1975, the EITC was a modest tax credit that provided financial assistance exclusively to low-income working families with children. Various legislative changes over the past 50 years have increased and expanded this credit, and it is now one of the

BOX 2-1

Chapter 2 Main Messages

- The 2021 American Rescue Plan Act (ARPA) expanded the Child Tax Credit (CTC) by making it fully refundable, increasing the maximum credit amount (up to $3,600 per child under 6 and $3,000 for children ages 6 to 17), and raising the age limit for eligible children from 16 to 17. It also introduced advance monthly payments. These changes substantially increased support for low-income families with children compared to the credit under the Tax Cuts and Jobs Act (TCJA). The ARPA provisions expired at the end of 2021, and the CTC reverted to the parameters of the TCJA.

- ARPA made limited changes to the Earned Income Tax Credit (EITC). The most notable change was a temporary increase in benefits for childless workers, while benefits for families with children remained essentially unchanged. The benefit increases for childless adults lapsed after 2021 and reverted to its prior-law levels.

- Both credits include Social Security number (SSN) requirements, though the CTC is somewhat more inclusive, allowing noncitizen tax filers with Individual Taxpayer Identification Numbers to claim the credit if their children have SSNs. These requirements were not changed in 2021 under ARPA. Note that these SSNs must generally be associated with work authorization, sometimes referred to as work-authorized SSNs or employment SSNs.

- Almost all of the other provisions of the EITC and CTC policies in 2021 reverted to those in the U.S. tax code (EITC) and/or those enacted under the TCJA (CTC).

federal government’s largest antipoverty programs providing cash assistance to low-income working families—primarily, but no longer exclusively, to working families with children. The EITC is a refundable tax credit, which means that the benefit is not limited by a recipient’s income tax liability. For example, if an individual were initially eligible for a $500 nonrefundable credit, but they owed $100 in income taxes, they could only receive a $100 credit, effectively forfeiting the remainder. If the credits were refundable, they could receive the entire $500 amount.

Since the EITC is a tax provision under Section 32 of the Internal Revenue code and thus administered by the IRS, recipients must file a federal income tax return to receive the credit. In addition, the EITC is subject to a variety of eligibility requirements described below. In the sections that follow, the eligibility requirements and benefits of the EITC in effect in TY 2018 and TY 2021 are described. (See Box 1-2 in Chapter 1 for the terms used to characterize the various configurations of EITC and CTC policies described in this chapter.) As described in more detail below, the latter changes, referred to as the “ARPA EITC Expansion,” temporarily increased the childless EITC for eligible workers, which had limited impact on families with children—the primary focus of this report.3 For more detailed descriptions of the EITC and its provisions, see Congressional Research Service (2022a,b, 2023). IRS statistics on total number of tax returns with the EITC and total credit amounts in TYs 2018 and 2021 are also presented below.

Design of the EITC

As noted above, the EITC is designed to aid low-income working families, especially those with children. Since the EITC is a refundable credit, it is not limited by what a household owes in income taxes. Any amount greater than what is owed in income taxes is received as part of the household’s annual tax refund. Since many low-income families owe little to nothing in income tax due to the structure of the federal income tax (e.g., the standard deduction), they can benefit from refundable tax credits like the EITC.

The credit amount is determined by a formula that varies based on tax filers’ earned income (and adjusted gross income [AGI] in some cases), with these formulas depending on tax filing status and number of qualifying children. Below, EITC eligibility requirements and the schedules of benefits that eligible tax filers may receive are described. Because the EITC is indexed

___________________

3Unlike it did for the CTC, the TCJA did not make any changes specifically to the EITC. However, it did change how the inflation adjustments for numerous tax provisions were calculated, including for the EITC.

for inflation, the income limits and maximum credit amounts are adjusted annually to reflect changes in the cost of living. In the sections that follow, the dollar values used for these amounts are based on the provisions of the EITC in TY 2018.

Eligibility Requirements

This section reviews the eligibility requirements for the EITC, including those related to income, qualifying children, and SSNs.

To be eligible to receive the EITC, a tax filing unit must have earned income, meaning the tax filer, or one member of a married couple who files a joint tax return, must have earnings in the form of wages, salary, tips, or self-employment income4 during the tax year. In some cases in which the AGI is greater than earnings, AGI may also affect the credit calculation. Certain types of investment income can also limit credit eligibility.5

Tax filers without EITC-qualifying children—often simply referred to as “childless” filers—may receive an EITC benefit if they are between the ages of 25 and 64.6 However, the EITC provides more generous benefits for eligible tax filers who have EITC-eligible children.

Credit-qualifying children must meet certain relationship, age, and residency requirements. To meet the relationship test, a “qualifying child” must be a son, daughter, stepchild, foster child, or a grandchild, sibling, half or step sibling, niece, or nephew. To meet the age test, qualifying children must be under the age of 19 by the end of the tax year or under the age of 24 if they are students, with the age limit waived if the child is permanently and totally disabled.

To meet the residency test, a qualifying child must have lived with the tax filer for more than half of the tax year in the United States.7 Only one taxpayer can claim a child for the EITC in a given tax year. In cases where more than one taxpayer may be able to claim a child for the EITC (e.g., multigenerational households) tie-breaker rules may apply.

Finally, to claim the EITC, tax filers, their spouses (if applicable), and all of their qualifying children must have “work-authorized” SSNs, sometimes

___________________

4See Congressional Research Service (2023) for precise definitions of what is counted as earned income.

5Investment income is defined as interest income (including tax-exempt interest), dividends, net rental income, net capital gains, and net passive income. See Congressional Research Service (2023) for details.

6Among married childless couples, one spouse must be in this age range for the household to qualify.

7There are exceptions to residency requirements in the case of separated parents who file their tax returns separately. In addition, if parents file separate returns, a child can be claimed by only one parent (the parent claiming the child as a dependent).

referred to as employment SSNs.8 The vast majority of SSNs, including those issued to noncitizens, are associated with work authorization. Thus, for simplicity, the rest of this chapter simply refers to them as SSNs.

Benefit Schedules

The benefits under the EITC vary by earned income, filing status, and number of qualifying children. The benefit schedule that prevailed in TY 2018 is summarized in Figure 2-1. There are three relevant tax filing statuses for the EITC: unmarried tax filers that have no children (single), unmarried filers that are heads of households (HoH) and have dependent children, and married couples that file jointly (MFJ). In most cases, taxpayers who file their returns as married filing separately are not eligible for the EITC. As shown in Figure 2-1, the benefit schedules under the EITC differ by filing status, with single and HoH filers (i.e., unmarried tax filers) experiencing credit phase-out at lower income levels than married joint filers with the same number of EITC-qualifying children.

Since the EITC is a refundable tax credit, individuals or married couples filing tax returns need not owe income taxes to receive a benefit. Thus, individuals with incomes below the minimum level subject to taxes (i.e., less than the standard deduction) can receive the credit. For those who do owe income taxes, the credit will first offset those taxes with any additional amount included as part of their tax refund. Thus, in Figure 2-1, single, HoH, and MFJ filers in TY 2018 with incomes below the standard deductions of $12,000, $18,000, and $24,000, respectively, received the EITC even though they owed no income taxes when they filed their tax returns for that year.

As shown in Figure 2-1, over the phase-in region of the credit, the EITC increases with earned income until it reaches the maximum credit amount.9 The benefit then remains at its maximum level over the “plateau” region, as earned income increases, and then gradually declines over the “phaseout” region, until earned income (or AGI, if greater) increases to the point at which filers are no longer eligible to receive a benefit.10 As indicated in Figure 2-1, EITC benefits vary by type of tax filer (i.e., single, HoH, or MFJ). MFJ filers are eligible for benefits at higher income levels compared

___________________

8For more information on work-authorized SSNs, see Social Security Administration (2024); Lunder and Crandall-Hollick (2016).

9Generally, an EITC-eligible tax filer with a qualifying child will file their income tax return as a HoH, but there may be cases in which they file as single. The HoH and single-filer EITC benefit schedules/formulas are the same.

10While the EITC phases in based on a tax filer’s earned income, it phases out as a function of the filer’s earned income or adjusted gross income, whichever is greater. See Congressional Research Service (2023) for details.

NOTES: While the Earned Tax Income Credit (EITC) phases in based on a tax filer’s earned income, it phases out based on the tax filer’s earned income or Adjusted Gross Income, whichever is greater. ARPA = American Rescue Plan Act of 2021.

to single/HoH filers, and benefits are higher for filers with more children, up to three or more credit-qualifying children.

Table 2-1 illustrates another way to characterize EITC, as well as CTC, benefits. This table shows the EITC benefits excluding changes under ARPA [non-ARPA EITC in columns (3)]; CTC benefits under TCJA [CTC TCJA in columns (1)]; and the combination of these two tax credits [TCJA CTC + EITC excl. ARPA in columns (5)]. This set of benefits is calculated for TY 2018. In addition, the table includes benefits for the policies in place in 2021 for the EITC [EITC Policy in 2021 in columns (4)]; the CTC [CTC Policy in 2021 in columns (2)]; and in combination [Combined EITC & CTC Policies in 2021 in columns (6)]. These benefits are tabulated for various household types and for a number of different levels of annual income displayed in the table.11

___________________

11The annual income levels included are multiples of thresholds for poverty used in the Supplemental Poverty Measure (SPM; see Chapter 3) constructed by the Bureau of Labor Statistics for a household consisting of two adults and two children in 2018. Also note that all of the calculations presented in this table assume that all of the annual incomes are made up entirely of wage earnings.

TABLE 2-1 Benefits for EITC and CTC in TY 2018 Under TCJA and Permanent Tax Law EITC and CTC Policies in 2021 Under ARPA for TY 2021 by Different Types of Households, Number of Children, and Annual Incomea,b

| CTC | EITCc | CTC + EITC | CTC | EITC | CTC + EITC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (1) | (2) | (3) | (4) | (5) | (6) | |

| Annual Income or Earningsd | $14,000 | $28,000 | ||||||||||

| Single or Head of Household (HoH) | ||||||||||||

Childless | $0 | $0 | $100 | $1,136 | $100 | $1,136 | $0 | $0 | $0 | $0 | $0 | $0 |

% of Annual Income | 0.0% | 0.0% | 0.7% | 8.1% | 0.7% | 8.1% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

1 child, ages 0–5 | $1,400 | $3,600 | $3,468 | $3,618 | $4,868 | $7,218 | $2,000 | $3,600 | $1,982 | $2,263 | $3,982 | $5,863 |

% of Annual Income | 10.0% | 25.7% | 24.8% | 25.8% | 34.8% | 51.6% | 7.1% | 12.9% | 7.1% | 8.1% | 14.2% | 20.9% |

1 child, ages 6–17 | $1,400 | $3,000 | $3,468 | $3,618 | $4,868 | $6,618 | $2,000 | $3,000 | $1,982 | $2,263 | $3,982 | $5,263 |

% of Annual Income | 10.0% | 21.4% | 24.8% | 25.8% | 34.8% | 47.3% | 7.1% | 10.7% | 7.1% | 8.1% | 14.2% | 18.8% |

2 children, ages 0–5 & 6–17 | $1,725 | $6,600 | $5,600 | $5,600 | $7,325 | $12,200 | $3,800 | $6,600 | $3,769 | $4,194 | $7,569 | $10,794 |

% of Annual Income | 12.3% | 47.1% | 40.0% | 40.0% | 52.3% | 87.1% | 13.6% | 23.6% | 13.5% | 15.0% | 27.0% | 38.6% |

3 children, 2 ages 0–5 & 1 ages 6–17 | $1,725 | $10,200 | $6,300 | $6,300 | $8,025 | $16,500 | $4,825 | $10,200 | $4,485 | $4,942 | $9,310 | $15,142 |

% of Annual Income | 12.3% | 72.9% | 45.0% | 45.0% | 57.3% | 117.9% | 17.2% | 36.4% | 16.0% | 17.7% | 33.3% | 54.1% |

| CTC | EITCc | CTC + EITC | CTC | EITC | CTC + EITC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (1) | (2) | (3) | (4) | (5) | (6) | |

| Married (MFJ) | ||||||||||||

Childless | $0 | $0 | $520 | $1,502 | $520 | $1,502 | $0 | $0 | $0 | $0 | $0 | $0 |

% of Annual Income | 0.0% | 0.0% | 3.7% | 10.7% | 3.7% | 10.7% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

1 child, ages 0–5 | $1,400 | $3,600 | $3,468 | $3,618 | $4,868 | $7,218 | $1,800 | $3,600 | $2,893 | $3,214 | $4,693 | $6,814 |

% of Annual Income | 10.0% | 25.7% | 24.8% | 25.8% | 34.8% | 51.6% | 6.4% | 12.9% | 10.3% | 11.5% | 16.8% | 24.3% |

1 child, ages 6–17 | $1,400 | $3,000 | $3,468 | $3,618 | $4,868 | $6,618 | $1,800 | $3,000 | $2,893 | $3,214 | $4,693 | $6,214 |

% of Annual Income | 10.0% | 21.4% | 24.8% | 25.8% | 34.8% | 47.3% | 6.4% | 10.7% | 10.3% | 11.5% | 16.8% | 22.2% |

2 children, ages 0–5 & 6–17 | $1,725 | $6,600 | $5,600 | $5,600 | $7,325 | $12,200 | $3,200 | $6,600 | $4,970 | $5,447 | $8,170 | $12,047 |

% of Annual Income | 12.3% | 47.1% | 40.0% | 40.0% | 52.3% | 87.1% | 11.4% | 23.6% | 17.7% | 19.5% | 29.2% | 43.0% |

3 children, 2 ages 0–5 & 1 ages 6–17 | $1,725 | $10,200 | $6,300 | $6,300 | $8,025 | $16,500 | $4,225 | $10,200 | $5,686 | $6,195 | $9,911 | $16,395 |

% of Annual Income | 12.3% | 72.9% | 45.0% | 45.0% | 57.3% | 117.9% | 15.1% | 36.4% | 20.3% | 22.1% | 35.4% | 58.6% |

| CTC | EITCc | CTC + EITC | CTC | EITC | CTC + EITC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (1) | (2) | (3) | (4) | (5) | (6) | |

| Annual Income or Earningsd | $42,000 | $56,000 | ||||||||||

| Single or Head of Household (HoH) | ||||||||||||

Childless | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

% of Annual Income | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

1 child, age 0–5 | $2,000 | $3,600 | $0 | $26 | $2,000 | $3,626 | $2,000 | $3,600 | $0 | $0 | $2,000 | $3,600 |

% of Annual Income | 4.8% | 8.6% | 0.0% | 0.1% | 4.8% | 8.6% | 3.6% | 6.4% | 0.0% | 0.0% | 3.6% | 6.4% |

1 child, age 6–17 | $2,000 | $3,000 | $0 | $26 | $2,000 | $3,026 | $2,000 | $3,000 | $0 | $0 | $2,000 | $3,000 |

% of Annual Income | 4.8% | 7.1% | 0.0% | 0.1% | 4.8% | 7.2% | 3.6% | 5.4% | 0.0% | 0.0% | 3.6% | 5.4% |

2 children, ages 0–5 & 6–17 | $3,800 | $6,600 | $821 | $1,246 | $4,621 | $7,846 | $4,000 | $6,600 | $0 | $0 | $4,000 | $6,600 |

% of Annual Income | 9.0% | 15.7% | 2.0% | 3.0% | 11.0% | 18.7% | 7.1% | 11.8% | 0.0% | 0.0% | 7.1% | 11.8% |

3 children, 2 ages 0–5 & 1 age 6–17 | $4,825 | $10,200 | $1,537 | $1,994 | $6,362 | $12,194 | $6,000 | $10,200 | $0 | $0 | $6,000 | $10,200 |

% of Annual Income | 11.5% | 24.3% | 3.7% | 4.7% | 15.1% | 29.0% | 10.7% | 18.2% | 0.0% | 0.0% | 10.7% | 18.2% |

| CTC | EITCc | CTC + EITC | CTC | EITC | CTC + EITC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (1) | (2) | (3) | (4) | (5) | (6) | |

| Married (MFJ) | ||||||||||||

Childless | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

% of Annual Income | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

1 child, age 0–5 | $1,800 | $3,600 | $656 | $977 | $2,456 | $4,577 | $2,000 | $3,600 | $0 | $0 | $2,000 | $3,600 |

% of Annual Income | 4.8% | 8.6% | 1.6% | 2.3% | 6.3% | 10.9% | 3.6% | 6.4% | 0.0% | 0.0% | 3.6% | 6.4% |

1 child, age 6–17 | $1,800 | $3,000 | $656 | $977 | $2,456 | $3,977 | $2,000 | $3,000 | $0 | $0 | $2,000 | $3,000 |

% of Annual Income | 4.8% | 7.1% | 1.6% | 2.3% | 6.3% | 9.5% | 3.6% | 5.4% | 0.0% | 0.0% | 3.6% | 5.4% |

2 children, ages 0–5 & 6–17 | $3,200 | $6,600 | $2,021 | $2,499 | $5,221 | $9,099 | $4,000 | $6,600 | $0 | $0 | $4,000 | $6,600 |

% of Annual Income | 9.5% | 15.7% | 4.8% | 5.9% | 14.3% | 21.7% | 7.1% | 11.8% | 0.0% | 0.0% | 7.1% | 11.8% |

3 children, 2 ages 0–5 & 1 age 6–17 | $4,225 | $6,800 | $2,737 | $3,247 | $6,962 | $10,047 | $6,000 | $10,200 | $0 | $298 | $6,000 | $10,498 |

% of Annual Income | 14.3% | 18.1% | 6.5% | 7.7% | 20.8% | 25.8% | 10.7% | 18.2% | 0.0% | 0.5% | 10.7% | 18.7% |

| CTC | EITCc | CTC + EITC | CTC | EITC | CTC + EITC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (1) | (2) | (3) | (4) | (5) | (6) | |

| Annual Income or Earningsd | $112,000 | $280,000 | ||||||||||

| Single or Head of Household (HoH) | ||||||||||||

Childless | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

% of Annual Income | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

1 child, age 0–5 | $2,000 | $3,600 | $0 | $0 | $2,000 | $3,600 | $2,000 | $3,600 | $0 | $0 | $2,000 | $3,600 |

% of Annual Income | 1.8% | 3.2% | 0.0% | 0.0% | 1.8% | 3.2% | 0.7% | 1.3% | 0.0% | 0.0% | 0.7% | 1.3% |

1 child, age 6–17 | $2,000 | $3,000 | $0 | $0 | $2,000 | $3,000 | $2,000 | $3,000 | $0 | $0 | $2,000 | $3,000 |

% of Annual Income | 1.8% | 2.7% | 0.0% | 0.0% | 1.8% | 2.7% | 0.7% | 1.1% | 0.0% | 0.0% | 0.7% | 1.1% |

2 children, ages 0–5 & 6–17 | $4,000 | $6,600 | $0 | $0 | $4,000 | $6,600 | $4,000 | $6,600 | $0 | $0 | $4,000 | $6,600 |

% of Annual Income | 3.6% | 5.9% | 0.0% | 0.0% | 3.6% | 5.9% | 1.4% | 2.4% | 0.0% | 0.0% | 1.4% | 2.4% |

3 children, 2 ages 0–5 & 1 age 6–17 | $6,000 | $10,200 | $0 | $0 | $6,000 | $10,200 | $6,000 | $9,600 | $0 | $0 | $6,000 | $9,600 |

% of Annual Income | 5.4% | 9.1% | 0.0% | 0.0% | 5.4% | 9.1% | 2.1% | 3.4% | 0.0% | 0.0% | 2.1% | 3.4% |

| CTC | EITCc | CTC + EITC | CTC | EITC | CTC + EITC | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | TCJA | Policy in 2021 | non-ARPA | Policy in 2021 | TCJA CTC + EITC excl. ARPA | Combined EITC & CTC Policies in 2021 | |

| (1) | (2) | (3) | (4) | (5) | (6) | (1) | (2) | (3) | (4) | (5) | (6) | |

| Married (MFJ) | ||||||||||||

Childless | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

% of Annual Income | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

1 child, age 0–5 | $2,000 | $3,600 | $0 | $0 | $2,000 | $3,600 | $2,000 | $3,600 | $0 | $0 | $2,000 | $3,600 |

% of Annual Income | 1.8% | 3.2% | 0.0% | 0.0% | 1.8% | 3.2% | 0.9% | 0.9% | 0.0% | 0.0% | 0.9% | 0.9% |

1 child, age 6–17 | $2,000 | $3,000 | $0 | $0 | $2,000 | $3,000 | $2,000 | $3,000 | $0 | $0 | $2,000 | $3,000 |

% of Annual Income | 1.8% | 2.7% | 0.0% | 0.0% | 1.8% | 2.7% | 0.9% | 0.9% | 0.0% | 0.0% | 0.9% | 0.9% |

2 children, ages 0–5 & 6–17 | $4,000 | $6,600 | $0 | $0 | $4,000 | $6,600 | $4,000 | $6,600 | $0 | $0 | $4,000 | $6,600 |

% of Annual Income | 3.6% | 5.9% | 0.0% | 0.0% | 3.6% | 5.9% | 1.8% | 1.8% | 0.0% | 0.0% | 1.8% | 1.8% |

3 children, 2 ages 0–5 & 1 age 6–17 | $6,000 | $10,200 | $0 | $0 | $6,000 | $10,200 | $6,000 | $10,200 | $0 | $0 | $6,000 | $10,200 |

% of Annual Income | 5.4% | 9.1% | 0.0% | 0.0% | 5.4% | 9.1% | 2.7% | 2.7% | 0.0% | 0.0% | 2.7% | 2.7% |

a The EITC excluding ARPA and the CTC and EITC receipt amounts assume that all household members have SSNs.

b Definitions of column headings are found in Box 1-2 in Chapter 1.

c Note that because of the annual indexing of EITC benefits for inflation, some of the benefit amounts change from 2018 to 2021. The exception is the increase in EITC benefits for childless households in 2021, which, as noted in the text, were a provision of ARPA.

d Annual incomes are based on multiples of the 2018 SPM threshold for a household consisting of two adults and two children and who are renters, which was $28,166 (see Table A-3 in Fox, 2019). The committee approximated the 2018 SPM threshold to be $28,000 and used $14,000 for 50% of 2018 SPM poverty threshold; $42,000 for 150% SPM poverty threshold; $56,000 for 200% SPM poverty threshold; $112,000 for 400% SPM poverty threshold; and $280,000 for 1,000% SPM poverty threshold. Also note that all of the calculations presented in this table assume that all of the annual incomes are made up entirely of wage earnings or earned income.

As evident from Table 2-1, households filing as single and HoH with very low earnings (see columns under annual income of $14,000) received EITC benefits that excluded ARPA ranging from $100 to $6,300 in TY 2018 (see columns [3]). Benefits increased with the number of children claimed and ranged from 0.7% to 45% of earned income. Among households that filed as MFJ, benefits ranged from $520 to $6,300. For households with earned income of $28,000, the benefits for childless households declined to zero, while the credit amounts and the percentage of income for households with children declined relative to corresponding households with earned income of $14,000. Households with incomes of $56,000 or higher were not eligible to receive any EITC in TY 2018. In summary, the benefits of the EITC are designed to be concentrated among very to relatively low-income households, with EITC benefits to very low-income households modestly increasing their financial resources.

The benefit schedules in Figures 2-1 and 2-2 for the EITC excluding changes under ARPA and the illustrations of these benefits in Table 2-1 are only available among tax filers who satisfy the residency and SSN requirements of the credit. In practice, this means that households in which all members are either U.S. citizens or noncitizen U.S. residents allowed to work in the United States (or some combination) are eligible for the credit. But households that include family members who are not allowed to work in the United States (and hence do not have an SSN associated with employment) or family members that are not U.S. residents would generally not be eligible. Hence, mixed-status families generally cannot receive this benefit. As explained in more detail in Chapters 8 and 9, these requirements have consequences for reducing child poverty among households that include certain noncitizens.

IRS Statistics

The total number of returns and total amount of benefits distributed under the provisions of the EITC that prevailed in TY 2018 are displayed in Table 2-2. Based on IRS statistics, 26.49 million tax returns claimed the EITC, including both childless tax filers and filers with children, for a total of $72.96 billion in 2021 dollars.

ARPA Reforms and EITC in 2021

Benefit Schedules

As part of ARPA, the EITC for workers without qualifying children—the childless EITC—underwent a large, temporary expansion for TY 2021. As displayed in Figure 2-2, the maximum childless EITC in TY 2018 would

TABLE 2-2 EITC and CTC Numbers of Returns and Credit Amounts for Tax Years 2018 and 2021

| 2018 | 2021 | |

|---|---|---|

| Earned Income Tax Credit (EITC)a | ||

| Number of returns (millions) | 26.49 | 32.22 |

| Amount (billions) | $72.96 | $65.68 |

| Child Tax Credit (CTC) | ||

| Nonrefundable CTC (& Other Dependent Tax Credit) | ||

| Number of returns (millions) | 39.38 | |

| Amount (billions) | $91.59 | |

| Refundable Portion of CTC (i.e., Additional Child Tax Credit) | ||

| Number of returns (millions) | 20.45 | 37.77 |

| Amount (billions) | $40.72 | $115.87 |

| Advance Payment | ||

| Number of returns (millions) | 37.96 | |

| Amount (billions) | $93.62 | |

| Total Amount (billions) | $132.31 | $209.49 |

NOTES: Numbers of returns in millions. Amounts in billions of 2021 dollars. The Consumer Price Index for All Urban Consumers was used for inflation adjustment.

a EITC total returns and amounts include those for both childless tax filers and those with children.

SOURCE: Internal Revenue Service (2025). Advance CTC totals obtained from Internal Revenue Service table “Table 1. Advance Child Tax Credit Payments” https://www.irs.gov/statistics/soi-tax-stats-advance-child-tax-credit-payments-in-2021

have been $502 for MFJ tax filers. This amount increased under ARPA by $982, to a total combined credit of $1,502 in TY 2021. (The same change in the maximum EITC credit occurred for single filers and HoH tax filers.) However, in 2021 the EITC schedules for tax filers that claimed one or more children remained unchanged, except for indexing credit amounts annually for inflation. Table 2-1 illustrates this change for childless single, HoH, and MFJ filers; compare columns (3) and (4) for the rows labeled “Childless.” Note that while there was no expansion of EITC benefits for households with children, the dollar amounts of benefits for columns (3) and (4) differ slightly due to the cost-of-living adjustments for TY 2018 versus TY 2021.

Several other temporary changes to the childless EITC were also enacted under ARPA. For example, the childless EITC was originally only available to tax filers between the ages of 25 and 65. In 2021, the minimum age was reduced to 19 for most workers and the upper age limit was eliminated. These reforms expired at the end of 2021.

In addition to the changes to the childless EITC, ARPA also included a temporary income “lookback” provision for all EITC filers, whereby 2021 filers could claim a higher EITC in that year if their earned income from TY 2019 (prior to the COVID-19 pandemic) would have enabled them to receive a higher credit on their TY 2021 return. This extended a similar lookback provision introduced in TY 2020 after the onset of the pandemic. Finally, the investment income threshold for all filers was permanently increased to $10,000 in TY 2021 and indexed to inflation for future years. (See Congressional Research Service [2022a] for more details on these provisions.)

IRS Statistics

Based on IRS data, 32.22 million tax returns claimed the EITC in TY 2021, which temporarily included a higher maximum credit for childless tax filers, and had total claims of $65.68 billion (see Table 2-2). Compared to EITC claims in TY 2018 (26.49 million), the larger number of returns claiming the EITC in TY 2021 under the ARPA changes (32.22 million) presumably reflects, in part, an increased number of childless tax filers who claimed the more generous EITC. However, despite the larger number of tax returns claiming the EITC in TY 2021, the total amount of the EITC credits distributed by the IRS in that year was lower than the amount distributed in TY 2018 ($65.68 million vs. $72.96 million). The latter finding likely reflects, in part, the decline in employment in 2021 due to the COVID-19 pandemic.

THE CHILD TAX CREDIT

Overview

The CTC, enacted in 1997, is a tax credit to families with dependent children that reduces tax filers’ federal income tax liability by up to $2,000 per child. Low-income households may receive the benefit in the form of a refundable component (Congressional Research Service, 2021, 2025). The TCJA of 2017 made significant temporary changes to the CTC that were originally scheduled to be in effect from TY 2018 through TY 2025. These changes were meant to, in part, offset the temporary elimination

of the personal exemption for dependents from the U.S. tax code.12 (The personal exemption allows taxpayers to deduct a fixed amount—$4,050 in TY 2017—for themselves, their spouses [if married], and each of their dependents.) The sections that follow describe the eligibility requirements and benefit schedules for the CTC under TCJA, as well as the temporary ARPA CTC Expansion in TY 2021. (See Box 1-2 in Chapter 1 for the terms used to characterize the various configurations of CTC policies described below.) IRS statistics on total numbers of tax returns and amounts of CTC credits received also are provided for TYs 2018 and 2021.

The CTC Under TCJA

Under the provisions of TCJA, families with dependent children under 17 years who filed a tax return could receive the CTC and reduce their tax liability by up to $2,000 per child. Low-income families with little to no tax liability could receive the refundable portion of the credit based on their earnings. As with the EITC, benefits varied by income, tax filing status, and number of qualifying children, although there are important differences between the two credits. The sections that follow discuss eligibility requirements, benefits schedules, and IRS statistics.

Under TCJA, taxpayers with dependents who did not qualify for the CTC (including older children, children without SSNs, and adult dependents) were eligible for a $500 nonrefundable credit for each of these dependents. This credit, sometimes referred to as the other dependent tax credit (ODTC), is combined with any CTC and phased out according to the same rules.13 Most CTC provisions are not annually adjusted for inflation.14 However, under the TCJA, the maximum refundable portion of the credit is inflation indexed.

Eligibility Requirements

While the eligibility requirements for the CTC are similar to those of the EITC, there are some important differences. First, for low-income taxpayers who receive the refundable portion of the credit, their credit begins to phase in when earnings exceed $2,500, while the EITC phases in with the first dollar of earnings. The EITC benefit phases in faster, and the maximum benefit is larger for families with more children, up to three or

___________________

12As noted in footnote 2, the provisions of the TCJA were set to expire at the end of 2025, but in 2025, P.L. 119-21 made them permanent provisions of the U.S. tax law.

13https://povertycenter.columbia.edu/sites/povertycenter.columbia.edu/files/content/Publications/Credit-for-Other-Dependents-A-Policy-Explainer-CPSP-2025.pdf

14The $500 ODTC amount is not annually adjusted for inflation.

more children. In contrast, while there is no cap on how many children can be claimed for the CTC, the refundable portion of the credit phases in at a fixed rate irrespective of the number of children a family has. This means low-income families with more children tend not to receive additional benefit for each child (see Maag et al., 2023). The CTC is also available to households with much higher incomes. In addition, higher-income households with little or no earned income, but with sufficient income tax liability from other income sources, can still benefit from the credit but would not be eligible for the EITC. Finally, the EITC is disallowed for households with high levels of certain investment income, while no such limitation is in effect for the CTC.

In addition, the eligibility rules for children claimed for the CTC and EITC differ, meaning in some cases a child can be claimed for one credit but not the other. Common to both credits, the child generally must have a biological or legal relationship to the taxpayer claiming them; and the child must be either citizen, national, or a resident of the United States. Aside from these commonalities, there are numerous differences.

First, the CTC is only available for dependent children under 17 years old, while the EITC is available for dependent children under 19 years old (or under 24 years old if a full-time student, with no age limit if the child is permanently and totally disabled). Second, while both credits require the child to live with the taxpayer who is claiming them for more than half the year, for the EITC, the taxpayer and child must generally live together for more than half the year in the United States. In addition, the CTC allows the residency test to be waived in certain cases and subject to certain reporting requirements (IRS Form 8332), allowing some noncustodial parents to claim the credit. No such flexibility is provided for the EITC. Third, a child claimed for the CTC cannot be self-supporting (i.e., provide more than half of their own support), while no such requirement exists for a child claimed for the EITC.

Finally, as noted above, current law requires that, to claim the EITC, a taxpayer (and, if married, their spouse) must provide their SSNs and the SSNs of any children for whom they claim the credit. The provisions of the TCJA for the CTC require the taxpayer to furnish an SSN for the applicable child to claim the credit (this is a temporary change in effect from 2018 to 2025 but was permanently extended by P.L. 119-21). Under the TCJA, a taxpayer (and their spouse, if married) may provide either an SSN or, if they are not eligible for an SSN, an Individual Taxpayer Identification Number, to claim the CTC.15 This provision means that, in practice, mixed-status

___________________

15Under P.L. 119-21, beginning in TY 2025, a taxpayer must now provide an SSN to claim the CTC. If married filing jointly, only one spouse must provide an SSN.

families with children who have SSNs—such as U.S. citizen children—are eligible for the CTC under the TCJA but not eligible for the EITC.

Benefit Schedules

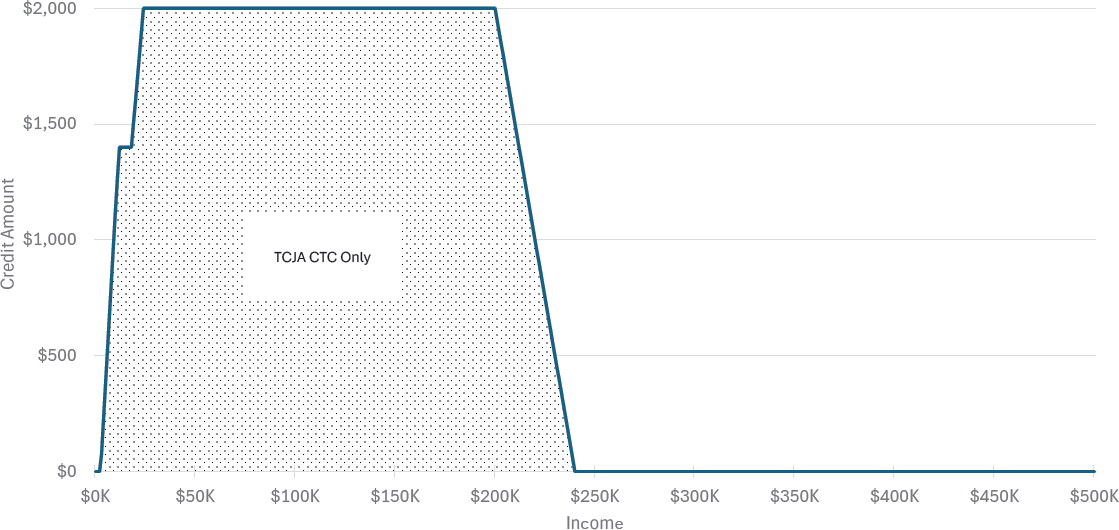

Under the provisions of the TCJA, the CTC reduces a household’s federal income tax liability by up to $2,000 per child per year.16 Lower-income households who tend to owe little to nothing in income taxes can receive the refundable portion of the credit based on their earnings. Hence, CTC benefits effectively vary by parents’ AGI (and for lower-income households, their earned income), tax filer type, and number of qualifying children (see Figures 2-3 and 2-4).

As previously discussed, the TCJA CTC has both nonrefundable and refundable components. The amount of the credit that offsets income taxes is known as the “nonrefundable” component of the CTC, and it is illustrated in Figure 2-3 for HoH tax filers with one qualifying child for TY 2018. By definition, the benefits of the nonrefundable component can only reduce a tax filer’s income tax liability to zero. Under the TCJA, HoH filers would generally not owe any income taxes until their AGI reaches $18,000. Low-income tax filers are also eligible for a “refundable” component of the CTC, which is referred to by the IRS as the Additional Child Tax Credit (ACTC). As shown in Figure 2-3, for HoH tax filers with one child and with incomes above $2,500, the ACTC under the TCJA provides a credit equal to 15% of earned income up to a maximum ACTC benefit of $1,400 when income (which is assumed to equal earned income for these calculations) is about $12,000.17 The child credit for these tax filers remains capped at the $1,400 per child maximum ACTC benefit until the tax filer’s income reaches $18,000 and they begin to owe income taxes. At this point, the HoH filer with one child begins to receive the CTC both as the refundable ACTC and the nonrefundable portion. When their AGI equals $24,000, the filer receives the maximum CTC: $1,400 as the refundable portion and $600 as the nonrefundable portion that offsets income taxes, after which the ACTC component phases out as the nonrefundable CTC phases in. When the filer has about $37,000 of AGI, they would owe $2,000 in income taxes and hence, in this simplified example, receive all of the credit as the nonrefundable portion.18 HoH tax filers with one child who have AGIs

___________________

16Under the TCJA prior to the passage of P.L. 119-21 in 2025, the maximum CTC benefit was not indexed to inflation.

17Under the TCJA, the maximum amount of the ACTC benefit is adjusted annually for inflation, rounded down to the lowest $100.

18At $36,933 of AGI, the taxpayer would have (minus $18,000 in the standard deduction) $18,933 of taxable income and would owe $2,000 in incomes taxes (10% on the first $13,600 = $1,360) plus 12% on the next $5,333 would yield $640.

NOTES: Income = earned income, although the Child Tax Credit is phased out based on modified Adjusted Gross Income. Maximum Additional Child Tax Credit = $1,400. TCJA CTC = Tax Cuts and Job Act Child Tax Credit.

between $18,000 and $37,000 receive a combination of the refundable (ACTC) and nonrefundable components of the CTC. Tax filers with AGIs above about $37,000 receive the CTC entirely as the nonrefundable credit (i.e., the maximum credit). The credit then phases out by $50 for every $1,000 (or fraction thereof) above $200,000 for a HoH filer. Hence, once this filer’s income is above $239,000, a $2,000 CTC has phased out to zero.

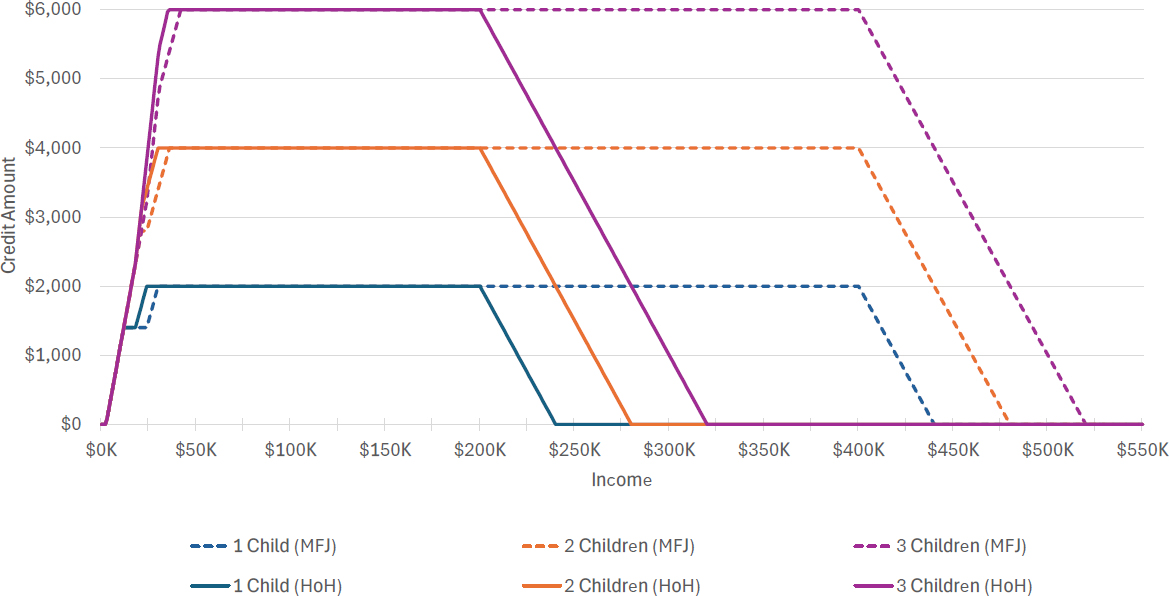

The CTC benefit schedule is similar for MFJ tax filers, although the plateau and phase-out regions extend to higher income levels (see Figure 2-4). The maximum CTC benefit also varies by the number of qualifying children, with each additional qualifying child being eligible for a maximum benefit of $2,000 and a maximum ACTC of $1,400 per child in TY 2018 (see Figure 2-4). Unlike the EITC, the maximum CTC benefit is not limited to families with more than three children, although the structure of the phase-in may limit the CTC for larger families with lower incomes. Specifically, the phase-in structure of the refundable portion of the CTC is the same irrespective of the number of qualifying children a taxpayer has (i.e., it phases in at 15% of earned income if the household has one child or three children). As illustrated in Table 2-1, this means a low-income filer with two children gets the same benefit as a low-income filer with three or more children ($1,725).

Comparing Figure 2-1 to Figure 2-4, it can be seen that the EITC and the TCJA CTC have a similar benefit structure, with benefits rising as income rises, hitting a plateau range, then phasing out as income rises further. However, relative to the EITC, a key feature of the CTC is that its benefits extend to tax filers with much higher incomes (see Table 2-1), in part to offset the loss of the personal exemption for dependents. While comparable households with children and incomes of $56,000 (200% of the SPM poverty threshold) or higher no longer received EITC benefits in TY 2018, they continued to receive CTC benefits, which provided them with 6.4% to 18.2% of their income as additional income. The antipoverty effectiveness of the CTC is likely to be somewhat similar for households with low incomes, but whether the CTC has a greater effect at somewhat higher incomes depends on how many of those families are in poverty, as will be discussed in detail in Chapter 8.

IRS Statistics

The number of tax returns receiving the nonrefundable CTC was 39.38 million in TY 2018, and 20.45 million returns received the ACTC (the IRS does not provide data on the number of returns that receive the credit as a mix of the refundable and nonrefundable credit; hence adding these two numbers together would lead to double counting of all the returns that

receive the CTC).19 Credits received in TY 2018 totaled $132.31 billion in 2021 dollars, of which $91.59 billion were nonrefundable credits and $40.72 billion comprised the refundable component of the CTC.

ARPA Reforms to CTC Policy in 2021

For TY 2021, ARPA changes that applied to households with children were more extensive for the CTC than for the EITC. In particular, ARPA made the CTC fully refundable (i.e., the maximum credit was fully available to low-income households and did not phase in with earnings), which substantially increased CTC benefits for low-income families—both in absolute amounts and percentage of income—compared to TY 2018 or to current policy. Furthermore, ARPA advanced half of the credit in monthly payments that started in mid-2021, before tax filing began in 2022. The consequences of these advance monthly payments for child poverty are examined in Chapter 8.

ARPA did not change CTC eligibility requirements for TY 2021, with one notable exception; it increased the maximum age of qualifying children from 16 to 17. It also provided larger benefits for younger children—$3,600 per child under 6 compared to a $3,000 per-child benefit for children between 6 and 17 years old.

Benefit Schedules

Three key changes to CTC benefits occurred under ARPA. First, as a result of a policy change often referred to as “full refundability,” the ACTC phase-in and the ACTC benefits cap of $1,400 per child were eliminated.20

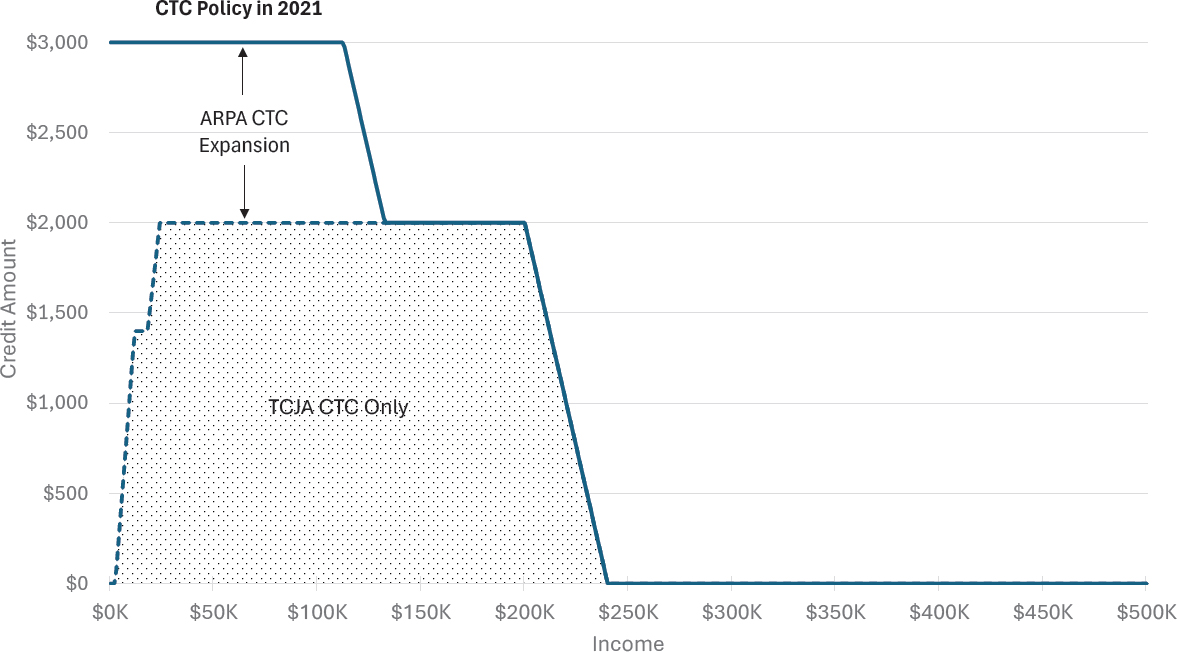

Second, the maximum credit amount was increased to $3,000 per child under 18 years old, with a larger $3,600 per-child credit for those under 6 years old. As a result of both of these changes, eligible households with no or very low earned incomes received substantially larger credits. This can be seen in Figures 2-5 and 2-6 for HoH and MFJ tax filers, respectively, with one qualifying child aged 6 to 17. The larger the maximum benefit for qualifying children ages 0 to 6 is shown in Figures 2-7 and 2-8. The schedule that prevailed under the TCJA (and subsequent to TY 2021) is shown in both figures (as shaded areas) to clarify differences in CTC benefits under ARPA. The larger maximum credit was in effect up to $112,500 of AGI

___________________

19This number of tax returns also includes those receiving the $500 nonrefundable credit for other dependents.

20Full refundability was generally only available to taxpayers who lived more than half of 2021 in the United States, with an exception for certain service members. Among married joint filers, only one spouse needed to meet this principal place of abode requirement.

for HoH filers and $150,000 of AGI for MFJ filers. As household incomes increased from these levels, CTC benefits declined until they reached the benefit schedule that prevailed under prior law (see Figures 2-5 and 2-6). In short, under the policies in place in 2021, the ARPA CTC Expansion of credits provided temporary increases in credits to households with no taxable income and up to those with moderate incomes compared to what those households would have received if the TCJA CTC Only schedule had prevailed.

Third, ARPA instituted an advance payment of the CTC, under which the IRS provided one-half of the CTC annual benefit as monthly installments from July to December 2021, with the remaining half paid after filing 2021 tax returns in 2022.21 Advance payment amounts were calculated based on an estimate of what the household’s 2021 CTC would be, generally using data on family structure and income from 2020 tax returns. These advance payments based on an estimate of their 2021 credit then had to be reconciled with the 2021 credit the household was actually eligible for. Under this arrangement, the taxpayer calculated their actual 2021 credit on their 2021 return and subtracted from this amount any benefits they had received in advance payments. If a taxpayer received more in advance payments than the 2021 credit they were eligible for, they might receive a smaller refund or even owe tax.

For example, if a low- or moderate-income taxpayer had one older qualifying child on their 2020 return, the IRS would generally have advanced them $1,500 (half of $3,000) over the last six months of 2021 (or $250 a month). If that child ultimately did not live with the filer in 2021, and the tax filer had no other qualifying children, their TY 2021 CTC would be $0 and the $1,500 of advance payments would generally need to be paid back to the IRS. In certain cases, a safe harbor provision could protect low-income families from repayment. In contrast, if a tax filer failed to receive any advance payments they had been eligible for—for example because their child was born in 2021—they would receive the full 2021 CTC benefit when they filed their 2021 return. Details of advance payments and determination of which tax filers received excess benefits in advance payments are described in Congressional Research Service (2021).

Table 2-1 displays the CTC credit amount received by HoH and MFJ households with differing incomes and numbers of children under the provisions of the TCJA (see columns [1]) under the provisions for TY 2021 (see columns [2]). The table also includes the combined EITC and CTC benefits these households would have received in TY 2018 (see columns [5]) and under the policies in place in 2021 (see columns [6]). For households with an annual income (or earnings) of $14,000, the 2021 CTC provided between

___________________

21https://taxfoundation.org/blog/american-rescue-plan-covid-relief/

$3,600 and $10,200 to both HoH and MFJ households, with the lower amounts for households with only one young child and higher amounts for households with three children (two children ages 0 to 5 and 1 child age 6 to 17). These benefits constitute 25.7% to 72.9% of households’ income. When these CTC benefits are combined with the EITC, the combination of credits ranges from $7,218 to $16,500, which is between 51.6% and 117.9% of these households’ earned incomes. This represents a markedly larger increase in household resources compared with the amounts households achieved under the provisions of the EITC and CTC for 2018.

Except for the highest-income households, the CTC benefits received under 2021 policy are greater than the corresponding CTC benefits under TCJA. Furthermore, for incomes up to $280,000, the increase in resources above household income is mainly due to the 2021 CTC (see Table 2-1). Finally, for the scenarios displayed in Table 2-1, only when household income reaches $280,000 do ARPA reforms no longer improve household resources relative to benefits received under 2018 law. (See Chapter 8 for impacts of these expanded benefits on reducing child poverty.) Increases in household resources due to increased benefits under ARPA (primarily from the 2021 CTC; see Table 2-1) are likely to markedly impact child poverty among low-income families.

The markedly different benefit structure of the CTC Policy in 2021 compared to that under the TCJA—with the latter providing lower benefits at the lowest incomes than at somewhat higher incomes and with the former providing the opposite—is likely to have important antipoverty impacts, depending on how many families with different incomes are in poverty without the programs. This will be discussed in detail in Chapter 8.

IRS Statistics

IRS statistics for numbers of returns and 2021 CTC credit amounts in TY 2021 are displayed in Table 2-2. Due to ARPA provisions, the entries for TY 2021 in Table 2-2 differ slightly from those under the CTC in TY 2018. Namely, while the IRS broke down the nonrefundable and refundable components of the CTC claimed on tax returns, they did not provide this breakdown for the advance payments of the credit. Hence, a breakdown of the 2021 CTC into nonrefundable and refundable components comparable to 2018 levels is not available.

Nonetheless, total credit dollars can be calculated. The total amount of CTC credits substantially increased in TY 2021 relative to TY 2018, with $209.49 billion paid out for 2021—an increase of slightly more than $77 billion in 2021 dollars.

STATE-LEVEL POLICIES

A sizeable number of states have also implemented state-level EITC and CTC policies.22 State EITC and CTC credits were accounted for in the determination of family income in the analyses presented in Chapter 8 and in the evaluation of alternative policy options in Chapter 9, but neither set of analyses estimates the impacts that changes in state EITC or CTC policies may have had on child poverty. (See Appendix I for details of how the Transfer Income Model version 3 estimates these impacts.)

CONCLUSION

CTC Policy in 2021 increased coverage and provided larger benefits, particularly for families with no earnings and those with young children (ages 0 to 5). For families with children, EITC provisions were largely unchanged by ARPA.

Children claimed for both the EITC and CTC must have SSNs. Both credits also require that claimed children meet requirements based on their relationship to the tax filer and time spent living with the filer, which excludes a small percentage of children (i.e., those who live with individuals to whom they are not related or to whom they are only distantly related, such as a cousin). The EITC is also generally unavailable to mixed-status families, while these families may be able to claim the CTC under current law.

Under current law, both the EITC and the refundable portion of the CTC available to low-income families require tax filers to have earned income to be eligible. However, for the 2021 CTC, this requirement was temporarily suspended, expanding access to the credit to those with no earnings. For TY 2021, maximum EITC benefits were between $3,618 and $6,728 for families with one, two, or three or more children, whereas CTC benefits are $2,000/per child (through TY 2024) and were as high as $3,600 under ARPA. Under ARPA, EITC credit amounts increased for childless tax filers but generally remained unchanged for families with children.

Having reviewed the eligibility criteria, benefit structures, and key policy changes to the EITC and CTC—particularly under 2021 ARPA reforms—the next step is to evaluate how these tax credits influenced child poverty. The next chapter introduces the SPM, the primary tool used by the committee to assess these impacts, and explains why it offers an accurate, policy-relevant gauge of poverty.

___________________

22See Tax Policy Center (2024a) and National Conference of State Legislatures (2024a) for details on state CTC programs and see Tax Policy Center (2024b) and National Conference of State Legislatures (2024b) for details on state EITC programs.

This page intentionally left blank.