Pathways to Reduce Child Poverty: Impacts of Federal Tax Credits (2026)

Chapter: Summary

Summary

The American Rescue Plan Act (ARPA) of 2021 temporarily expanded the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC). As part of the Consolidated Appropriations Act of 2023, Congress directed the National Academies of Sciences, Engineering, and Medicine (National Academies) to conduct a comprehensive study of what impact these and other possible changes to federal tax policy had or would have on child poverty.1 Specifically, the statement of task asked the following questions:

- What were the impacts of the federal CTC and the EITC in 2021 on the level of poverty for all U.S. children and the level of poverty for specific populations of U.S. children?

- How was the CTC implemented in 2021? How did the implementation of the program impact participation and therefore its effectiveness for reducing child poverty?

- Among children in different racial and ethnic groups or immigrant families, as well as other populations of interest, how did the implementation of the CTC in 2021 affect credit access and poverty reduction?

- What further changes to the EITC and CTC, if adopted, would reduce the number of U.S. children in poverty?

Besides race/ethnicity, the specific subgroups the committee was charged to consider included those with different parental education and marital

___________________

1The committee’s full statement of task is listed in Chapter 1, Box 1-1.

status, household living arrangements, citizenship or immigrant status, and residential location. Also, according to the congressional charge, poverty was to be assessed using the Census Bureau’s Supplemental Poverty Measure (SPM), a fuller measure of family resources than the Official Poverty Measure.

To meet this charge, the National Academies’ Board on Children, Youth, and Families in collaboration with the Committee on National Statistics convened an ad hoc committee with expertise across the social sciences. The committee reviewed research literature, commissioned data analyses, held public information-gathering sessions, and conducted listening sessions with parents and other community stakeholders.

HISTORY OF THE EITC AND CTC

The EITC and CTC are two major tax benefits that support low-income individuals and families in the United States. Administered by the Internal Revenue Services (IRS), these credits aim to supplement household income, reduce poverty, and encourage work, especially among families with children.

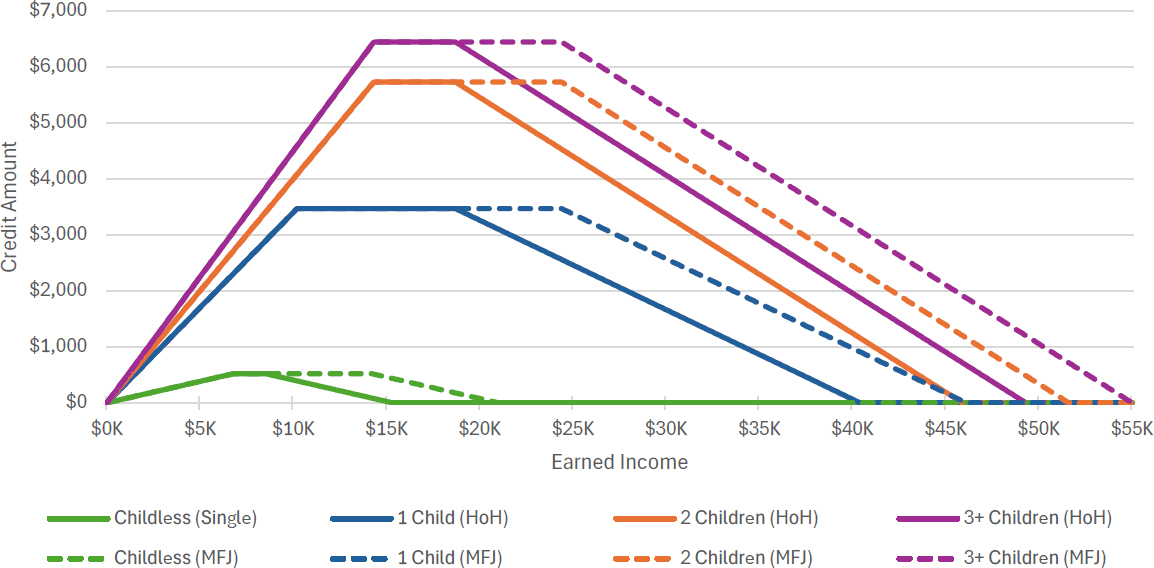

Established in 1975 and amended over time, the EITC is a tax credit for low-income workers, particularly those with children. It is fully refundable, providing benefits even to families owing no income taxes. Eligibility depends on earnings, age, tax filing status, presence of qualifying children (as defined in the tax code), and possession of Social Security Numbers (SSNs). The credit increases with earnings (phase-in), levels off (plateau), then declines (phase-out). Families with more qualifying children receive larger credits.2 Figure S-1 displays the 2018 EITC amounts for the phase-in, plateau, and phase-out levels of earnings for different types of tax filers and by numbers of qualifying children.

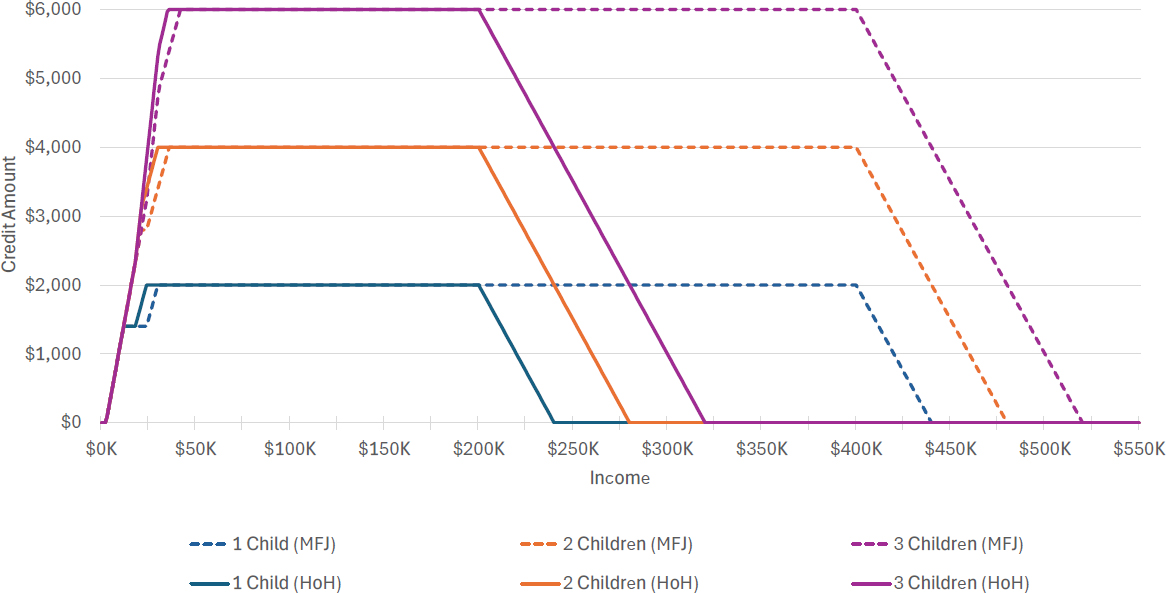

The CTC, first enacted in 1997, was designed to reduce income taxes of families with earned income and dependent children. Initially structured as a nonrefundable credit, it applied only to wage-earning families that owed federal income taxes; most low-income families received no benefit until their earnings were high enough to trigger federal income taxes. The Economic Growth and Tax Relief Reconciliation Act of 2001 expanded CTC refundability, allowing families with earnings above a threshold to receive part of the credit even if they owed no federal income taxes. Over time, policy changes adjusted the CTC amount, income requirements, age of eligible dependents, refundability rules, and SSN requirements. Unlike the

___________________

2For example, a family earning $20,000 with two children would receive about $6,604 in EITC benefits; a married couple earning $30,000 with three children, about $7,430; and a single person earning $12,000 with no children, about $632.

NOTES: While the EITC phases in based on a tax filer’s earned income, it phases out based on the tax filer’s earned income or adjusted gross income, whichever is greater. ARPA = American Rescue Plan Act, EITC = Earned Income Tax Credit.

EITC, the CTC allows children with SSNs to qualify even if their parents file taxes without an SSN. Like the EITC, the CTC includes a phase-in, plateau, and phase-out (see Figure S-2 for a 2018 example).

In 2021, ARPA made a series of temporary changes to the EITC and CTC. The EITC temporarily increased the benefit amount for childless workers, broadened eligibility by lowering the minimum age, and eliminated the upper age limit, along with other changes. But ARPA did not change the benefit amounts for taxpayers with dependent children and likely had no impact on the vast majority of families with children.

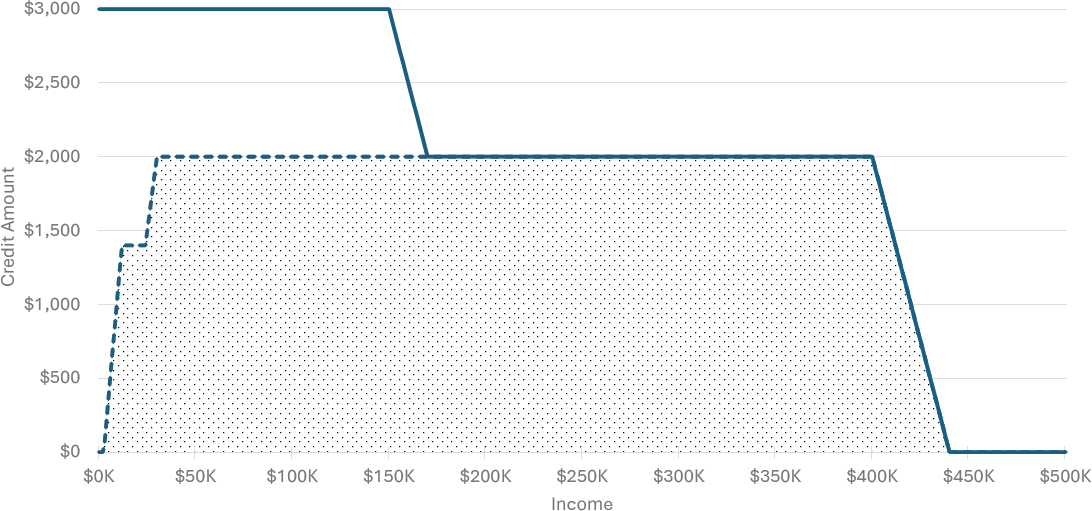

The ARPA legislation made more significant temporary changes to the CTC, including making the credit fully refundable so parents with little or no income could receive the full amount; it also increased the maximum credit for children under 6 and children ages 6 to 17. Figure S-3 shows, for a married couple filing jointly, how changes to the CTC benefit schedule under ARPA compared to that under the prior (and later) provisions of the CTC under the Tax Cuts and Jobs Act (TCJA). Under ARPA, a family with two children ages 3 and 7 could receive $6,600 in CTC benefits for the year, compared to $4,000 under TCJA CTC rules. ARPA also allowed the IRS to deliver half the credit in monthly advance payments from July to December of 2021, rather than as a lump sum. For example, instead of receiving $3,000 at tax time, a parent might receive $250 per month for six months, with the rest received after filing a return. (See Chapter 2 for further details of the EITC and CTC policies prior to and during 2021.)

ASSESSING THE IMPACTS OF 2021 EITC AND CTC ON CHILD POVERTY

To estimate the impacts of the provisions of ARPA and alternative policy options,3 the committee used the Urban Institute’s Transfer Income Model version 3 (TRIM3), a microsimulation model, based on data from the Current Population Survey Annual Social and Economic Supplement (CPS ASEC). Despite some limitations,4 TRIM3, and its use of the SPM, is the most robust tool available for analyzing the effects of the EITC and

___________________

3Since changes to the EITC under ARPA focused primarily on childless adults, the committee assumed changes had no effect on child poverty, though the non-ARPA EITC still could reduce it. The effects of the ARPA CTC Expansion on child poverty reflected both the original CTC and the changes in response to ARPA.

4The SPM has limitations, particularly in how it estimates taxes and credits. The SPM uses tax models rather than actual tax return data, which introduces potential errors due to incomplete or misreported information on income and household composition. The SPM also counts tax credits in the year they are earned rather than the year they are received, which can skew results in years with major policy changes, like 2021. Data quality also is a concern, as many low-income families underreport benefits, as was particularly the case during the pandemic.

NOTE: Income = earned income, although CTC is phased out based on modified adjusted gross income. CTC = Child Tax Credit.

NOTE: Income = earned income, although CTC is phased out based on modified adjusted gross income. CTC = Child Tax Credit.

CTC on child poverty. In producing estimates of child poverty in the United States, a key difference between the TRIM3 and that used by the Census Bureau is the adjustments TRIM3 uses for the undercounts in CPS ASEC for receipt of various safety net programs other than tax credits. As a result of these adjustments, TRIM3 produced lower child poverty estimates than those produced by the Census Bureau in 2021. This difference is discussed and analyzed in Chapter 8.

With respect to its charge to analyze the effects of EITC and CTC policies in 2021, the committee analyzed the effects of four separable components of these policies on child poverty relative to having no EITC or CTC:5

- The EITC policy in place in 2021, referred to as “EITC Policy in 2021”;6

- The component of the CTC in 2021 that was enacted under the TCJA, referred to as “TCJA CTC Only;”

- Changes to the CTC in the ARPA legislation, referred to as the “ARPA CTC Expansion;” and

- The combined EITC and CTC policies in place in 2021, referred to as the “Combined EITC & CTC Policies in 2021.”7

(Figure S-3 illustrates the components of the CTC Policy in 2021 for married filing jointly couples.)

Before carrying out its analysis, the committee identified three key issues it needed to better understand and address to assess the impacts of ARPA changes to the EITC and CTC on child poverty:

- The share of families with children who are eligible for the program and, among them, the share who receive (or “take up”) the credits;

- The extent to which other federal COVID-19 pandemic (hereafter, “pandemic”) programs reduced child poverty and may have offset the additional poverty reduction effects of the Combined EITC & CTC Policies in 2021; and

- The extent to which families adjusted their employment in response to these credits, and whether any resulting changes in earned income enhanced or diminished the credits’ impact on child poverty.

___________________

5The particular configuration of these components whose antipoverty effects are analyzed is discussed in the Methods section of Chapter 8.

6Given the changes to the EITC under ARPA noted above and discussed in Chapter 2, the committee could not assess the separate impacts of the pre-ARPA EITC and the ARPA EITC Expansion on child poverty (see Box 1-2 for descriptions of these components). Thus, it only assessed the overall impact of the EITC Policy in 2021.

7See Box 1-2 in Chapter 1 for definitions of the components of the EITC and CTC Policies considered in this report.

Take-Up of Tax Credits

To assess take-up of the EITC and CTC, the committee reviewed existing literature on multiple data sources, each with their own strengths and limitations. The analysis examined differences across demographic groups and considered system-level and policy factors that may have affected both participation and compliance with eligibility rules.

The committee also examined evidence from IRS administrative records and national surveys to assess take-up. IRS records accurately show benefit receipt but lack detailed demographics, while national surveys offer richer demographic data but rely on self-reports or estimated (“imputed”) values, which may understate receipt due to errors or missing tax information. IRS data indicate relatively high overall participation—about 81% of eligible individuals received the CTC and EITC payments, reaching roughly 84% of eligible children—but not all eligible families received these benefits. Self-reported survey data indicate lower CTC and EITC take-up among lower-income families, Hispanic households, and those who had not recently filed taxes.

TRIM3 simulations assign credits to all survey respondents who appear eligible to receive them, assuming 100% take-up of credits. However, even with this method, the numbers of filers and credit amounts often differ from administrative totals. The committee examined various pieces of evidence, including evidence from linked CPS and IRS tax return data, to better understand and possibly adjust for this discrepancy. While these analyses suggested several possible explanations, the committee concluded it could not confidently make adjustments for these differences. As a result, one of the committee’s recommendations is for further research to understand the determinants and reasons for incomplete take-up and disparities between IRS and survey data.

Key Message: Not all eligible families receive tax credits, and there are discrepancies between estimates from tax simulation models like Transfer Income Model version 3 and Internal Revenue Service data regarding take-up. The committee was unable to develop credible strategies to adjust for these disparities; better understanding them remains an important issue for future research.

Other COVID-19 Pandemic-Period Policies and Programs

Isolating the effects of the EITC and CTC policies in 2021 is complicated by the social, economic, and policy conditions of 2021. In response to the pandemic’s impact on employment and household income, federal, state, and local governments changed existing unemployment and safety net

programs and introduced new cash payments. While important for reducing child poverty, the presence of these programs complicated efforts to isolate the impacts of the EITC and CTC during this period.

The committee reviewed major policies and programs8 and found that new and expanded pandemic measures in 2021 both directly and indirectly affected estimates of the EITC’s and CTC’s impact on child poverty by altering the baseline poverty rate and the context in which families received the expanded credits.

The committee estimated that these other pandemic-related programs reduced child poverty rates from 17% to 5.7% in 2021, and this reduction lessened the EITC or CTC impacts on poverty. To better isolate the impact, the committee estimated poverty impacts that either included or excluded many pandemic-related resources. Since these temporary pandemic-era expansions and exemptions are unlikely to continue if ARPA changes to the EITC and CTC are made permanent, estimates that exclude the effects of other temporary programs may provide useful insights. However, the committee also noted that temporary programs may have influenced family decisions—such as employment, benefit participation, or living arrangements—though these effects are not fully understood and difficult to adjust for.

Key Message: The presence of other pandemic-related programs in 2021 complicated the committee’s task to isolate the impacts of the provisions of the Earned Income Tax Credit and Child Tax Credit policies in 2021 on child poverty.

Employment Effects

Another important question is whether and how families adjusted their work behavior in response to expanded tax credits. The report reviews research on short-term changes, like the ARPA expansion to the CTC, and research on longer-term or permanent reforms. It examines how employment decisions (or “labor supply”) respond to work incentives shaped by both wages and income support programs, which can either encourage or discourage people from working.

Research shows that stronger work incentives generally increase employment—which strengthens the antipoverty impact of the tax credits or income supports that raise incentives. The incentive to work depends on

___________________

8The committee defined major programs as those with funding over $5 billion that directly affected household resources. “Directly” refers to policies providing income, rather than influencing the broader economic and public health context that may have changed economic calculations, resulting in decreased poverty. The committee recognizes this categorization is somewhat subjective and does not imply that excluded programs were unimportant.

the extent to which these benefits are available for families with little or no earnings—the more available they are to such workers, the lower the incentives are to work. While the provisions of the non-ARPA EITC and the TCJA CTC Only provide little or no benefits to those with no earnings, they strengthen work incentives and raise employment. In contrast, the changes under CTC Policy in 2021 made CTC benefits fully available to those with no earnings, it thereby reduced work incentives.

But uncertainty about the magnitude of the effect remains. Economists call this responsiveness of the labor supply “elasticity”—the extent to which employment changes when financial incentives to work increase or decrease. Elasticities vary by income, family structure, or policy design, and evidence suggests elasticity is highest for low-income families headed by unmarried mothers. Evidence shows that the elasticity also varies with whether benefit changes are temporary or permanent; temporary benefits like ARPA have smaller effects. Accordingly, the committee used a range of elasticities in its analysis, varying by family type and whether changes were permanent or temporary.

Key Message: The Earned Income Tax Credit and Child Tax Credit affect employment decisions, which are likely to also affect child poverty rates, although the magnitudes of employment-level changes due to these tax credits remain uncertain.

ANALYSIS AND RESULTS FOR IMPACTS OF EITC AND CTC POLICIES IN 2021

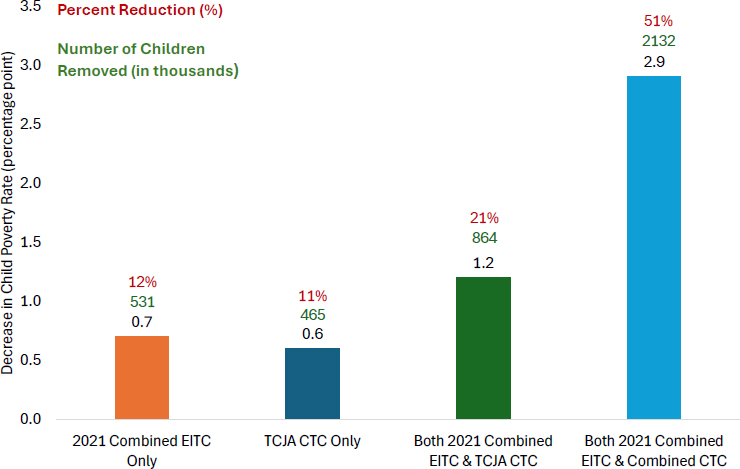

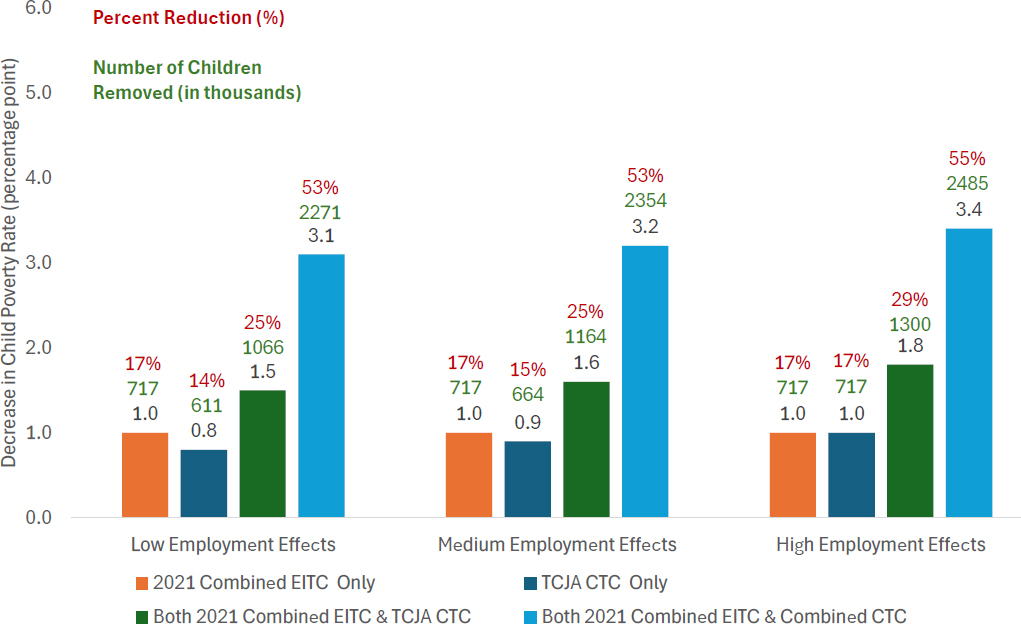

TRIM3 analysis simulated eligibility and receipt of the EITC and CTC in 2021. It estimated the antipoverty effects of the four components of the policies in place in that year: the EITC Policy in 2021, the TCJA CTC Only, the ARPA CTC Expansion, and the Combined EITC & CTC Policies in 2021. The analysis considered different scenarios with and without employment changes and the presence of other pandemic programs. Even without adjusting for employment effects and accounting for other major pandemic programs, the Combined EITC & CTC Policies in 2021 were estimated to significantly reduce child poverty.

Key Message: The Combined Earned Income Tax Credit and Child Tax Credit (CTC) Policies in 2021, including the American Rescue Plan Act CTC Expansion, had major impacts on child poverty, reducing it by approximately 2.9 percentage points or about 50%. Adjusting for employment effects, their estimated impacts were even greater, reducing child poverty by 3.1 to 3.4 percentage points or 53% to 55%.

NOTE: CTC = Child Tax Credit, EITC = Earned Income Tax Credit, TCJA = Tax Cuts Job Act.

SOURCE: Estimates from TRIM3 commissioned by the committee.

The estimated reductions in child poverty reflect the cumulative impact of the programs. Without accounting for employment changes, the EITC Policy in 2021 reduced child poverty by 0.7 percentage points, the TCJA CTC Only reduced child poverty by 0.6 percentage points, and together those two credits reduced child poverty by 1.2 percentage points—lifting nearly 900,000 children out of poverty. But adding the fully refundable component of the CTC under ARPA, which is the ARPA CTC Expansion noted above, reduced child poverty by another 1.7 percentage points (2.9 minus 1.2), more than the two pre-ARPA programs combined. Altogether these credits, without employment effects, lowered child poverty by 2.9 percentage points, lifting over 2 million children out of poverty (see Figure S-4).

Adjusting for employment effects—see Figure S-5—the estimated impacts of these policies were even greater. At medium employment effects levels, the EITC Policy in 2021 reduced child poverty by 1.0 percentage point, the TCJA CTC Only by 0.9 percentage points, and the two together reduced it by 1.6 percentage points—lifting nearly 1.2 million children out of poverty. Adding the ARPA CTC Expansion further reduced child poverty by another 1.6 percentage points (3.2 minus 1.6), which was equal to the combined effect of the other two programs. Altogether these credits,

NOTE: CTC = Child Tax Credit, EITC = Earned Income Tax Credit, TCJA = Tax Cuts Job Act.

SOURCE: Estimates from TRIM3 commissioned by the committee.

adjusting for employment effects, lowered child poverty by 3.2 percentage points, lifting 2.4 million children out of poverty. (The patterns for and conclusions drawn using low or high employment effects are similar.)

Employment effects of the TCJA CTC and all versions of the EITC are positive because benefits in both cases are not available to families with no earnings, creating strong work incentives; the CTC Policy in 2021 reduced those incentives, since families with little or no earnings were eligible for the full credits, but the credits’ estimated impacts on employment were muted because they were temporary. Combining the incentives and elasticities of the pre-ARPA and ARPA changes generates positive effects of the combined EITC and CTC policies that were implemented in 2021.

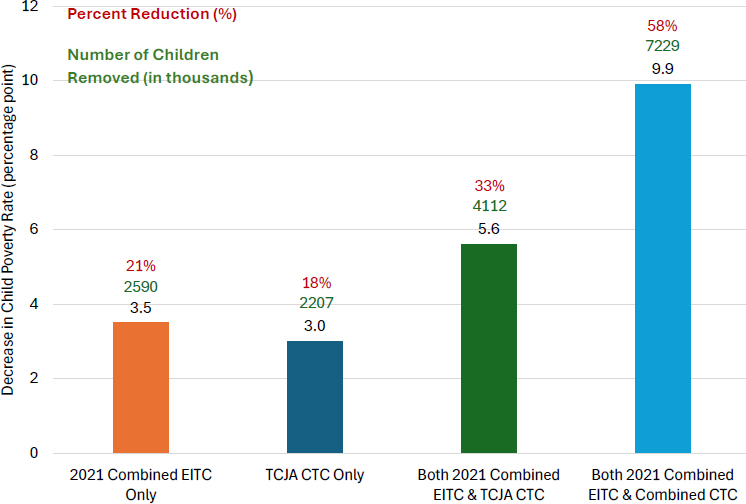

The committee found that other major pandemic relief programs significantly reduced child poverty in 2021, and without them, the combined EITC and CTC policies as implemented in 2021 would have had an even greater effect. In their absence, the combined credits would have lifted over 7 million children out of poverty, lowering child poverty by nearly 10 percentage points or nearly 60% (see Figure S-6). This analysis underscores how other forms of relief had already lowered the baseline poverty rate and limited the possible range of improvement.

NOTE: CTC = Child Tax Credit, EITC = Earned Income Tax Credit, TCJA = Tax Cuts Job Act.

SOURCE: Estimates from TRIM3 commissioned by the committee.

The largest child poverty reductions from the EITC and CTC policies in 2021 were seen among children in single-parent families and large households, young children, those with part-time employed and less-educated parents, and those living in the West, South Central, and Pacific census regions. Hispanic children and children in mixed-status families had the largest percentage point reductions in child poverty as a result of the credits, but these reductions were smaller in relative terms, especially in families with an undocumented family member or noncitizen child, since many immigrant and mixed-status families were not eligible for the EITC or CTC.

In 2018 (a nonpandemic year), the highest child poverty rates were among children in single-parent families, families without workers, families with parents with less than high school education, Hispanic children, and children in immigrant families or mixed-status families. In 2021, these same subgroups continued to have disproportionately elevated child poverty rates.

The committee drew the following conclusions from its analysis of the estimated impacts of the Combined EITC & CTC Polices in 2021 and its components on child poverty:

- Substantial Poverty Reduction: The Combined EITC & CTC Policies in 2021 significantly reduced child poverty—by 2.9 percentage points, or over 50%—even amid a low-poverty baseline due to the impact of other pandemic relief programs. In the absence of these other programs, the EITC and CTC policies in 2021 would have lifted over 7 million of the more than 12 million children initially living in families with incomes below the poverty line out of poverty.

- Non-ARPA Impacts: Even without the ARPA changes to the CTC, the EITC Policy in 2021 and the provisions of the TCJA CTC Only provided more support to families just above the poverty line—for example, for low-wage working families earning under about $42,000 in 2021 for a family of four—than to those in poverty. Relative to no EITC or CTC, the EITC Policy in 2021 + TCJA CTC reduced the percentage of children living in near poverty (i.e., those between 100% and 150% of the poverty threshold) by 5.6 percentage points, or 27%, lifting over 4 million children from near poverty.

- Limited Employment Effects: The ARPA CTC Expansion likely had limited effects on parental employment due to its temporary nature. However, permanent expansions could modestly raise or lower employment, depending on employment responses, but child poverty reductions would remain substantial.

ALTERNATIVE POLICY OPTIONS

Building on its analysis of the ARPA EITC and CTC Expansions in 2021, the committee analyzed 16 policy options that would permanently alter the EITC and CTC (see Chapter 9). Using TRIM3 and CPS ASEC data for calendar year 2018, the analysis simulated how each policy option—modifying a single feature at a time, including the maximum credit amount, refundability, phase-in/phase-out structure, or eligibility—could reduce child poverty relative to the provisions of the TCJA CTC and non-ARPA EITC. Because these changes were assessed sequentially, the estimated impact associated with each policy depends in part on the order in which changes are made. The goal was to understand how different versions of the EITC and CTC might reduce child poverty outside the unique context of the pandemic and other pandemic relief policies.

Key Message: Policy options that increase the generosity of the Child Tax Credit (CTC) relative to the current CTC policy enacted under the Tax Cuts and Jobs Act are all estimated to reduce child poverty. Adjusting for employment effects reduces the estimated impact on child poverty for almost all options considered, since these policies would likely reduce work incentives, but all options still reduce child poverty compared to current CTC policy.

Although the committee estimated the antipoverty effects of all 16 policy options (“PO” in list below), the report focuses in depth on seven options that reflect key policy trade-offs, such as the link between benefits and work, support for families with no or very low earnings, credit generosity, and cost. The committee also evaluated how permanent changes might affect parental employment and thus labor market earnings.

- PO 1 represents current policy, that is, the non-ARPA EITC + TCJA CTC policies, that included a $2,000 per-child credit phased in at 15% of earnings (per family) in excess of $2,500 under the current EITC and CTC policies adjusted to 2018 dollars. (See Figures S-1 and S-2, respectively, for the EITC and CTC benefit schedules under current policy.)

- PO 5 phases in the credit from the first dollar of earnings at 15% per child instead of per family.

- PO 6 adds a $1,000 minimum (or “lump sum”) credit to PO 5.

- PO 9 exempts certain caregivers (e.g., those with young children, disabilities, or aged 65+) from earnings requirements.

- PO 11 introduces a larger credit, of the size under ARPA policy, but provides just 50% minimum credit to families with no earnings.

- PO 12 approximates the ARPA CTC Expansion with a higher and fully refundable credit, but with a faster phase-out (to reduce total fiscal outlays).

- PO 13 builds on PO 12 by adding an additional $2,000 per child phased in at 15%.

The committee compared child poverty rates in POs 2–16 to those in PO 1, reflecting current policy, to estimate the antipoverty effects of all of the new policy options. Since PO 12 reflects the ARPA changes of 2021, the report also evaluated changes that are both less and more generous than those implemented by ARPA.

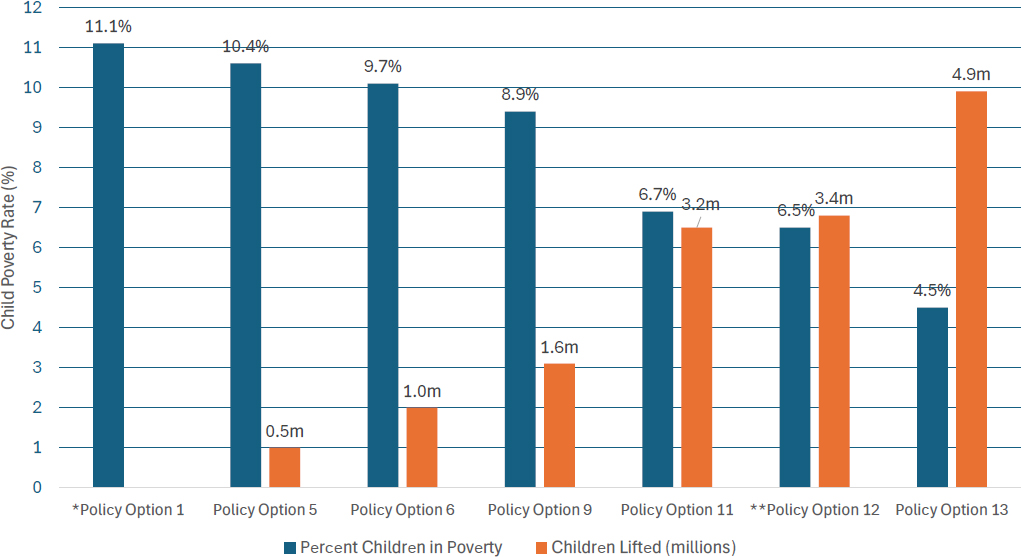

The committee first estimated the impacts of these policy options with no adjustments for employment effects. PO 1, reflecting current law, shows 8.2 million children in poverty and the highest child poverty rate of 11.1% (see Figure S-7). Among options with a minimum earnings requirement, without incorporating employment responses, PO 5 provides a modest reduction in child poverty to 10.4%, by increasing benefits for families with low earnings through a 15% per-child phase-in from the first dollar of earnings. Adding a $1,000 minimum credit in PO 6 reduces child poverty to 9.7%, while PO 9 drops it to 8.9% by exempting certain caregivers from meeting minimum earnings thresholds to receive the credit.

More substantial reductions are seen in options that provide a higher maximum credit and greater support to families with no or very low earnings. PO 11, with a higher credit and 50% minimum credit to families without earnings, reduces child poverty to 6.7%, and PO 12, replicating 2021 ARPA full refundability, reduces child poverty to 6.5%. The largest estimated impact comes from PO 13, which combines a high minimum credit, full refundability, and a work-based add-on, reducing child poverty to 4.5% and lifting 4.9 million children out of poverty.

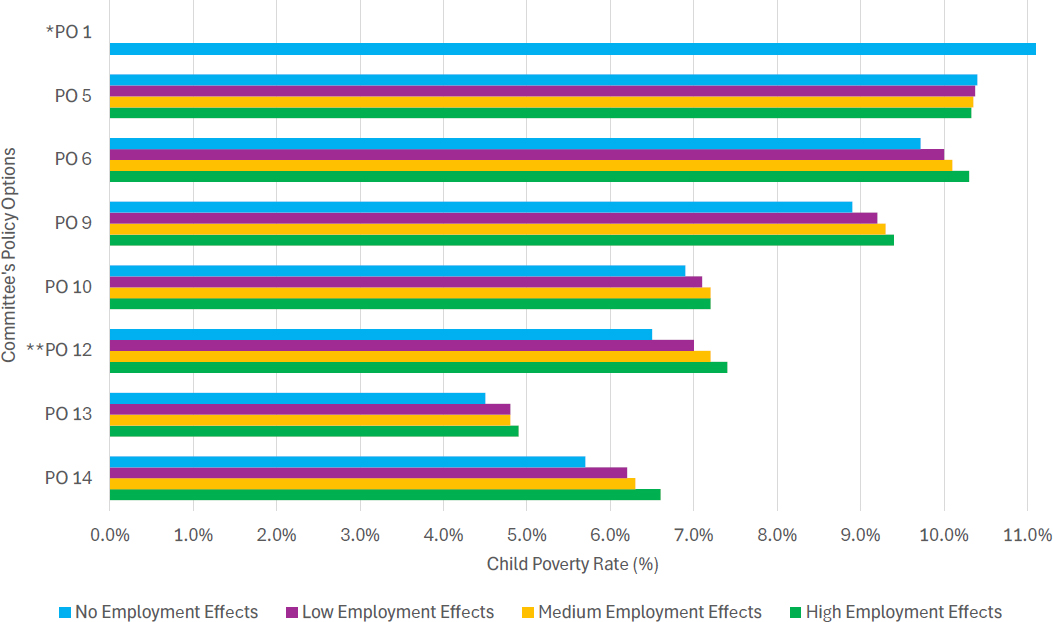

The committee also evaluated how different employment effects—based on low, medium, and high estimates of labor supply elasticities—might affect child poverty under permanent versions of a subset of the committee’s 16 policy options that notably varied the incentives to work in one direction or another. While the temporary nature of the ARPA CTC Expansion resulted in little impact on parental employment, long-term expansions could raise or lower employment and thus change families’ earnings from work, depending on employment responses.

Accounting for employment effects reduces the estimated impacts of almost all of the committee’s policy options on child poverty by 0.2 to 0.9 percentage points (2.9% to 16%), compared to estimates of the same policy options that made no such adjustments (see Figure S-8). Except for PO 5, which raises work incentives by phasing in the CTC on the first dollar earned adjusting for the estimated employment effects reduces the

NOTES: *Policy Option 1 is the non-American Rescue Plan Act of 2021 Earned Income Tax Credit (EITC) + Tax Cuts and Job Act Child Tax Credit (CTC) policy option.

**Policy Option 12 is the Modified Combined EITC & CTC Policies in 2021. In the modified version CTC benefits schedule was phased out faster than in the CTC policy implemented in 2021. See Chapter 9 for details.

SOURCE: Estimates from TRIM3 commissioned by the committee.

NOTES: *PO 1 is the non-American Rescue Plan Act of 2021 Earned Income Tax Credit (EITC) + Tax Cuts and Job Act Child Tax Credit (CTC) PO. **PO 12 is the Modified Combined EITC & CTC Policies in 2021. Limited to a subset of the committee’s 16 POs.

SOURCE: Estimates from TRIM3 commissioned by the committee.

estimated impacts on child poverty because the other options reduce work incentives and employment. Among the policy options that produce some of the largest reductions in child poverty, adjustments for employment effects reduce the impacts on child poverty the most for PO 12 (which approximates the Combined EITC & CTC Policies in 2021) and PO 14; they have negative but lesser impacts on PO 10 and PO 13.

Nonetheless, all policy options reduce child poverty compared to current policy, even after accounting for employment effects. The options that increase maximum benefits—even for nonearners—reduce child poverty the most, even after accounting for negative employment effects. Poverty reductions are made even larger when additional CTC components (as in PO 13) or additions to the EITC strengthen work incentives. Specifically, the committee considered how making the EITC more generous—by raising the maximum credit by 8 percentage points—would affect child poverty in combination with some of the policy options considered. In each case, child poverty is further reduced, typically by half an additional percentage point, or less.

Finally, reductions in child poverty varied across subgroups defined by parental characteristics, household structure, race/ethnicity, and immigration status. Generally, families with the highest pre-ARPA poverty rates experienced the largest declines in poverty under the alternative policy options considered.

Regarding fiscal costs, the estimated fiscal outlays for many CTC policy options range from slightly below current levels (around $100 billion) to more than double. Under current policy, almost 89% of outlays go to children in families with incomes above the poverty line, while the 18% of children living in poverty receive the remaining 11%. To further reduce child poverty, options like increasing maximum benefits require higher spending, including increased outlays to children not growing up in poverty, unless one also includes more rapid phase-outs of benefits at higher incomes. Put differently, reducing total fiscal costs requires limiting outlays to children in higher-income families.

The committee drew the following conclusions from its analysis of other policy options:

- Alternative policy options reduce child poverty: All CTC policy options reduce child poverty relative to current policy, though estimated impacts vary. Policy options that maintain the $2,000 maximum credit have modest effects; those increasing the credit have larger reductions. A more generous EITC also modestly reduces child poverty relative to the provisions of current policy.

- Accounting for employment effects: Since most policy options considered would reduce work incentives and employment, including

- employment effects in the report’s estimates generally reduces child poverty impacts compared to not adjusting for those effects. Nonetheless, even after accounting for employment effects, all the committee’s policy options reduce child poverty relative to current policy.

- Costs of policy options: Those policy options that increase the maximum CTC benefit have the largest estimated impacts but also require the largest fiscal outlays. Thus, trade-offs exist between the reduction of child poverty and the costs of doing so.

- Subgroup variation: The estimated impacts of policy options varied across demographic and income groups, with the poorest subgroups benefiting the most.

FUTURE RESEARCH

High-quality research is essential for evaluating the effectiveness of the EITC and CTC in reducing child poverty. The committee identified several data gaps and methodological limitations that constrained its analysis, and it recommends steps to improve the evidence base for policy making (see Chapter 10). Recommendations focus on improving data sources and key measurements, advancing research to better evaluate impacts on child poverty and well-being, and supporting policy experimentation and evaluation. The committee also calls for methodological improvements to better assess poverty and policy implementation. Stronger research and data infrastructures will enable more effective design and evaluation of future EITC and CTC policies and programs.